Smaller Companies and Technology in Emerging Markets

Trades in Whisky and Soda;

The S&P 500 made an all-time high last week, once again on hopes of a short war. That and an injection of money into the financial system. The other major countries that managed to make a new high were Italy, Brazil, and China. This week, we make a change in each portfolio to capture the developing investment themes.

A short war is possible, but it is far from assured, despite the optimistic messaging. The recent ceasefire ends tomorrow, and while the US has declared the Strait of Hormuz as open, Iran has kept it closed. There are questions surrounding who governs Iran, which makes negotiations difficult. Even if the war draws to a natural conclusion, we still face a logistical crisis in Asia, Africa, and Europe. The Americas, on the other hand, are more insulated given the continent’s energy security.

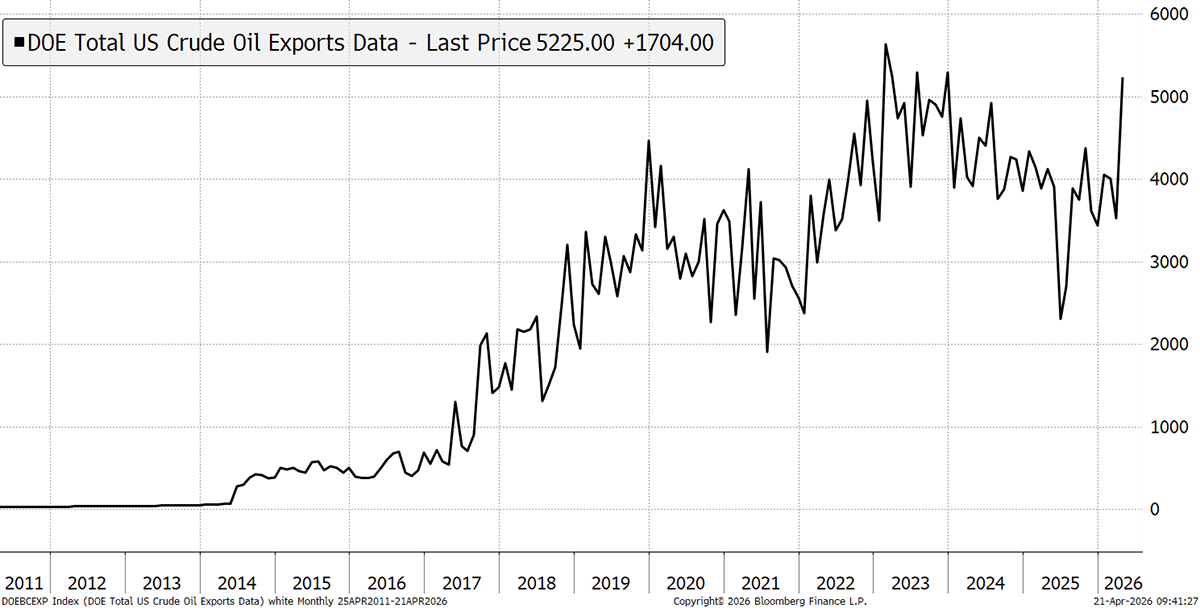

Despite the most important global energy source being disrupted, the oil price remains relatively calm despite impending shortages. Hardly headline news, but my local garage ran out of diesel yesterday, which brings it close to home. Diesel and kerosene (jet fuel) are similar grades, and it has been well flagged that the airports will face shortages in the coming weeks, whether the war ends or not. At the very least, we should be prepared for flight cancellations.

So why is the oil price so complacent? As we have learned, there are many different oil prices, depending on which product, in what location, and when. Then there is demand destruction, as a high oil price has put off non-essential buyers. Another alarming reason is that the shortage of crude from the Gulf has meant that some refineries haven’t been able to buy and have therefore “reduced demand” despite being desperate for product. Then there’s the USA, where the empty tankers are headed, ready to return with richly priced crude oil and refined products for the rest of the world.

USA Crude Oil Exports

The other reason is the powerful media effort that convinces markets that this remains a short war. Every time the oil price ticks up, you can be sure that an announcement will soon follow.

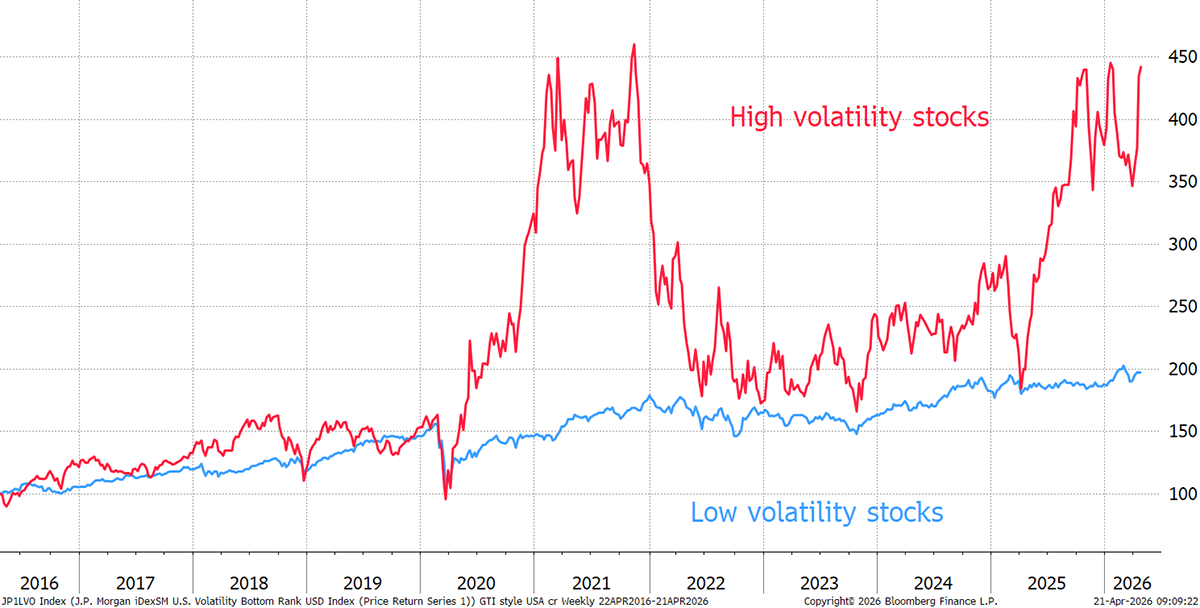

The April rally has been led by volatile stocks, which had looked like they had peaked. This year, I have taken steps to calm the portfolios by increasing allocations to low-volatility stocks. Traditionally, they are the place to find shelter when the pressures build, but instead, risk has returned with a vengeance. For example, the heavily indebted Avis Budget (CAR) is up 317% in April. Allbirds (BIRD), a shoe company, rose 917% last Thursday as it announced a shift from shoes to AI. The market regime has turned back to Risk-ON mode at speed.

High vs Low Volatility Stocks

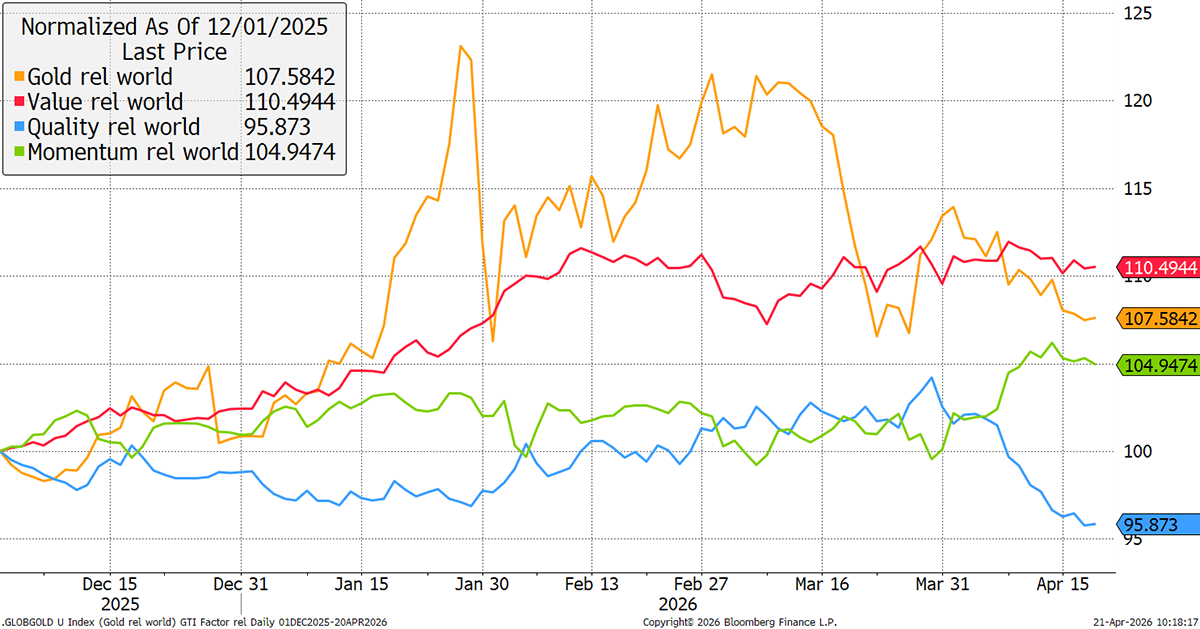

The key equity factor groups that reflect the fortunes of the Money Map now reflect bullish conditions. Growth or momentum (green) has been leading the market, while value has held up (red). The defensive groups, gold and quality, have lagged behind.

Global Factors vs the World

Focusing on the momentum effect, the leaders (past year’s best performers in blue) have shot out of the gates in April, leaving the losers (past year’s worst performers in red) for dust. This signals that financial markets are enjoying the recovery more than the real economy, where the problems lie.

Winners vs Losers

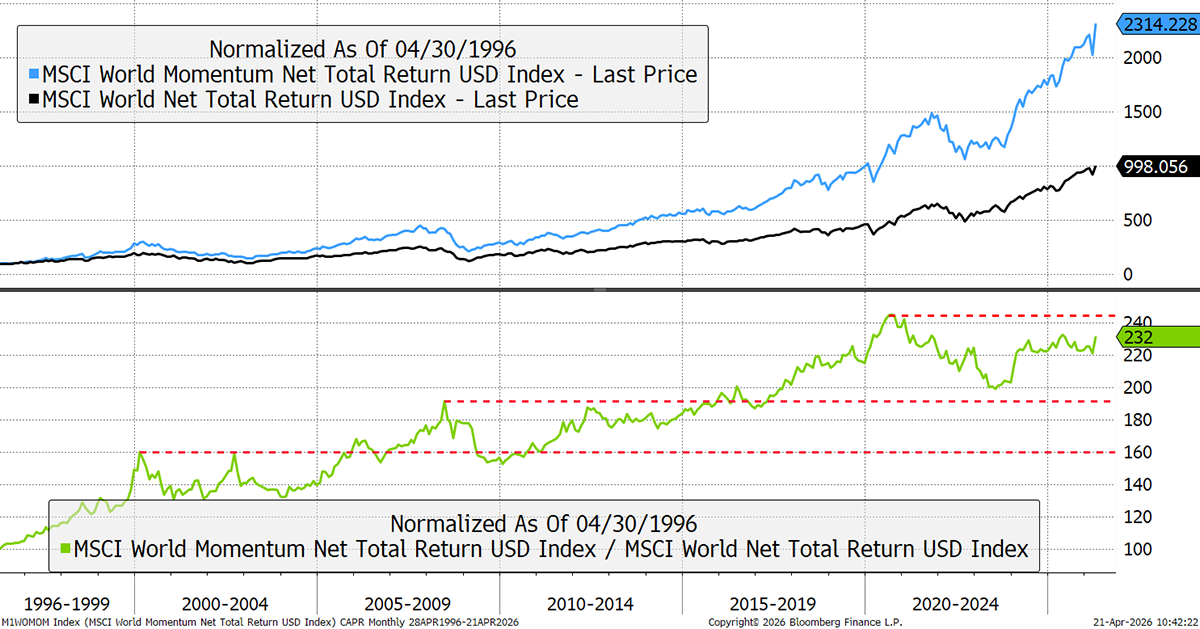

As per my recent flash note, I highlighted some of the key charts to explain this phenomenon. I will show this once again, which compares global equities to the MSCI Global Momentum Index. Despite momentum being a strategy that has been more than twice as strong as the market, it tends to move in bursts. The 1999 peak wasn’t exceeded until 2006, the 2008 peak wasn't exceeded until 2016, and the 2020 peak is still in progress.

Momentum vs the World

Why do I think this is another momentum market? Because the market has shifted into a higher Risk-ON environment, where there is a clear differential between the leadership and the market. The prevailing leaders relate to technology, financials, and high-end industrial companies, which are high-margin businesses and relatively insulated from the troubles of the real world. The rest of the market, on the other hand, has to face energy shortages, potentially higher food costs, layoffs, and a bruised consumer.

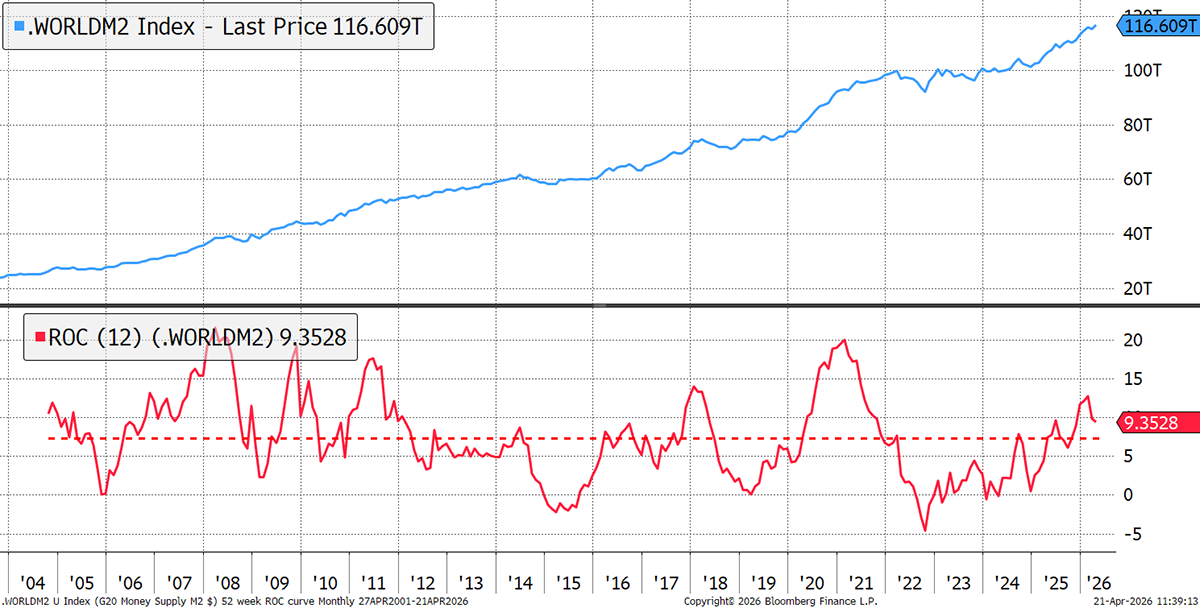

Add to that a resurgence in the money supply, which typically coincides with momentum rallies. With fewer attractive stocks to buy, the excess money becomes more focused on a smaller section of the market, driving it more aggressively. As a result, momentum rallies, while infrequent, can be powerful while they last. The money supply is above average once again, and indications show a further pickup will likely be published by the Fed next Tuesday. The liquidity withdrawn earlier in this year has been returned.

World Money Supply

I have made some further small changes to the portfolios to ensure we participate in this increasingly likely momentum market scenario, and I will make more changes as I find them. It is not just momentum that benefits from a market with plentiful liquidity, but small-caps and selective growth themes as well.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd