The Might of the Indices

IPOs

In just two weeks, the largest IPO in history, SpaceX (ticker SPCX), will come to market with a mooted valuation of $1.75 trillion. Congratulations to Elon Musk, who is a remarkable chap. No doubt a great innovator who will go down in history, but he is also a market manipulator extraordinaire.

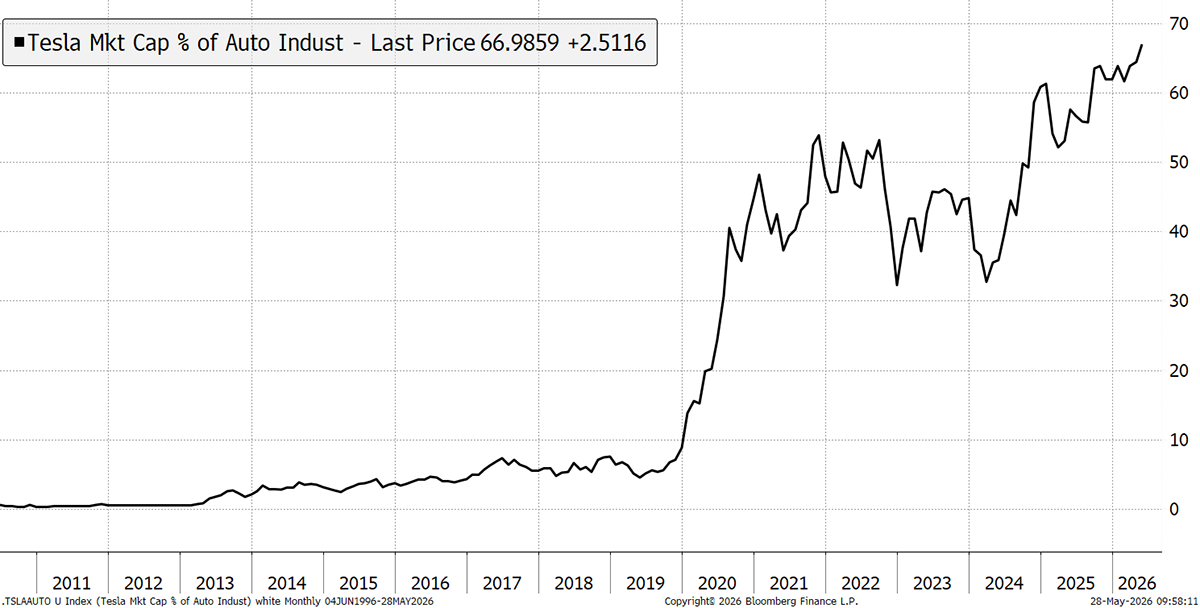

SpaceX will trade on 100x sales. That is, a $1.75 trillion valuation on $18.7 billion in sales in 2025. The company is growing very quickly but remains loss-making. We have seen this before with Tesla, which accounts for 67% of the global automotive industry, worth $2.5 trillion.

Tesla Valuation as a Percentage of the Global Auto Makers

That comes despite Tesla making 1.64 million cars last year in a global market of 96.4 million cars or 1.7% of the total. Of course, to understand Tesla, you have to feel the vibe and leave the financial analysis to dinosaurs like me.

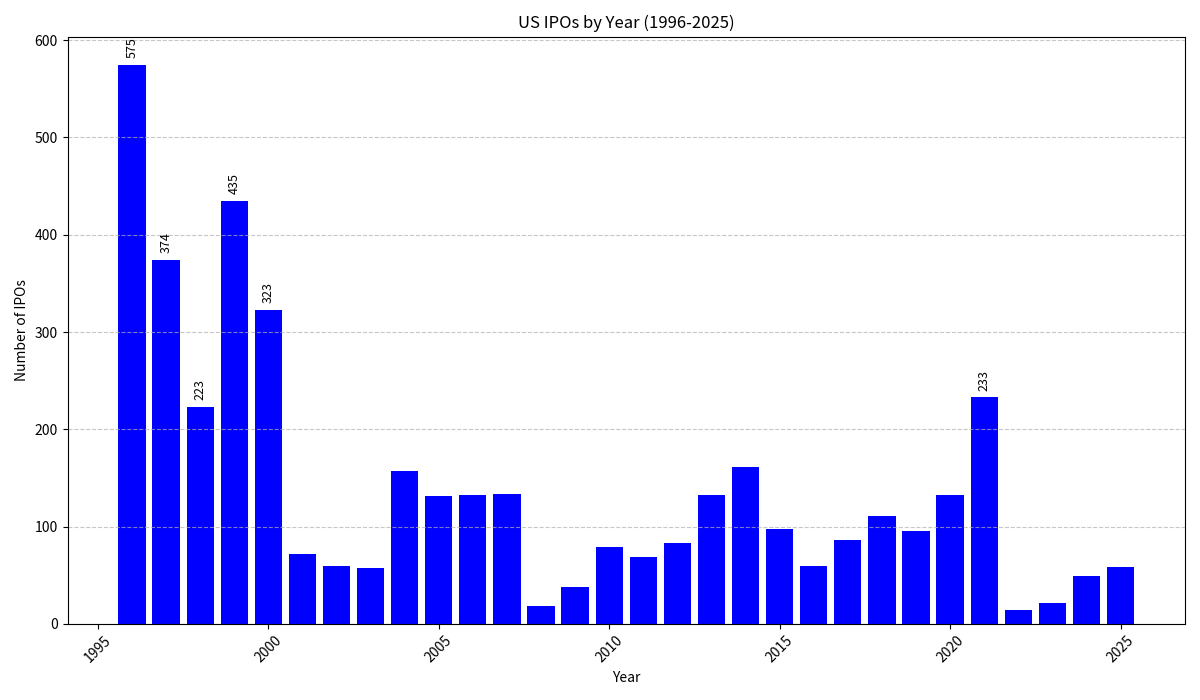

The number of IPOs was plentiful back in the 1990s, only to slump in the 2000s. Private equity became the preferred source of funding for growth companies and venture capital. That has led to companies being floated much later than in the past, and with much higher valuations.

US IPOs by Year - 1996 to 2025

That chart was powered by Grok, which is the AI tool on X. SpaceX includes xAI, which includes X, as well as the space rockets headed for Mars, alongside internet service provider, Starlink (which sits on my roof), Swarm Technologies (satellite communications), and Pioneer Aerospace (parachute/supply chain components). No doubt it is an impressive group of companies. Grok created the chart above in about 10 seconds; something I couldn’t find on Bloomberg.

SpaceX is impressive, but like Tesla, it has governance concerns. As Bloomberg’s Matt Levine wrote,

“When SpaceX is public, Elon Musk still gets to run it however he wants, and he can do weird stuff, and you have to trust him, and if you don’t like it you can’t complain.”

In essence, SpaceX has eliminated all of the main checks on corporate managers, such as shareholder voting and fiduciary duties, so that Musk can operate with a free hand.

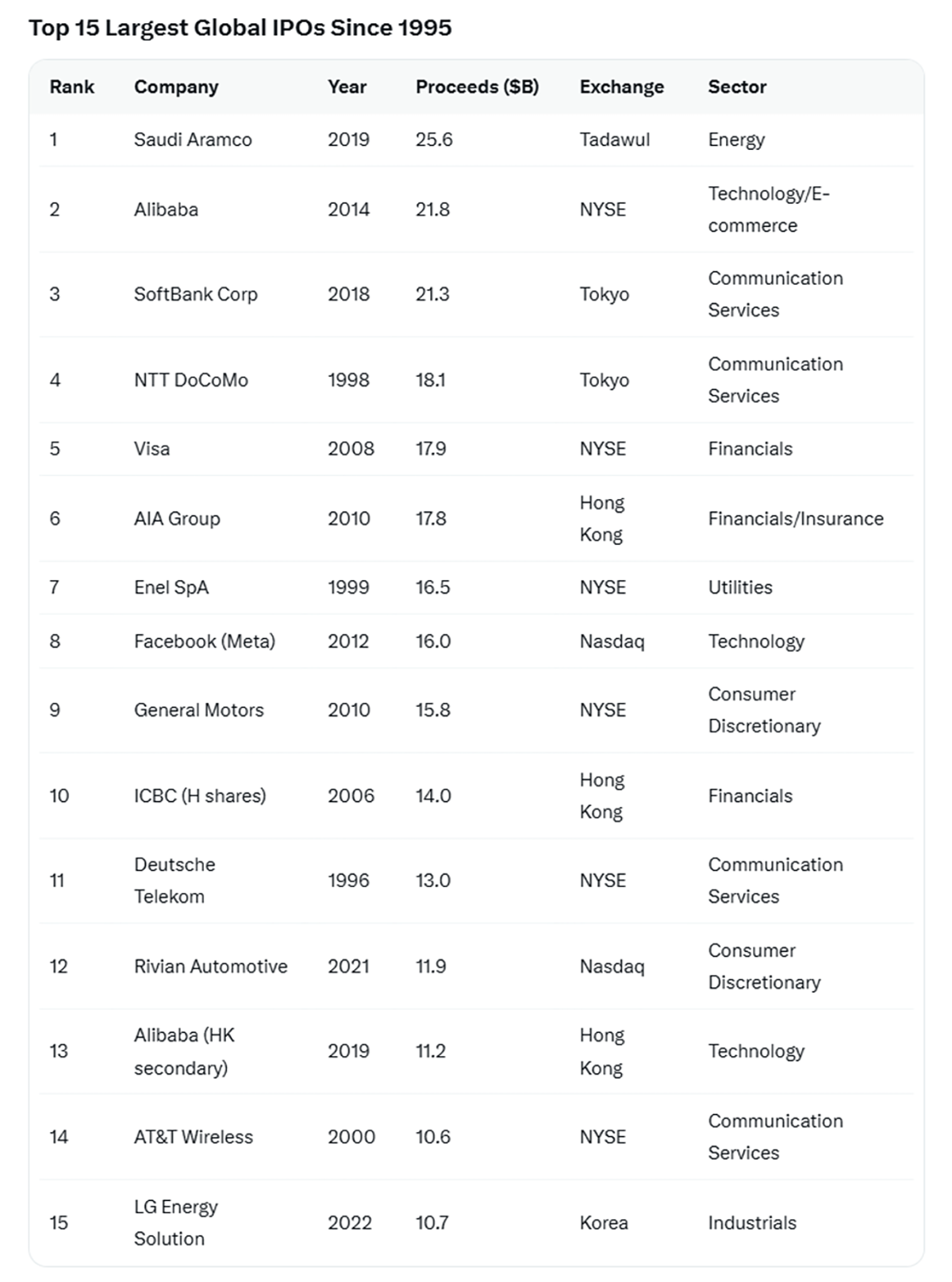

The previous largest IPO was Saudi Aramco, with a claim to the richest oil reserves in the world. They raised $25.6 bn with a modest free float of 2.5%. That means the Kingdom of Saudi Arabia retains 81.5% of the shares, and the public investment fund retains 16%, leaving just 2.5% for the rest of us. Alibaba and Softbank raised $21 bn, with the others in the teens.

Top 15 IPOs since 1995

This highlights why the SpaceX IPO is so important because the target raise is circa $75 bn, which is nearly 4x the previous record. Like Aramco, the company is only selling up to 5% of its shares, leaving 95% in the hands of Musk (42%) and other employees and institutional investors.

Free Float

That means when it floats, SpaceX won’t have very many shares available for the market to buy. According to Levine, from about 2017 until 2023, some big index providers tried to exclude new companies with dual-class stock that gave their founders voting control, on the theory that that’s bad governance and index funds shouldn’t have to buy companies with bad governance. Some indices, most notably the S&P 500, have profitability requirements, on the assumption that companies that lose money are bad and index funds shouldn’t have to buy companies with bad earnings, which kept Tesla out of the S&P 500 for years.

In the good ol’ days, most market indices adjusted for free float, giving a lower weight to companies with fewer available shares. For example, family companies with high family ownership had a lower weight in the index than their market cap warranted. For example, in the French CAC index, LVMH, L’Oréal and Hermes are the largest companies by market capitalisation. LVMH is worth €240bn, L’Oréal €206bn, and Hermes €172 bn. The CAC has a combined market cap of €1.8 Tn, and so they should be allocated at 13.3%, 11.4%, and 9.6%, respectively.

Yet the CAC rules discount the free float, so their actual weights in the index are 6.5%, 4.8% and 2.8%. That is a significant reduction, especially for Hermes, which is 66.7% owned by the family.

These days, the index funds and ETFs have ballooned to $30 to $35 trillion. They are not controlled by active fund managers but have a duty to track their respective indices. That puts the index providers like MSCI, S&P, Nasdaq, and FTSE into a strong position. Their index rules, which were once a nerdy back-room affair, are now front and centre in controlling global capital flows.

The FT reported that the rules, implemented this month by Nasdaq, mean billions of dollars of passive money will automatically flow to the three companies shortly after they go public, driving their share prices higher while forcing investors to sell other stocks.

The tight allocation by SpaceX, under the old rules, would ensure a low free float, as we saw with Hermes. But Nasdaq has loosened its rules to attract SpaceX, fearing it would list on the New York Stock Exchange instead. SpaceX will join the Nasdaq 100 index after just 15 days and will be given an index weighting equivalent to three times the value of the shares floated.

JPMorgan estimates that passive investors would have to sell $95bn of the eight biggest current tech stocks on Wall Street. Peter Haynes, head of index and market structure research at TD Securities, said,

“The SpaceX IPO, and the follow-on release of locked-up shares, like no other single index event in recent history we have been overwhelmed by institutional investors asking about the IPO, the name, the size, the impact.”

It doesn’t end there because the list of IPOs we may see in 2026 includes other major companies, such as OpenAI and Anthropic, on similar terms (source: Grok).

IPOs in 2026

| Company | Sector | Est. Market Cap (Bn $) |

| SpaceX | Space & AI | 1,750 |

| OpenAI | AI | 850 |

| Anthropic | AI | 600 |

| Stripe | Fintech | 159 |

| Databricks | AI | 134 |

| Anduril Industries | Defence | 60 |

Anthropic was founded in 2021 by seven former OpenAI employees, who split off to develop a model with a greater focus on safety. Today, Anthropic’s frontier model, Claude, stands out for its transparency. It focuses on automating coding, which has sent shock waves through the coding industry, as one of the great high-paying professions, worth $600 bn per year, has been superseded. Claude Code agents write 90% of the code for some of Anthropic's products, and it has quickly become the market leader.

OpenAI is targeting a public listing as early as September, at a valuation of up to $1 trillion, just above its last private round of $852bn. Yet OpenAI remains deeply unprofitable. The company’s need for data centres, chips, and cloud capacity means it needs to keep spending, and investors will have to decide whether they believe the company can turn that spending into durable profits.

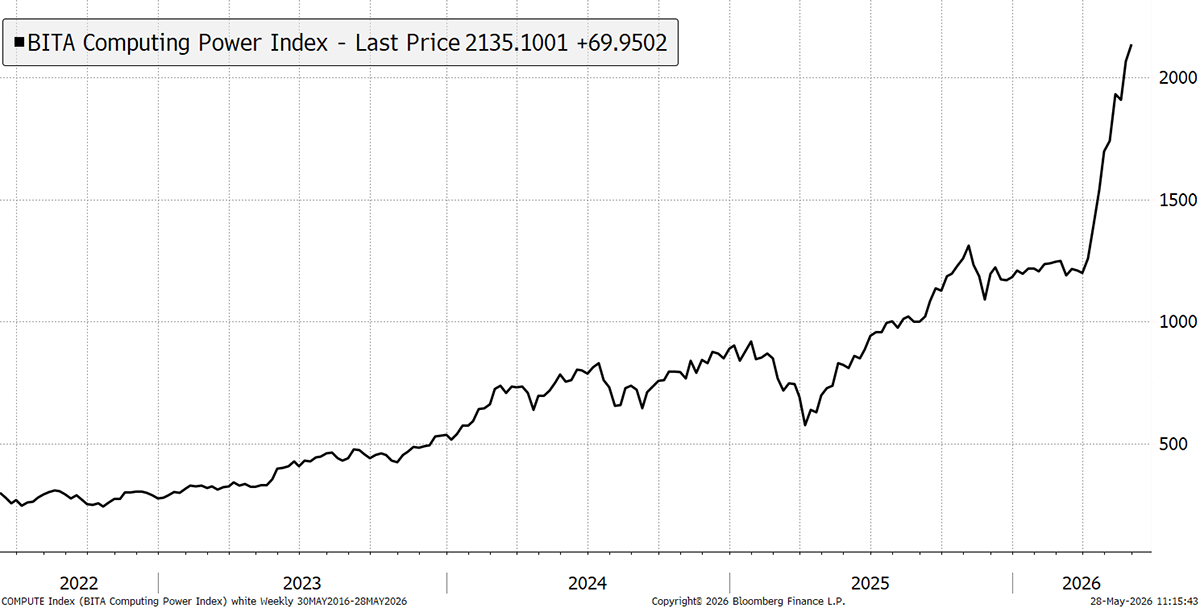

The AI industry (and associated industries) is spending $1 trillion on capital expenditure in 2026, driving up the costs of chips and datacentres. We have seen a boom in semiconductor stocks, alongside computer hardware. The cost of running AI datacentres has exploded.

The Cost of Compute

While few doubt the benefits of AI, the costs are spiralling out of control. This is a new problem for the IT industry, as they have become accustomed to high growth and high margins. AI takes them into the physical world, with high demands for energy and infrastructure.

The late deputy chairman of Berkshire Hathaway, Charlie Munger, once described Coca-Cola as the greatest company in the world. It sold low-cost sugared water with high margins worldwide. There was no better business model until software came along. That saw lines of code, with near-zero marginal costs, sold to a large audience. Then, when the internet came along, it could sell even more code to an even wider audience.

AI has threatened that because more people will be able to write their own code, meaning that competition in software will explode. That has already put downward pressure on the software stocks, as they are no longer seen as bulletproof business models. Munger will end up being right again, as we all hanker after shares in the tech-proof Coca-Cola.

Equity Supply and Demand

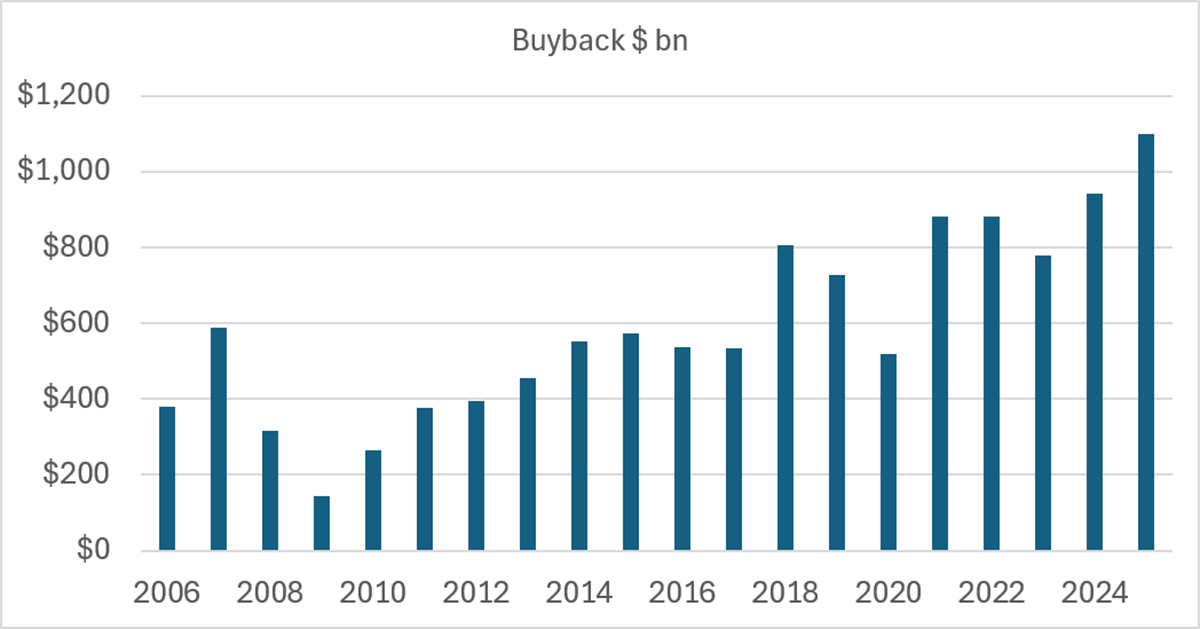

One of the drivers, especially of US equities, has been share buybacks. This has averaged around $500bn per year, which has effectively reduced the supply of shares to the tune of $11.8 bn since 2006. In the dark years like 2008 and 2020, those buybacks went a long way, as they were buying stocks on the cheap. Today, the same can’t be said of the estimated $1.1tn of buybacks in 2025, which have withdrawn equity at high prices.

Buybacks

But at the highest level, if there is X flowing into stockmarkets due to savings, and Y being withdrawn due to drawdowns, the difference determines whether the market rises or falls. Buybacks have been a positive force on the market, as they have tightened equity supply.

With a resurgence of larger-than-usual IPOs, equity supply will start to rise. This will be a trickle at first, but the companies mentioned earlier will be valued at circa $3tn, and there could be many more if SpaceX is well received. Just consider how much stock the private equity industry would like to sell.

This will be front-page news over the coming weeks as Musk becomes the world’s first trillionaire. He will be able to afford a new house, as he currently lives in a $50,000 prefabricated home, which he rents from SpaceX. No yacht, no mansion, but he does spend quite a lot of time in his private jet. He just wants to enable life on Mars.

The Might of the Indices

What is fascinating is that the market indices were designed as tools to gauge performance. The first was the Dow Jones Industrial Average, taking the average daily change of the top 30 companies. Then came the arithmetic weighted indices based on market cap, such as the S&P 500.

That was tracked by John C Bogel, the founder of Vanguard, who popularised the index fund. He reckoned that most investors lagged the index, so why not match it and focus on reducing costs? Today, his Vanguard S&P 500 ETF manages $981 bn, and charges 0.03% per annum. Index funds and ETFs have become a vast industry and a dominant force in stockmarkets.

That is the problem. Goodhart’s Law is the principle that "when a measure becomes a target, it ceases to be a good measure." Originally coined by economist Charles Goodhart in 1975, it describes how using a metric as a goal often incentivises people to manipulate the system to hit that specific number, destroying the metric's original value. As I wrote earlier, the index rules used to be nerdy small print but have become masters of the universe.

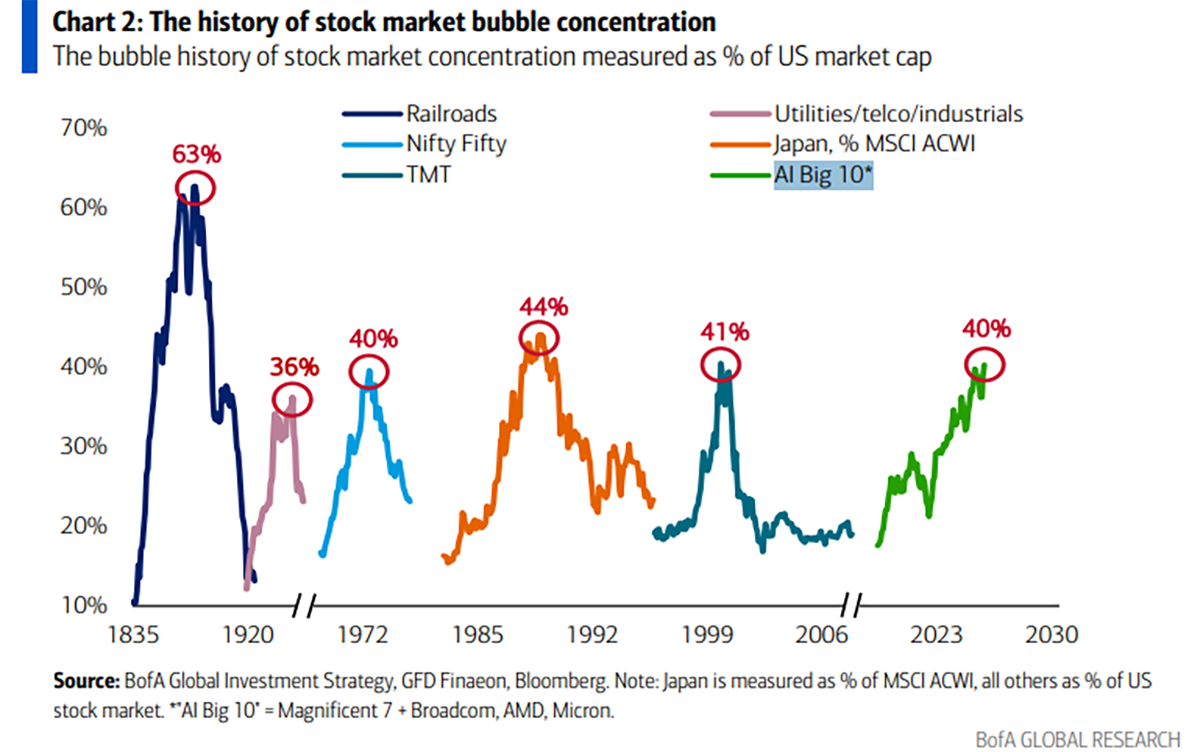

The AI boom is being sold to the market at sky-high prices, and the resulting concentration in market indices matches that of major historical bubbles.

Bubbles Through Time

It is a cause for concern for investors who participate at the sharp end of the market. But they too can benefit as did the late Sir John Templeton. At the age of 88, he famously shorted the dotcom stocks in 2000. His strategy was to sell short days before the lock-up periods expired, when the pre-IPO investors and employees were free to sell. He believed they wanted out and would scramble for the exit. Sir John was on the other side, collecting a cool $90 million in his retirement before nipping out for a swim in the Bahamas.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd