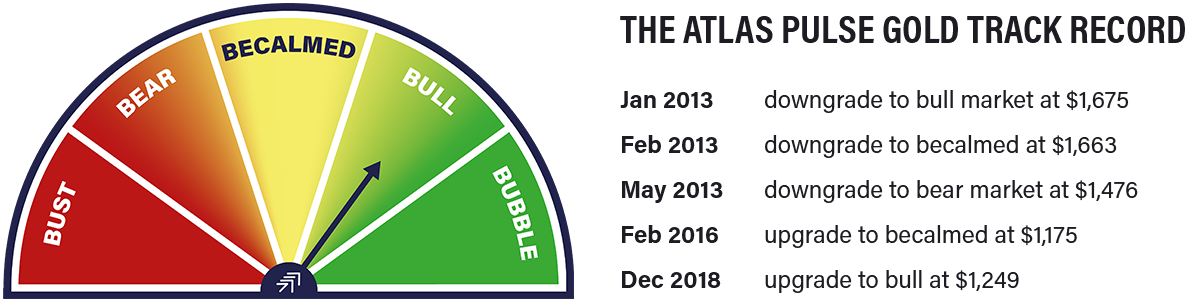

Gold Correction Still More Likely than a Bear

Atlas Pulse Gold Report Issue 115;

I do not think gold bull markets end in periods with high real rates. More likely, they begin from periods of high real rates. Moreover, the central banks are not stupid, and they are lapping up the opportunity to buy the dip.

Bear, or Correction?

For us gold bugs, life before 28th January was so much easier. In 2025, gold rose by 64.6%, the best year since the 126.5% surge in 1979. In 2026, gold is down by 5.8%, and 24.9% since the peak. Over five years, the gold price is up by 128% and over ten years, 203.3%.

The question remains whether this is a correction within an ongoing bull market, or a prolonged downturn, that we saw post 1980 and 2011. I remain in the correction camp. Several things have turned against gold, but we mustn’t underestimate the power of gravity. Gold has done well, too well perhaps, and all bull markets are periodically tested.

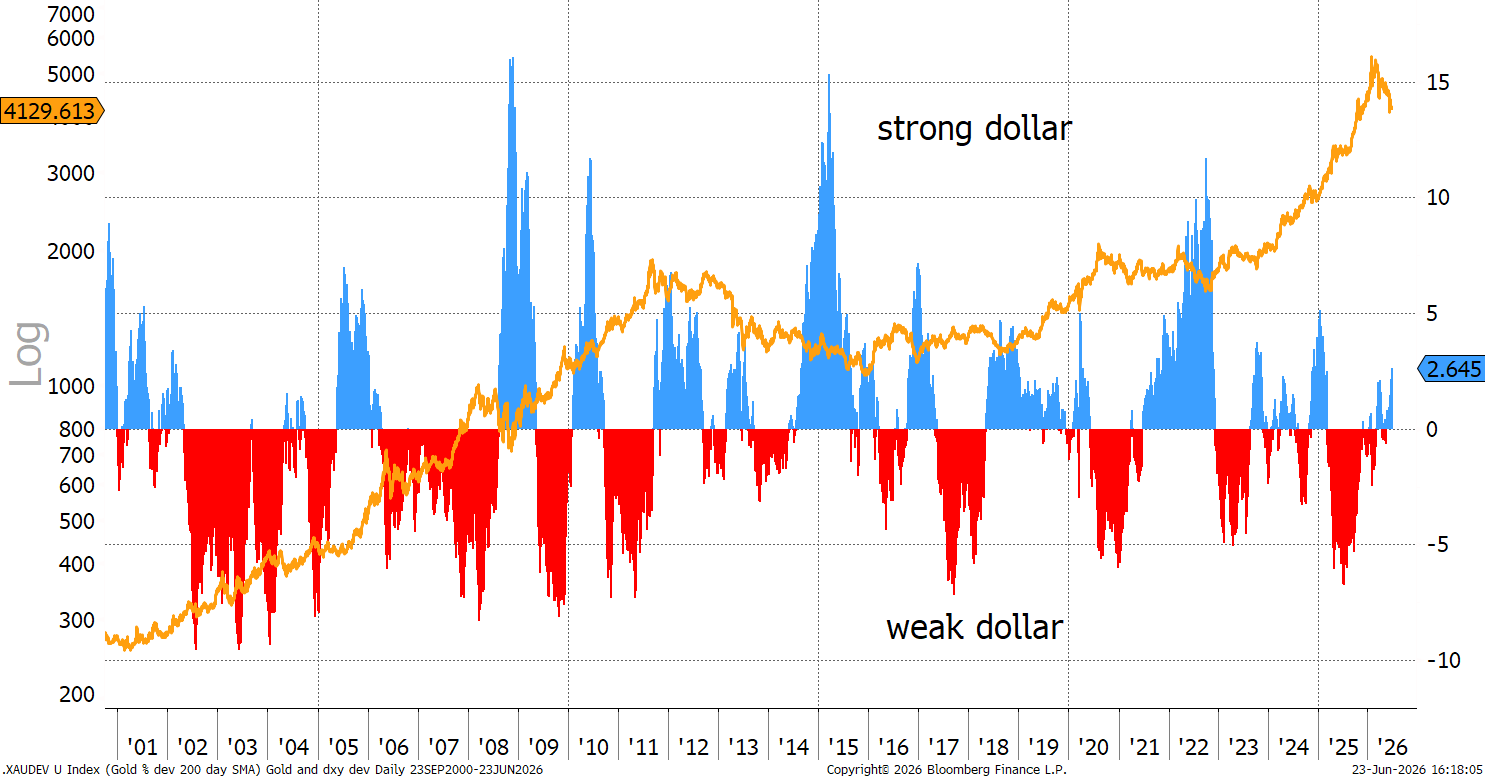

There are times when the dollar doesn’t matter that much for gold and times when it does. For example, in 2001, 2005, 2010, and 2019, the dollar rallied alongside gold, because the macro case at the time far exceeded the dollar headwind. At other times, when the macro case for gold has been lesser or exhausted, dollar rallies have been detrimental, such as in 2008, 2014, and 2022.

Gold and the US Dollar

This time, the fundamental case for gold remains strong, but the narrative is tired following the surge in price. Add to that a dollar rally, and a correction has ensued. The US dollar has been buoyed by a pickup in short-term real interest rates.

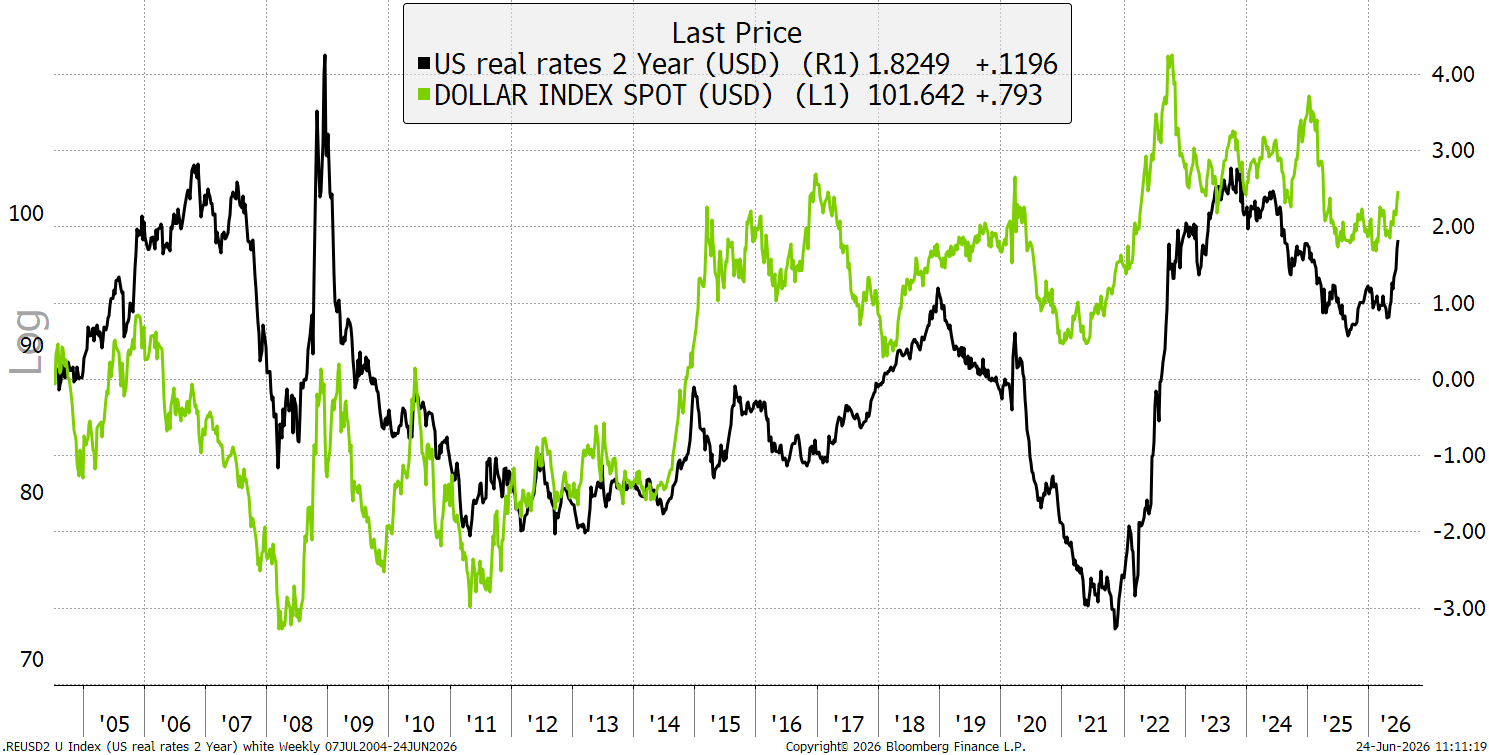

The Dollar and Short-term Real Rates

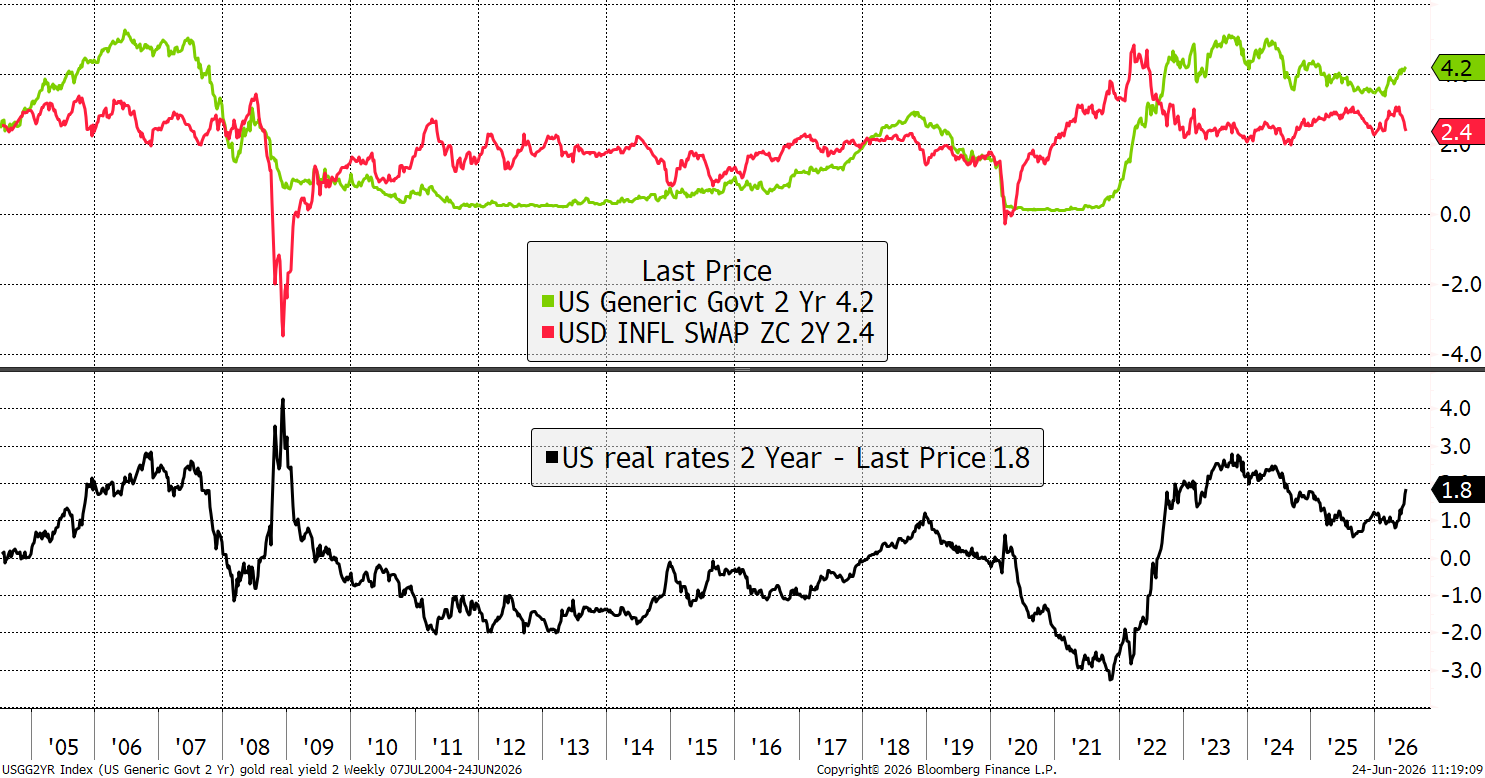

The 2-year real rate touched 1.8%, which is historically high. That comes as the 2-year treasury yield has risen to 4.2% (rate cuts less likely) and inflation expectations have plummeted to 2.4% (Warsh in the Fed Chair, and peace (?) in the Straits of Hormuz). The real rate is A-B, hence 1.8%. The previous high readings include 2007, 2008, 2018, and 2022. All these periods marked peaks in stockmarkets.

The Two-Year Real Yield

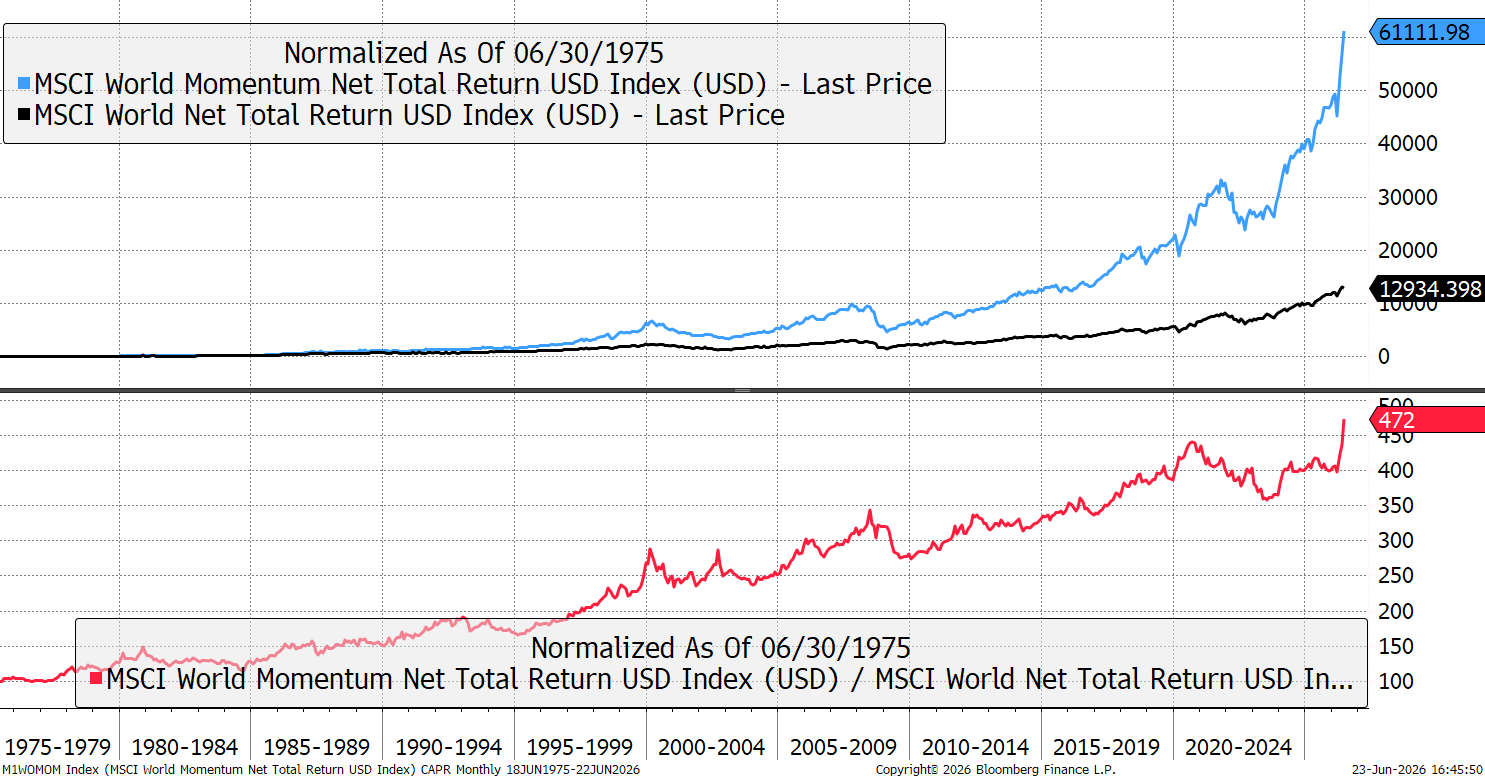

Real yields were also high in 2000 (not shown above), at the peak of the tech bubble. We have another major tech bubble, this time most prominent in AI. I show the world momentum index compared to the world index. The long-term outperformance has been excellent, but choppy. Recently there has been a huge move following a soft patch since 2020 (red).

Momentum Stocks Versus the World

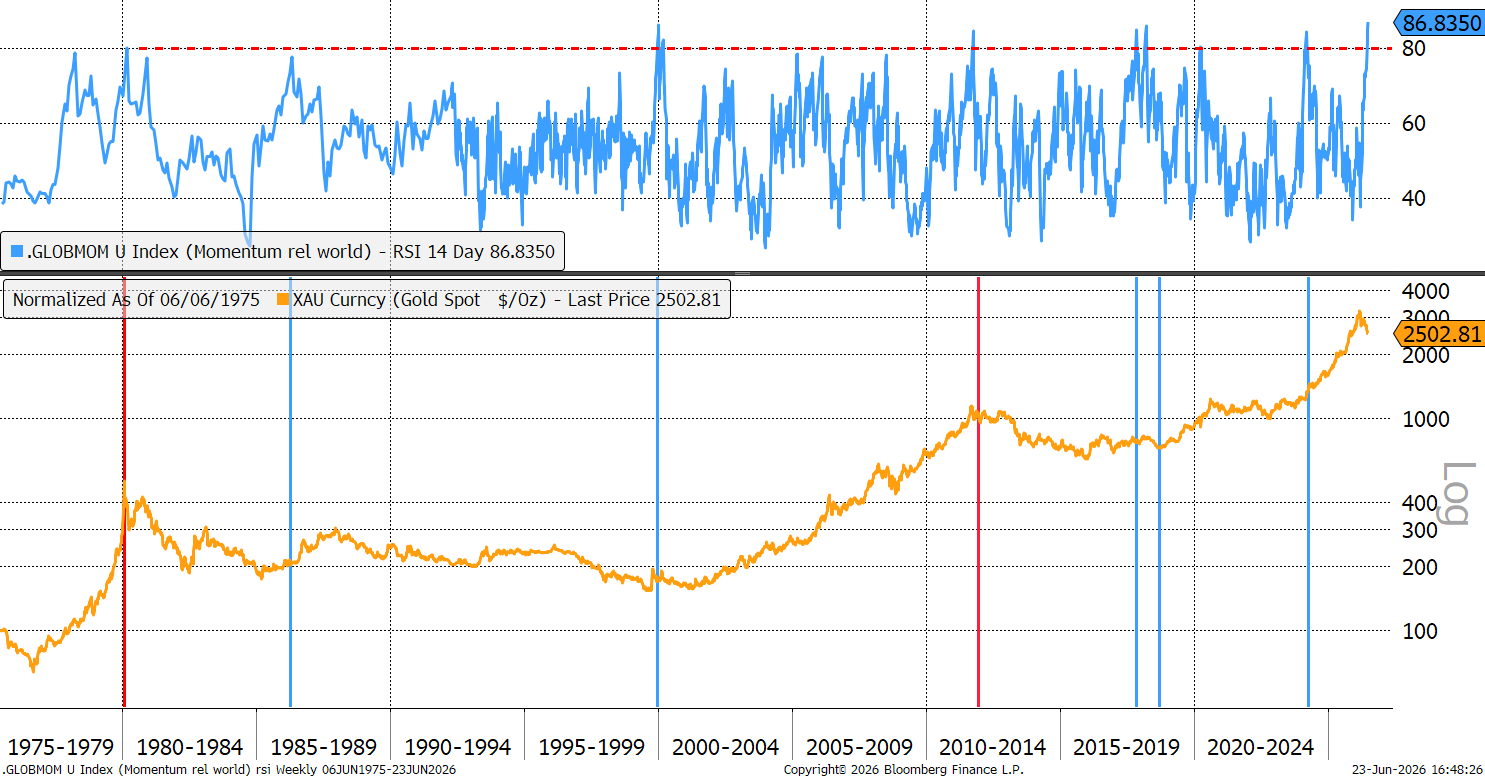

Momentum (momo) stocks are selected on the grounds that they have already been going up over the past year, hence they have captured the AI trade. When momo is doing well, it means the best-performing stocks are the ones that have already risen a great deal. I measure monthly RSI, an overbought/oversold indicator, on momo versus the world. High readings urge caution.

Momo RSI

Just as gold was heavily overbought in late January, just as momo is today. The lower chart overlays momo extremes (blue line) over the gold price since 1974. The blue horizontals show momo spikes which turned out to be good for gold, and the red ones bad. I would argue that the red ones coincided when gold was the momo trade, and the blue ones when it wasn’t.

In 1979, inflation was double digits and rising. The market leadership was dominated by gold stocks and commodities, meaning that gold was the bubble. In 2011, we had come out of a credit crisis, the economy was still in tatters, the European bond markets were fighting for survival, and even the tech sector was still in the doghouse. Real interest rates had collapsed, and for gold, that was as good as it got. The rise in real rates from 2013, killed the gold bull market.

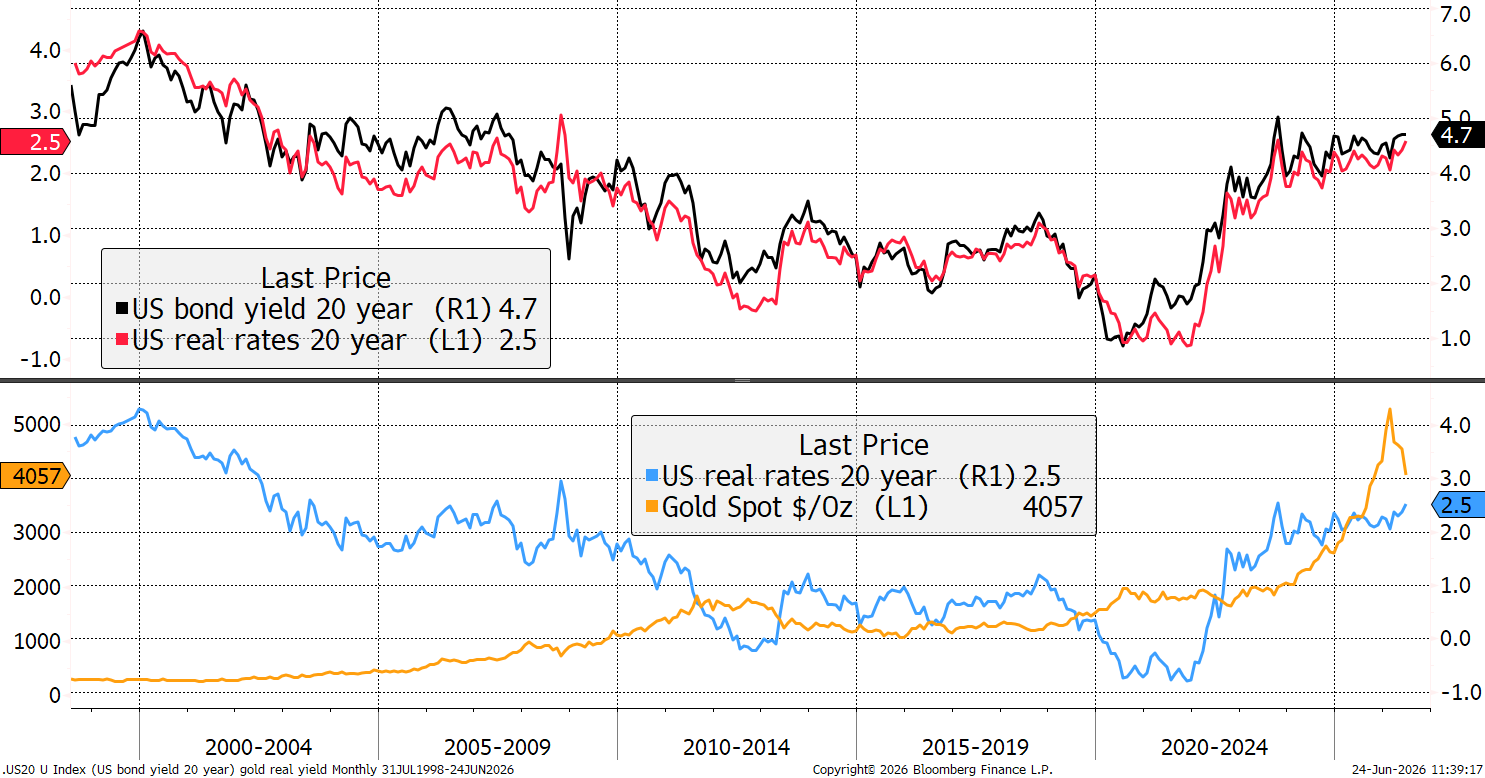

I have always believed that while the dollar is sensitive to short-term real yields, gold is most sensitive to 20-year real yields. In 2011, these were at a low (blue) and soon spiked.

Gold and 20-Year Real Rates

The great gold bull market that began in 1999 started from high real rates of 4%, which fell to 0% by 2011. The 2018 bull started from 1% falling to -1% by 2020. Remarkably, the demand for gold from the central banks since 2022 has been so high that the gold surge has shrugged off a period of high real rates. The gold bear of 2022 was short-lived, and once real rates stabilised, the price soared. But as I said, real rates are now rising again.

My question for the gold bears is, how can a gold bear market start from high real rates?

I agree that the gold price can slide while real rates are still rising, but they are already very high, and a material rise from here would require a new Paul Volcker at the Fed. Could that be Kevin Warsh, the new Fed Chair? Maybe, but Trump wouldn’t be very happy if he went on a market cleansing exercise. Also, these days, we couldn’t afford it. Debt to GDP is just too high.

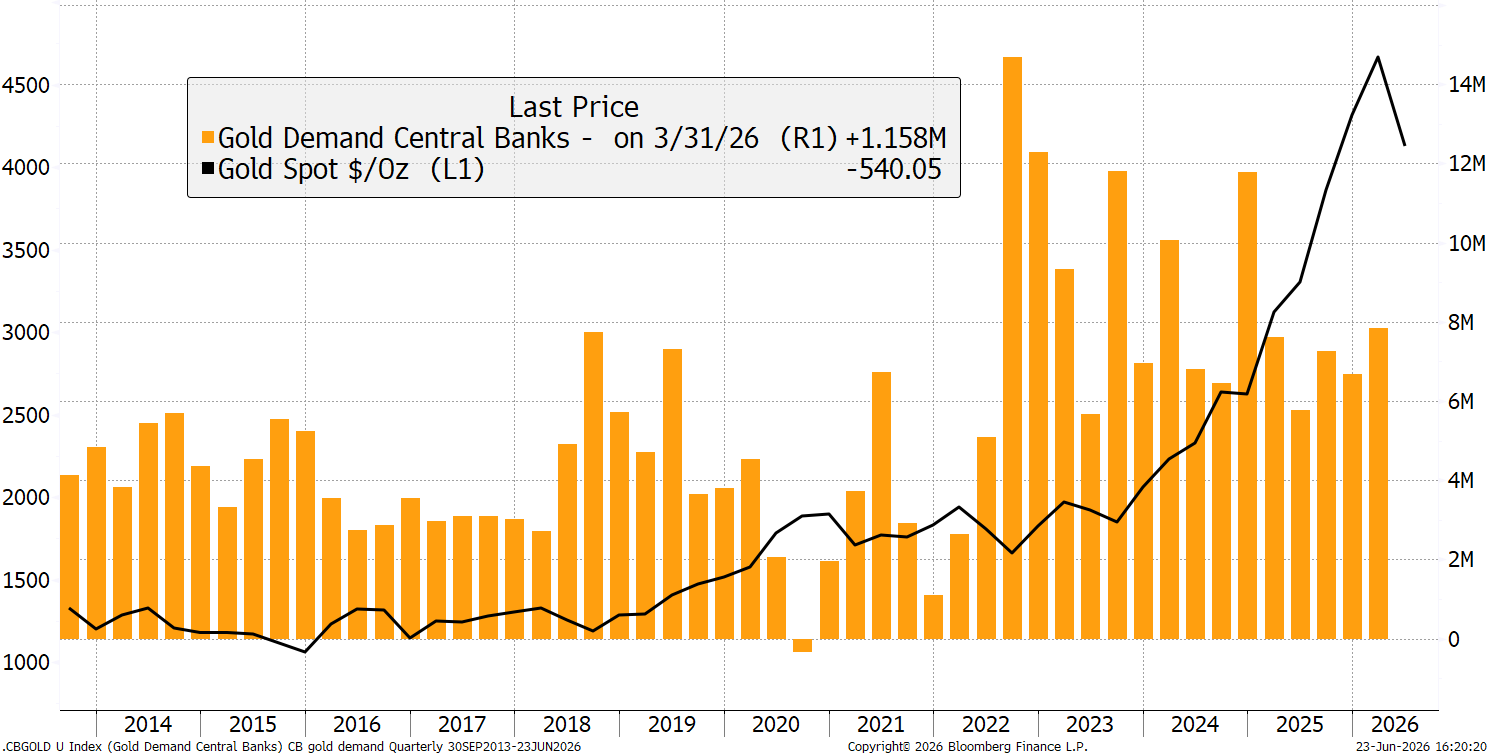

That is why the central banks have picked up their purchases because they see gold as an attractive way to hold reserves. Gold cannot be confiscated as easily as bonds, and unlike bonds, the supply is limited.

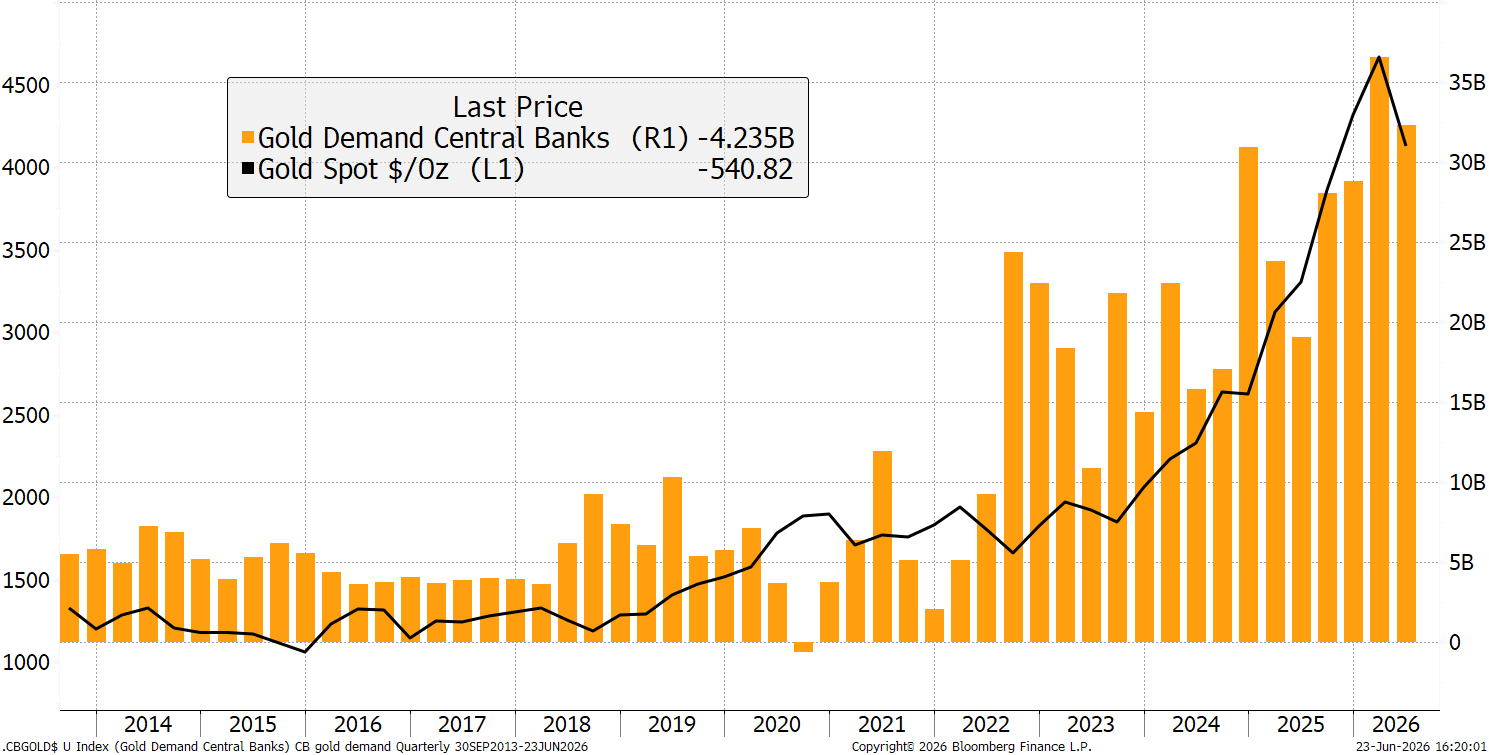

Central Bank Gold Purchases – million ounces

Before you say the central banks bought more gold in 2022, prices were sub $2,000 per ounce, when today they are double that. Looking at their dollar purchase amounts, the dollars invested have held at over $30 billion per quarter. This is real money.

Central Bank Gold Purchases – billion dollars

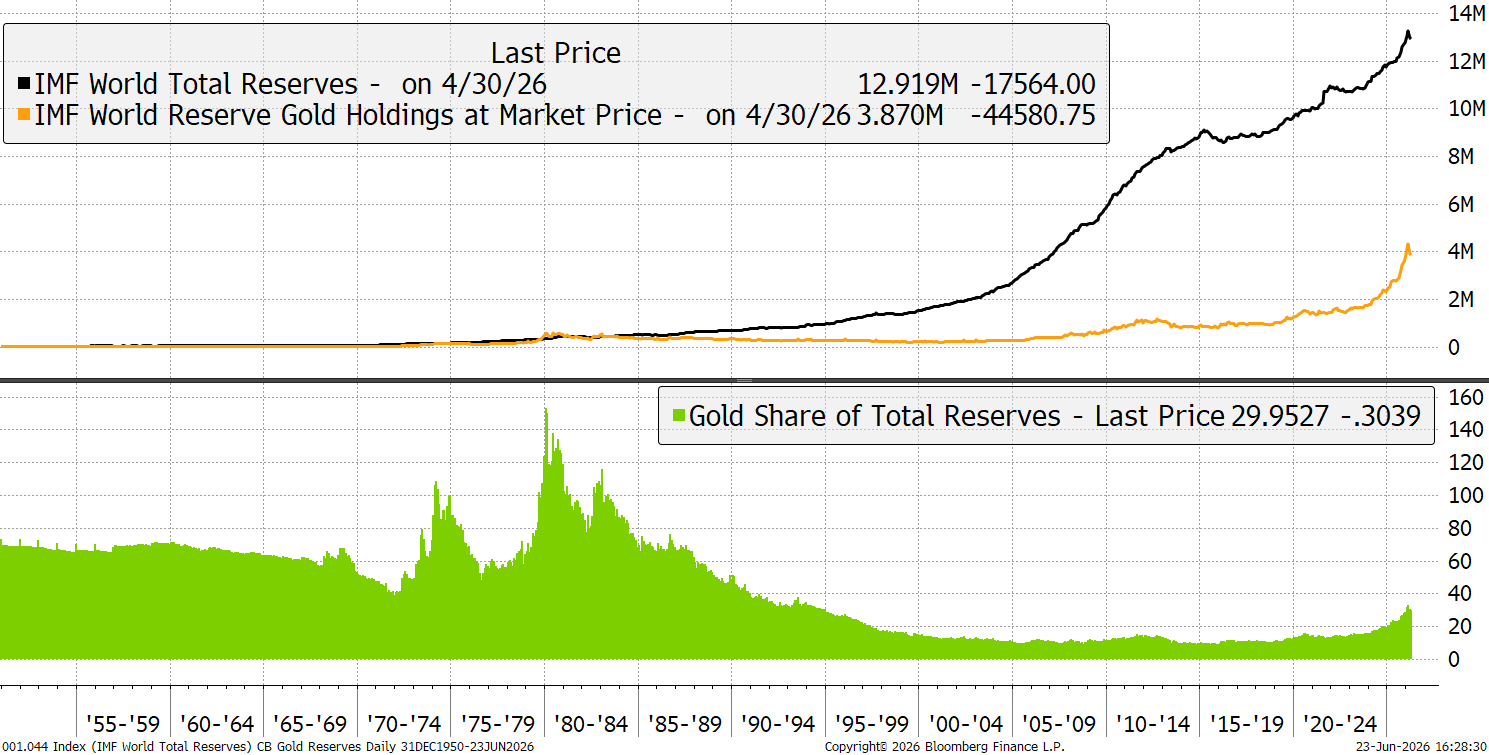

The central banks are on a mission. I show the world’s total reserves, and gold’s share of the total, which is just under 30%. May I remind you that in the good ol’ days, this was closer to 80%.

Central Bank Gold Share of Reserves

I do not think gold bull markets end in periods with high real rates. It is more likely they begin from periods of high real rates. Moreover, the central banks are not stupid, and they are lapping up the opportunity to buy the dip.

Bitcoin versus Gold

Gold has a friend in the liquid alternative asset space, which is complementary. I do not believe these assets are in competition as they have natural, and low correlation. That said, they can move together for brief periods, especially when the dollar is moving. A weak dollar boosts both, while a strong dollar causes pain.

You’d expect bitcoin to do better over the long term, as it is more mischievous and youthful, and it has.