Where There’s a Bubble, There’s an Anti-Bubble

Trades in Whisky;

SpaceX is coming to the stockmarket, probably on Friday, 12 June. I should have mentioned last week that RIT Capital (RCP) has a holding, which has swung them back into the limelight. That is very good news because ByteTree clients already have the bragging rights and don’t need to buy any more on IPO day.

I was surprised to learn that the UK retail brokers, such as Hargreaves Lansdown and AJ Bell, were offering access to the IPO. The implication is that Elon Musk is spreading the meagre 5% free float as far and as widely as he can. As we learned last week, the indices will give SpaceX a 3x weighting compared to the low free float, making the index funds and ETFs forced buyers at scale. This will be the largest squeeze in financial markets since the Bunker Hunt Brothers cornered the silver market in the late 1970s.

What to do?

- If you apply for SpaceX, you’ll be heavily scaled back.

- You’ll very likely make short-term gains, due to the squeeze, on a very small holding.

- Take profits quickly.

- At 100x sales, and probably more after the squeeze, bad things could happen to the share price when things settle down.

It’s no doubt a great and innovative company, but this IPO, along with the others that follow, is going to shake up markets like never before.

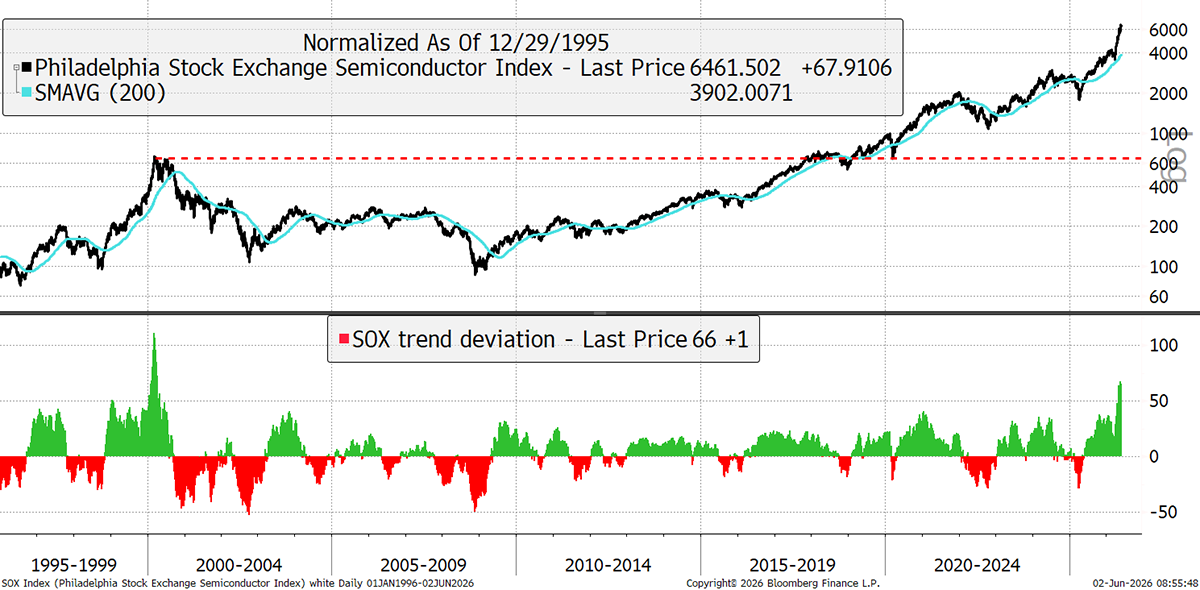

The boom in AI is driving semiconductor demand, with semiconductor stocks accounting for approximately 100% of the market gains. As our work in Global Trends shows, the Philadelphia Semiconductor Index (SOX) boom has gone nuts.

I show the SOX back to 1995, which is 65% above its 200-day moving average. Consider how gold only managed 43% in January. In 2000, the SOX got over 100% overbought, and that took 17 years before the market made another new high in 2017 and is up 10x since.

The SOX Boom

Notice how post the 2000 bust, the SOX returned to 1995 levels during the 2008 crisis. Yet since then, the SOX has risen 60-fold. It’s funny how that happened relatively quietly, while software grabbed the headlines, until the launch of ChatGPT in 2022.

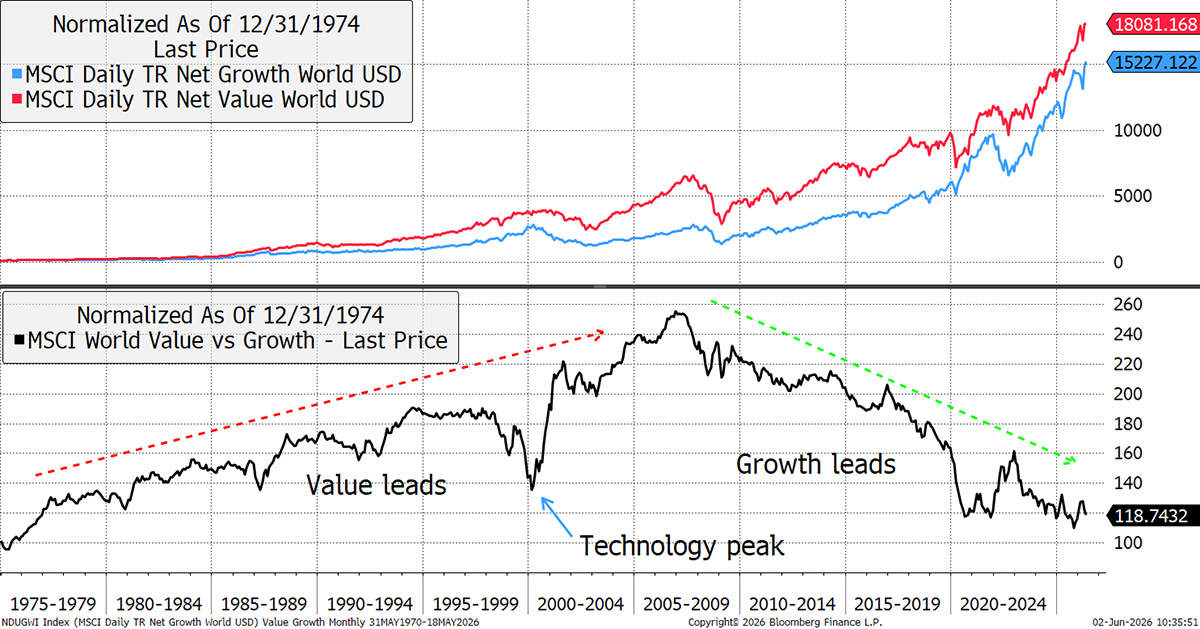

One observation from bubbles is how they suck the life out of things around them. For one group of stocks to surge exponentially, capital must come from elsewhere, therefore driving underperformance in other areas. This we call the anti-bubble, and if growth and risk are the obsession, the defensive areas suffer the most.

This is exactly what we saw in the late 1990s, where value slumped into the technology peak, only to thrive thereafter. Since 1975, value and growth have enjoyed approximately the same returns. According to financial theory, value is supposed to beat growth over the long term, and over 50 years, it is a mere 18% ahead.

World Value vs Growth (inc. Dividends)

Value surged post-pandemic but is now taking a back seat once again while the AI boom plays out. Perhaps value makes a new low versus growth, but don’t be so sure. The forthcoming run of large IPOs is quite likely to end with a hangover.

Knowing it won’t end well is possibly a hindrance to investment success because it holds you back in the boom. But I have found that life in the slow lane, being more concerned with risk than return, gets you to your destination in one piece.

Before we get to this week’s trade, I wanted to check in on the funds.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd