Bonds and Politics

As inflationary pressures mount in this commodity bull market, bond yields keep making new highs, squeezing public budgets. So far, equities have proved resilient, but how much longer will this last?

Bonds and Equities

I show UK equities and gilts, total return (including dividends), since 1999.

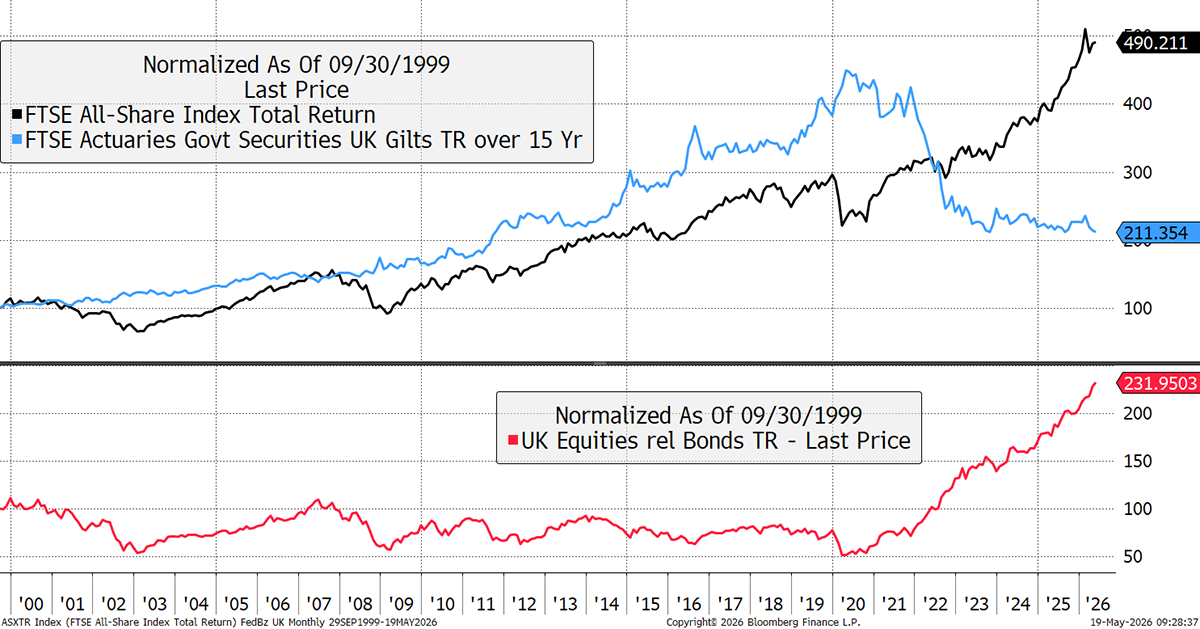

UK Equities vs Gilts

The outperformance of UK equities over bonds in the last five years has been truly staggering, and even more so in the USA. Much of that is deserved, as gilts offered poor value until recently. After the 2008 financial crisis, gilt yields fell, while prices rose, boosting returns. Then, after the pandemic, gilt yields have risen, while prices have slumped.

The FTSE All-Share Index has generally paid a dividend yield of around 4%, typically lower than that of gilts, as equity investors should expect higher growth. Between 2011 and 2022, UK equities have had a higher yield than gilts.

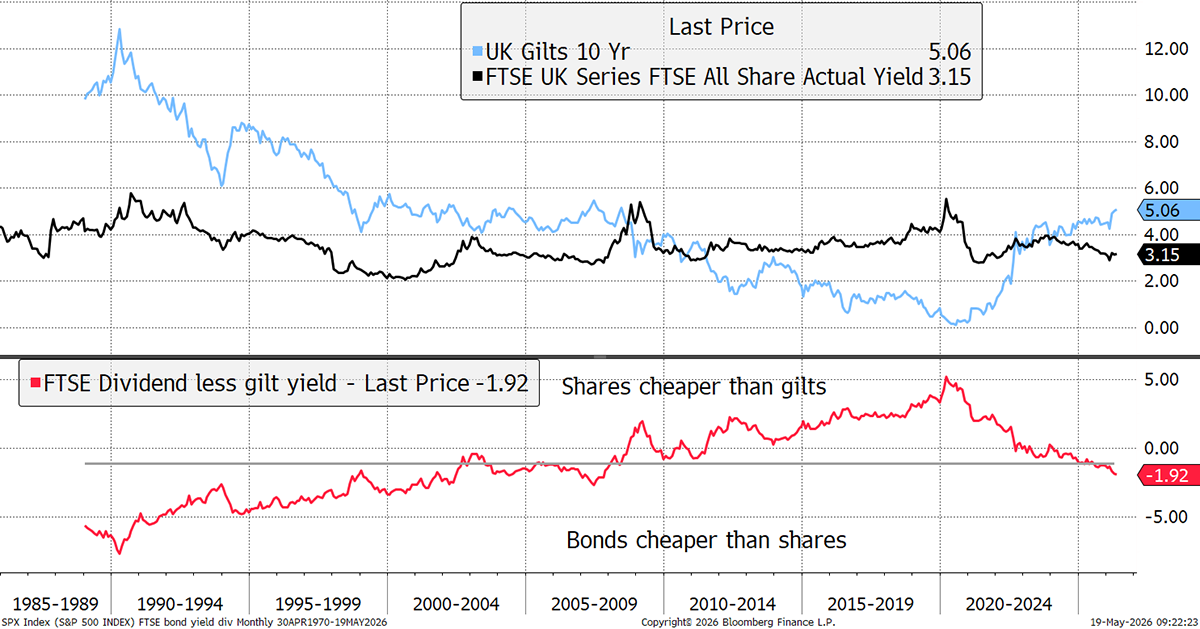

UK Equities vs Gilt Yields

We now find ourselves in an era where gilts yield more than equities, which was the prevailing condition pre-2008. Before 1960, it was the other way around. However, because equities offer growth, gilts yielding more is something we have become used to as people have paid up for equity growth. Perhaps there was a time, in a more uncertain world, where the safety of gilts commanded a premium over the uncertainty of equities.

Politics and Budgets

UK politics has become lively again. In a few weeks, there’ll be a by-election in Makerfield as Labour MP Josh Simons gives way to Andy Burnham, who will then challenge the prime minister, Sir Kier Starmer. Others will be throwing their hats into the ring.

It will be colourful, because lifelong Labour supporters who want Starmer to stay in power will have to vote for another party. In the meantime, Reform will be out in force to take the seat. If Labour loses, it will be a huge embarrassment, but perhaps the gilt market will take it well, as it will avoid a shift further to the left. Yet already, the leftist candidates have shifted their stance from defying the gilt market to accommodation. The message is clear: when a nation has borrowed heavily in the past, it must repay its debts. Whoever takes charge, this is no time for heavy spending policies.

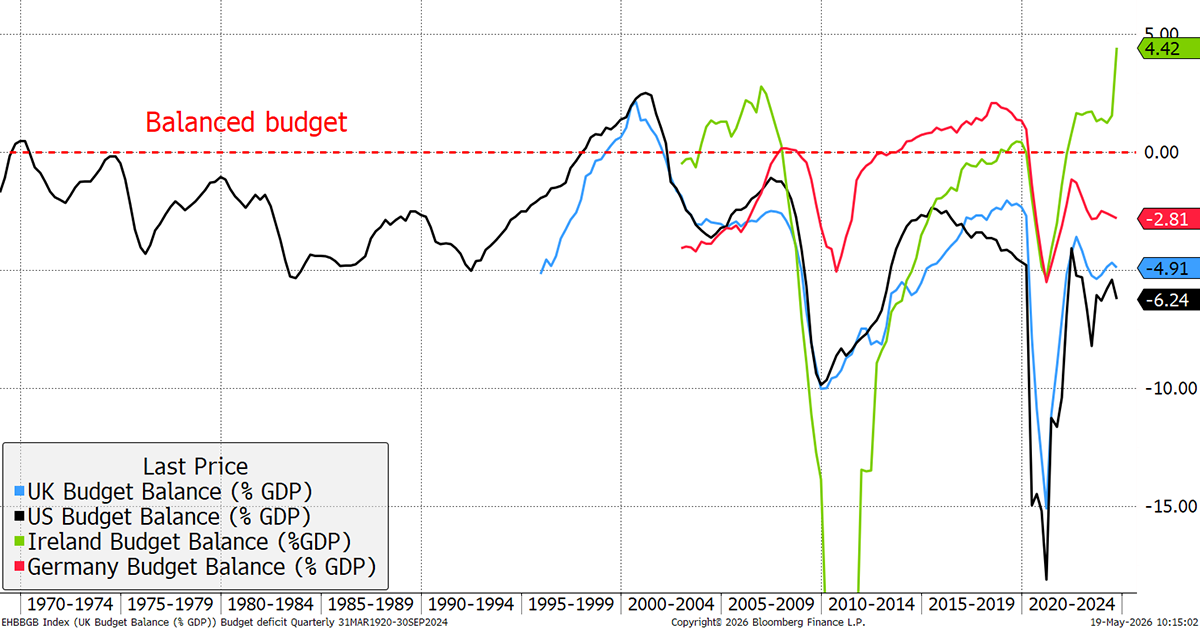

For some reason, politicians, of all parties, have been rewarded for spending money they don’t have, rather than balancing the books. The UK (blue) last balanced the budget under John Major, while the US did so under Clinton. That was an era of fast-growing tax revenues in a thriving economy. It has been downward ever since deficits have become the norm.

Budget Spending as a Percentage of GDP

There has been little effort to balance budgets since the pandemic, except in countries like Ireland (green) and others that got into difficulties post-2008, such as Spain and Portugal. Ireland is the poster child for a responsible government. Their debt-to-GDP spiked to 120% during the euro crisis of 2012. However, today it is just 33%, which is close to where UK debt levels were in the late 1990s.

Germany is spending more on defence, while its economy has been weakened by deindustrialisation policies. Meanwhile, the UK and the USA are seeing widening deficits at a stage of the cycle when they should be narrowing. Aren’t we supposed to fix the roof when the sun is shining?

The problem the UK and the USA now face is a structural deficit on top of a rising interest bill. The interest rates are rising because yields are rising, as the era of cheap debt is over. Perhaps it made sense to borrow to make long-term investments when debt was cheap, but sadly, there were not many investments, just high spending. The cost of servicing that old debt is rising, made worse by inflation.

Inflation was coming down until the war in Iran, but has turned up again, more so in Europe than in the USA. I believe that with a free-floating exchange rate, as in the UK, USA, or Japan, bond yields are primarily driven by inflation. In fixed-rate regimes, such as Europe or the Middle East, credit risk is a greater concern. In other words, if the markets lost faith in the UK’s ability to repay its debts, the bond yield would reflect higher inflation, and a falling pound would reflect deteriorating international credibility.

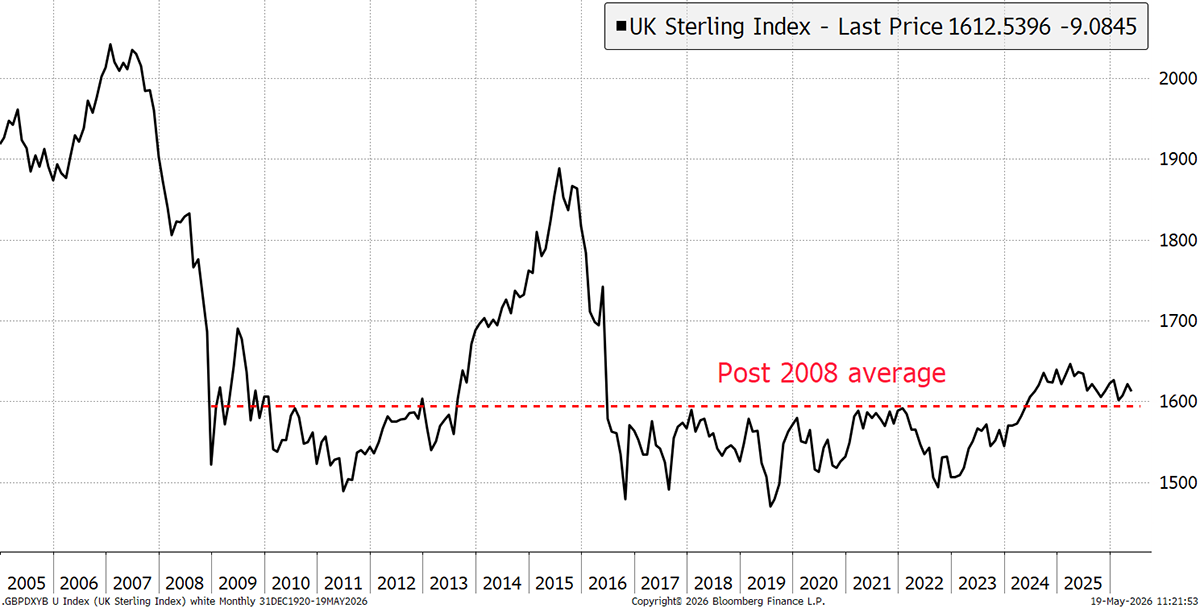

In a piece of good news, the pound is not dying. I show it against the leading currencies, including the Chinese Yuan and the Indian Rupee. It has been average since 2008, following a devaluation after the 2008 crisis. There was also the Brexit crash in 2016, but that correction was already underway before the vote, following an unsustainable rally. We’ll never know what a Remain outcome exchange rate would have looked like, but today the pound trades above its 2008 average. It may start to fall from here, but it hasn’t yet.

The Pound – Trade-Weighted vs Leading Currencies

Structural deficits are unwelcome, as they simply make the long-term situation worse. Today’s debt must be paid for by the next generation, and it surprises me how few politicians, on all sides of the political spectrum, see it that way. The greatest gift we could give future generations is financial stability.

The Commodity Squeeze

Things are not just getting worse due to deficits, but also due to rising inflation. Inflation is currently being driven by rising energy prices, where the problem could be much worse than what current oil prices reflect. Food and energy prices have been restrained because last year was a bumper harvest, and oil inventories have been relatively high, cushioning the supply crunch.

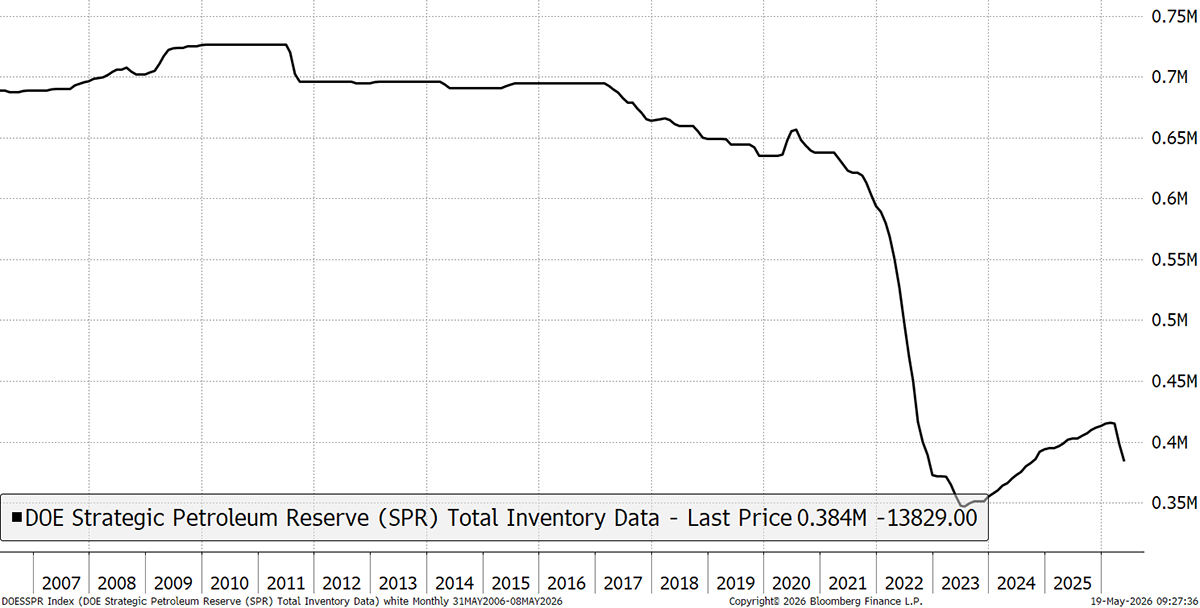

For example, the US strategic oil reserve had been recovering following the war in Ukraine, when 350 million barrels were depleted. That recovered slightly in 2024/5 but is now falling again.

US Strategic Oil Reserve

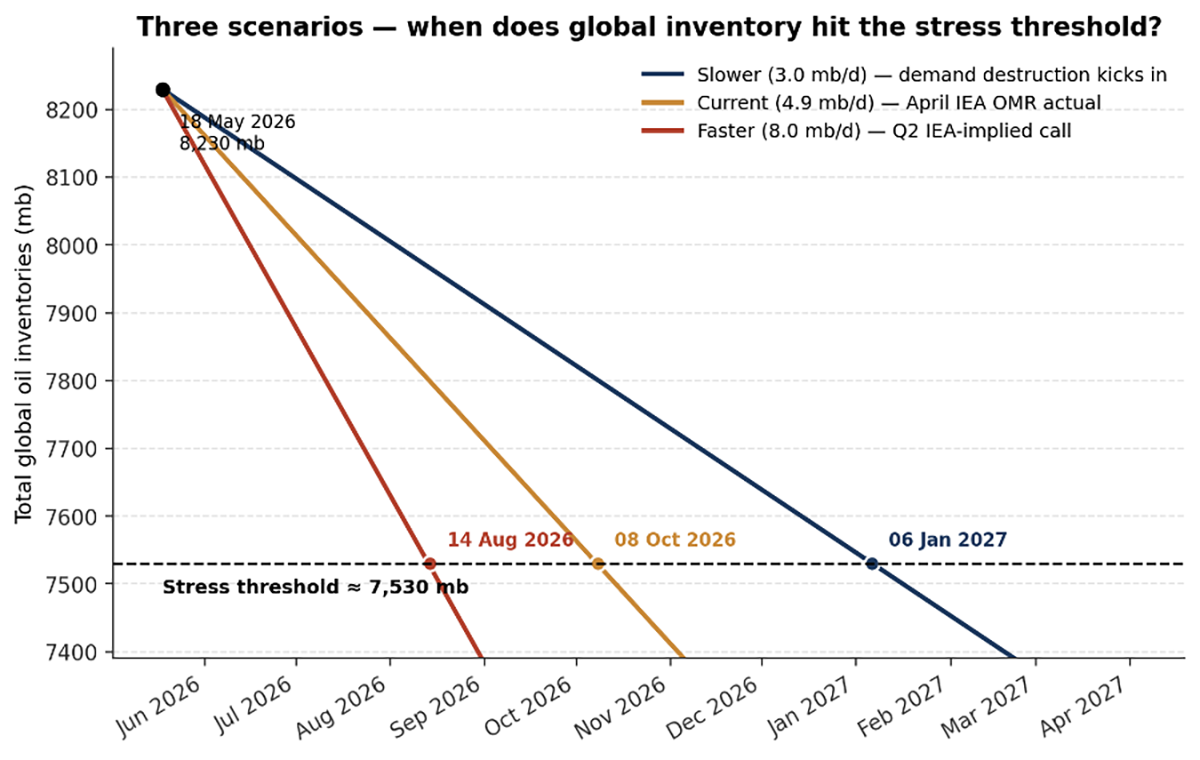

With a little help from Claude AI, we have looked at some scenarios to estimate when usable global inventories might hit rock bottom, at which point the system comes under stress. The early scenarios point to mid-August, with the latter towards the year-end.

Oil Inventory Scenarios

Jeff Currie, the former Head of Commodities at Goldman Sachs, has been vocal about this. He talks about a deficit versus a shortage. We are currently in a deficit, but the real pain doesn’t kick in until there’s a physical shortage.

Ryanair CEO Michael O’Leary doesn’t think his airline has a problem because they have hedged 80% of its oil needs into 2027. He talks of a steady supply from Norway, the USA and West Africa. That’s fine, and he wants to calm customers so that they book seats. While Ryanair has got it right, what about the others? Not every CEO is as brilliant as O’Leary. If the airlines keep on flying, the squeeze will have to shift elsewhere. Someone is going to have to do without the energy requirement they had before this crisis began.

Then there is the Middle East itself, which has had no petrol dollars for 79 days. At what point does that become a problem? I can only presume, with the help of insiders, that cautious depositors are shifting their funds out of the region. How does an oil crisis become a financial crisis? This could be it.

Portfolio Commodity Exposure

I have spent much time deliberating on how much commodity exposure is enough. My motivation is not so much to see the portfolios profit in a negative environment, but to protect them when things start to go wrong. We have direct commodity exposure and much more indirect exposure, with a resounding and comforting level of diversification.

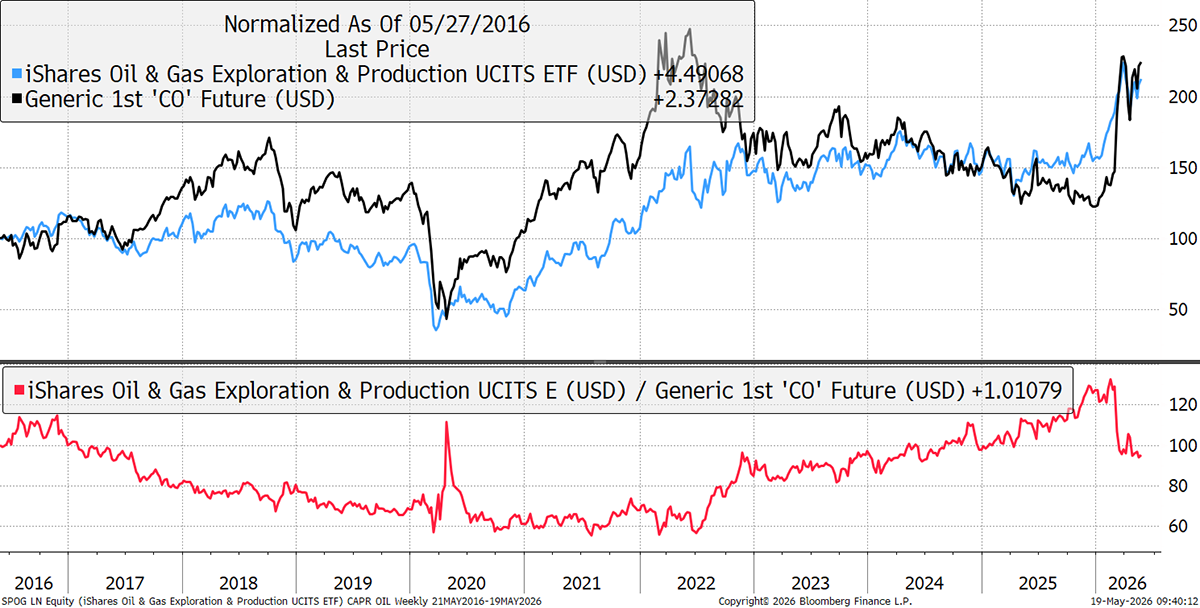

One thought has been to add to oil stocks despite it feeling late in the day. Something that holds me back is that oil stocks have low sensitivity (or beta in market jargon) to the oil price. Look at SPOG, our Energy Sector ETF (including dividends), compared to oil over the past decade. The performance has been the same: oil has beaten SPOG during rallies, while SPOG has proved more resilient during falls.

Oil Stocks vs Oil

It is curious how SPOG has underperformed oil so badly during the recent price surge. Presumably, the stocks are pricing a high oil price that will not last, just as they did in 2022. It means if your portfolio wants to benefit from a further oil shock, you need to own oil rather than oil stocks. On the flip side, the oil stocks pay dividends and will be more resilient when the price turns down.

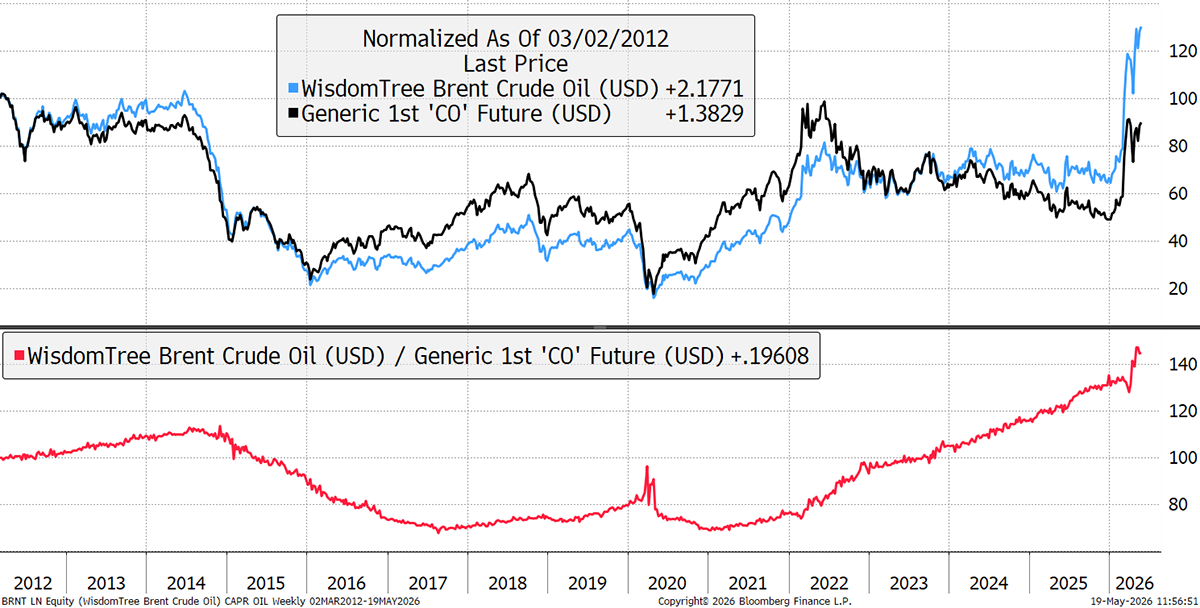

Another advantage of oil futures is the positive roll yield you can earn when the price is in backwardation. That means oil today costs more than oil in the future, so by holding futures via an ETP, the investor outperforms spot crude oil. This has been true since 2021, when the price last surged. Naturally, when the spot price is below the future price, the market is said to be in contango, and the ETP lags the oil price.

Spot Brent Crude vs Oil Futures

The current backwardation is massive, so holding an oil ETP makes a lot of sense at this time. I am even tempted to increase this position, but I need more evidence of an impending crisis before I do. It certainly makes sense as a superior hedge to oil stocks at this time, as the market is paying you to take risk.

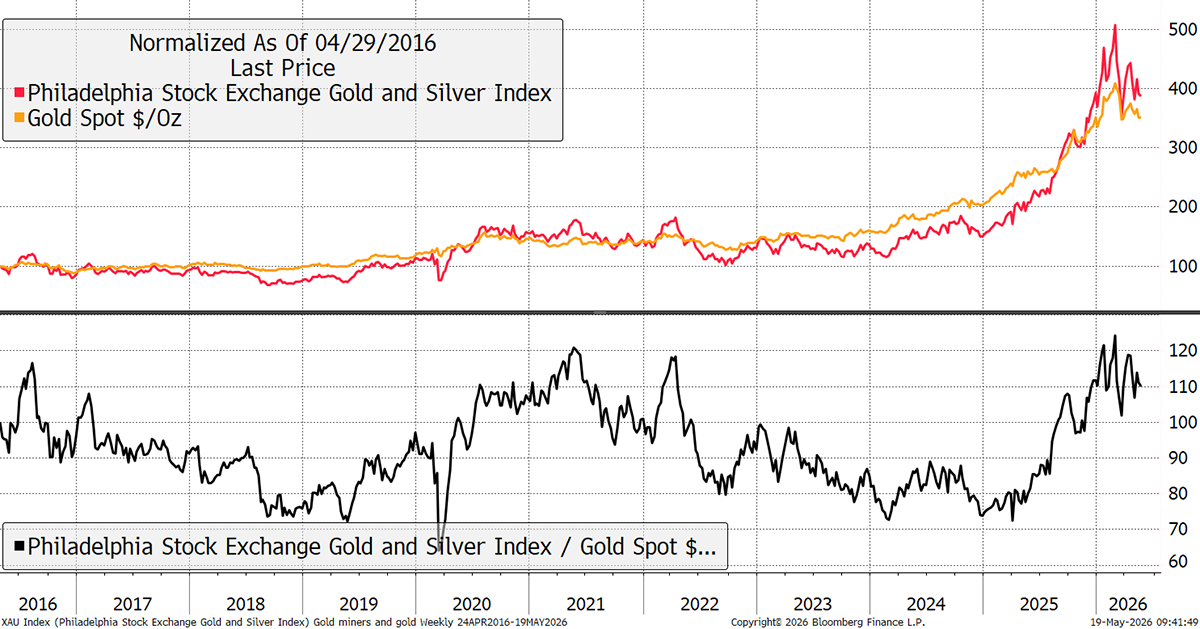

With gold and gold stocks, it is the exact opposite: the miners win the rallies and lag the falls. When gold was slack between 2020 and 2023, the stocks floundered. When the price took off in 2025, they surged. This couldn’t be more different from the relationship between oil and oil stocks. Gold stocks are for the gold bulls.

Gold vs the Gold Miners

I am still bullish on gold, but much more moderate. The world is printing money, but the price did so well last year that it needs a break. If we return to the 1970s scenario, oil and gold will take it in turns. That means gold’s next great run will kick off when oil finally peaks.

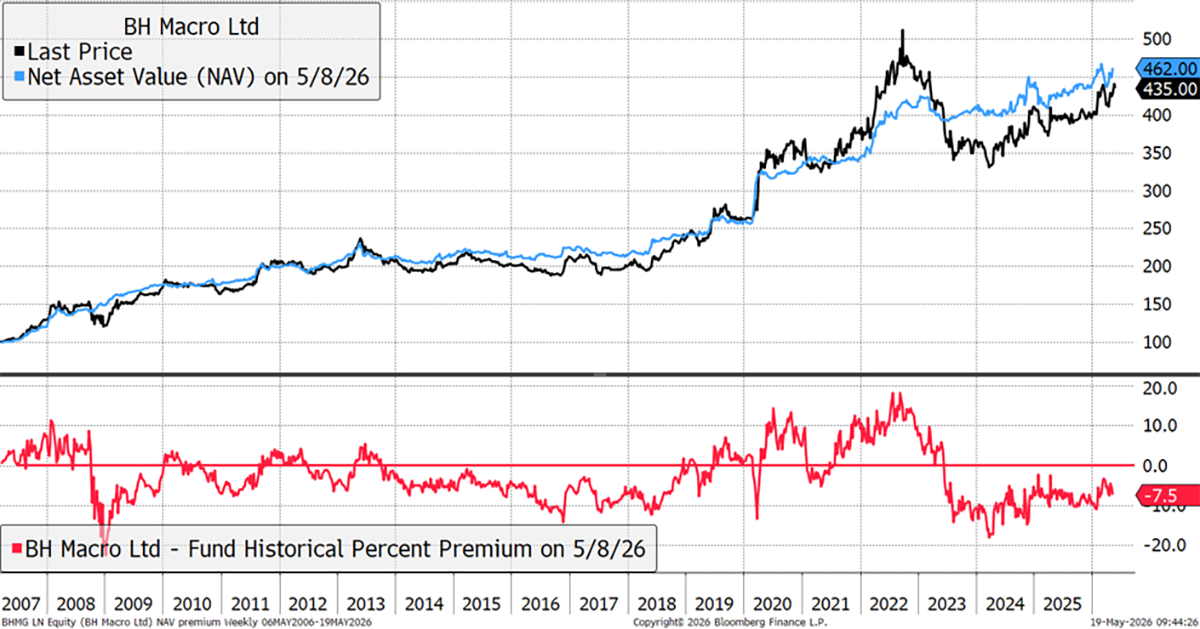

It is worth mentioning the BH Macro Trust (BHMG), which has been doing well. They are macro investors best known for their expertise in bonds and currencies. We bought it in June 2024, when the discount was wide. That has come in nicely, and better still, they are making money again as the NAV rises (blue). I mention BHMG because when they start doing well, they tend to go on a roll.

BH Macro Net Asset Value

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd