Crunch Time

Trade in Whisky;

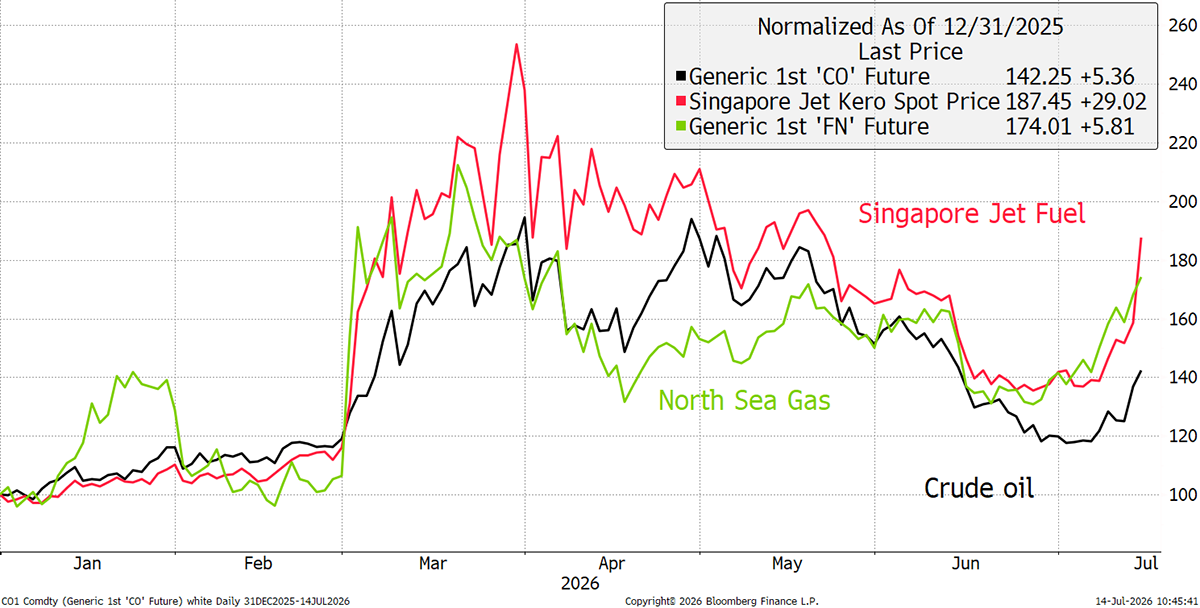

The war resumes. According to Bloomberg data, one ship passed through the Strait of Hormuz yesterday, while energy prices are rising again. I show crude oil, jet fuel, and North Sea natural gas since the start of this year.

Crude Oil and Jet Fuel

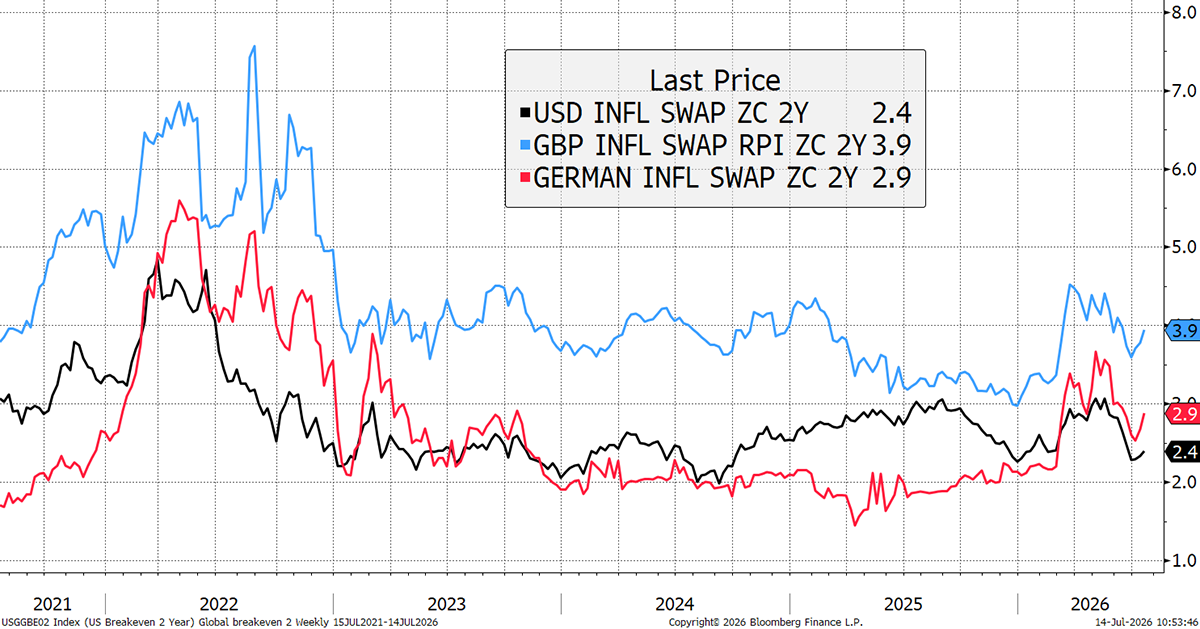

There seems to be no end to this conflict as trust has broken down. If the Tanker Wars of the 1980s are any guide, they went on for years, flaring up periodically. The difference between the end of February and today is that oil reserves have been severely depleted. What has become clear is how the stress is most focused on jet fuel, diesel, and North Sea gas, the latter of which largely sets UK and European electricity prices. It means inflation expectations are rising again, and rate cuts are, once again, unlikely.

Two-Year Inflation Expectations

The Middle East isn’t just an oil producer; it has also become the largest exporter of refined products. Gulf fuels are heavier than US fuels and yield much more jet fuel and diesel per barrel. As these fuels have risen faster than crude, that has boosted refining margins.

This week, I am adding a refiner to the Whisky Portfolio. I believe this makes more sense than a producer because it is focused on the pressure point. It also complements our existing position in crude oil exposure, which continues to benefit from the backwardation, giving us an additional and sizeable return over and above the spot oil price movements.

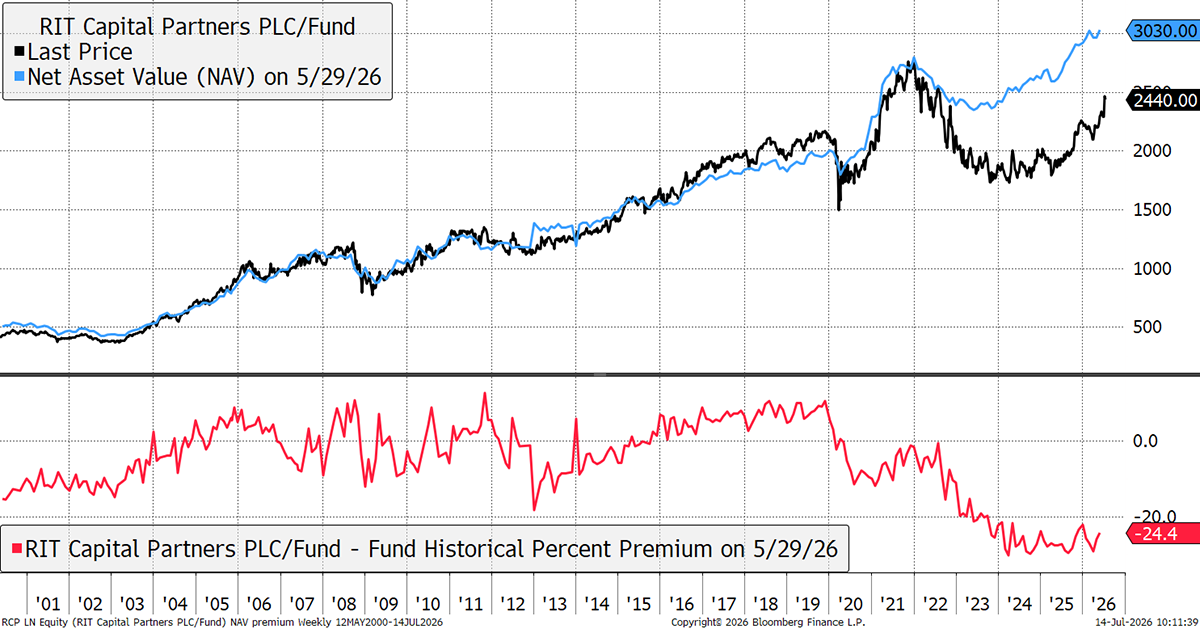

Before I get to that, I wanted to check in on RIT Capital following their announcement. I received several emails about it.

RIT Capital (RCP) Tender Offer

RCP have announced a series of measures to narrow its discount to net asset value. From their site:

- A tender offer for up to £300 million of Shares at a 15% discount to preliminary NAV as at 30 June 2026, which is expected to be meaningfully accretive to NAV per share for continuing Shareholders;

- A review of dividend policy, including consideration of an increased dividend from 2027;

- The continuation of the Company’s active share buyback programme; and

- The continued application of a disciplined capital allocation framework focused on long-term value creation.

I added RCP in January 2024, as I felt the discount was wide, offering a very attractive entry point. I added more last September. The NAV has done quite well, while the discount has narrowed, making this a strong performer.

RIT Capital: Net Asset Value

The series of measures taken by RCP is well-intended. They want to get rid of the discount as much as we do. I think the discount will disappear over time as the share price returns to par or NAV.

RCP have already bought back 12.5% of their shares over the past five years, and they propose to buy back a further 10% via a tender offer. If we take the shilling at a 15% discount, there is a modest uplift. But bear in mind the share price has already risen by 7.6% last week to reflect some of that. Furthermore, the buyback is for 10% of the overall stock, and so shareholders may not get filled.

The real issue is whether we want to own this fund or not. If shareholders want to sell, then the tender allows a good opportunity to do so. If we prefer to hold, then selling a few shares at a slightly higher price makes no sense.

I like RCP as it is an ideal holding for Soda. It is well-managed, diversified, and dynamic, with the occasional surprise such as SpaceX. With the NAV at 3030p and the price at 2440p, there is still a 25% upside plus fund returns by doing nothing. That may take longer to come to fruition, but the board members are motivated.

Given that I intend to hold RCP for some time, I opt to take no action.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd