The Gold to BOLD Switch

Atlas Pulse Gold Report - Issue 113;

Gold’s relationship with real yields is long established, but it has been less visible during the recent boom. Now, it is back with a vengeance, and the bulls need to respect the bond market.

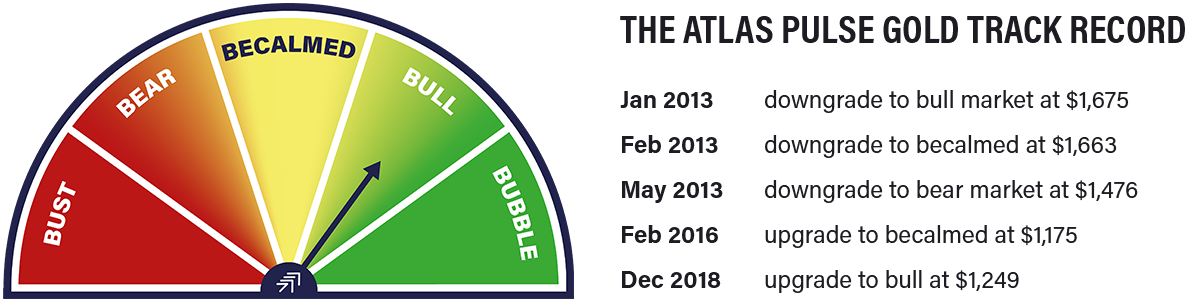

As the price of gold sits back in the market recovery, I felt it was a good time to check in on the Atlas Pulse gold dial, shown above. It is driven by three rules that determine the state of the market. I created the model nearly 20 years ago and haven’t changed it since. It reminds us that gold is still in a structural bull market, but that doesn’t mean the price of gold cannot stall over the medium term.

The three rules were based on three important things:

- Price strength

- Price relative strength

- Monetary conditions

Price Strength

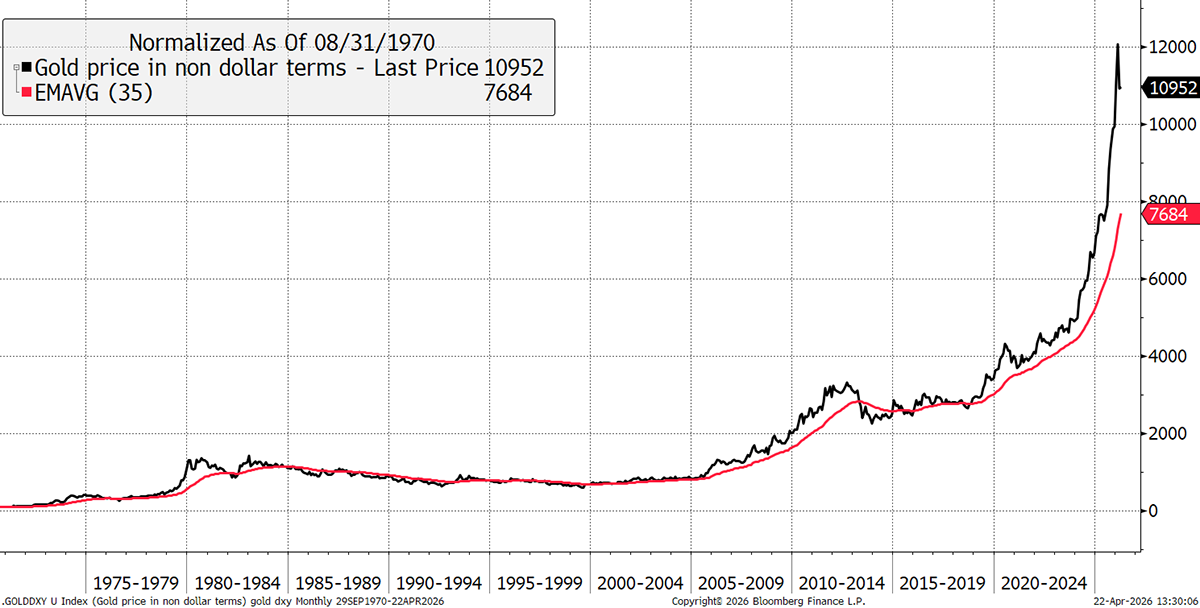

Even 20 years ago, I was suspicious of the gold bulls harping on about the end of the dollar. There have been times where gold price strength, measured in dollar terms, merely offset the falling dollar (e.g. between 2000 and 2008), and no more. For example, between 2000 and 2005, gold priced in euros was broadly flat while the dollar index fell by 30%, and gold in USD rallied by a similar amount.

To understand the true gold price trend, I use a medium to long-term horizon, with the dollar removed. That means the gold price is shown in a basket of currencies and can trend higher or lower regardless of dollar moves. It’s a cleaner measure. The moving average is a 35-month exponential, which is a medium to long-term horizon, and the exponential aspect is faster to respond to trend changes than a conventional moving average. The gradient of the 35-month exponential moving average gold price in global currency determines this first input; the trend (red) is strong.

Gold Price in a Global Currency Basket

Price Relative Strength

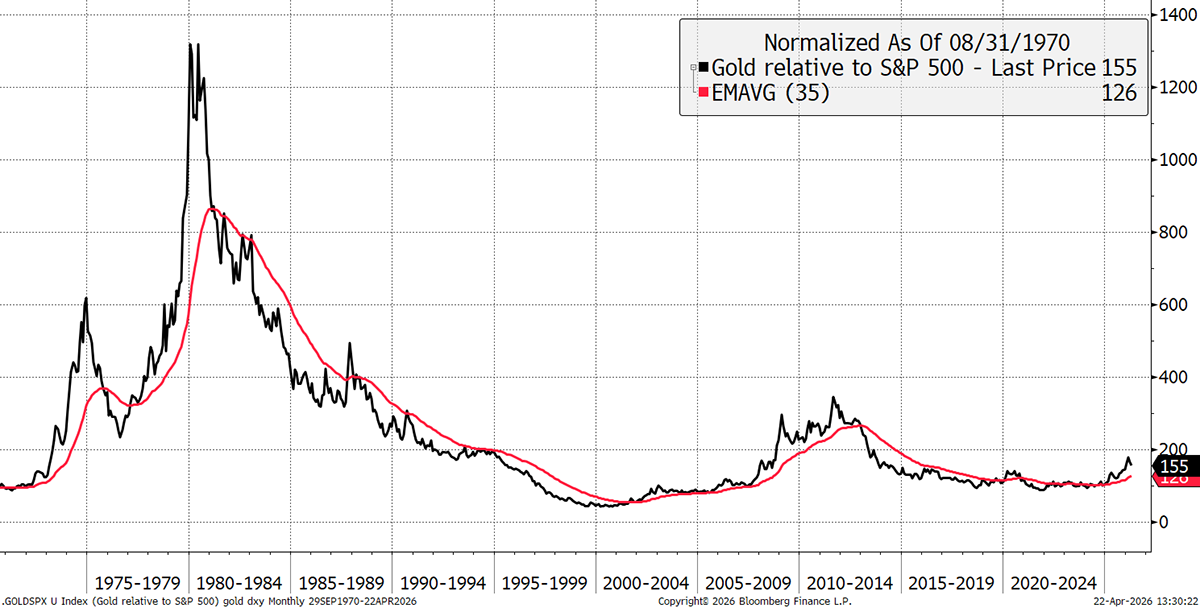

Using the same moving average as above, keeping things simple and not overly optimised, I measure the gold price relative to the S&P 500 Index. The key point here is that financial buyers will happily hold gold when they are confident that it will add to performance. If the gold price is failing to at least keep up with the stockmarket, then it detracts. Therefore, relative strength shows when an asset is “generating alpha”, in financial parlance, or, more simply, it is relevant. Even with a strong S&P, gold has been in an uptrend for the past 18 months.

Gold Price in a Global Currency Basket

Monetary Conditions

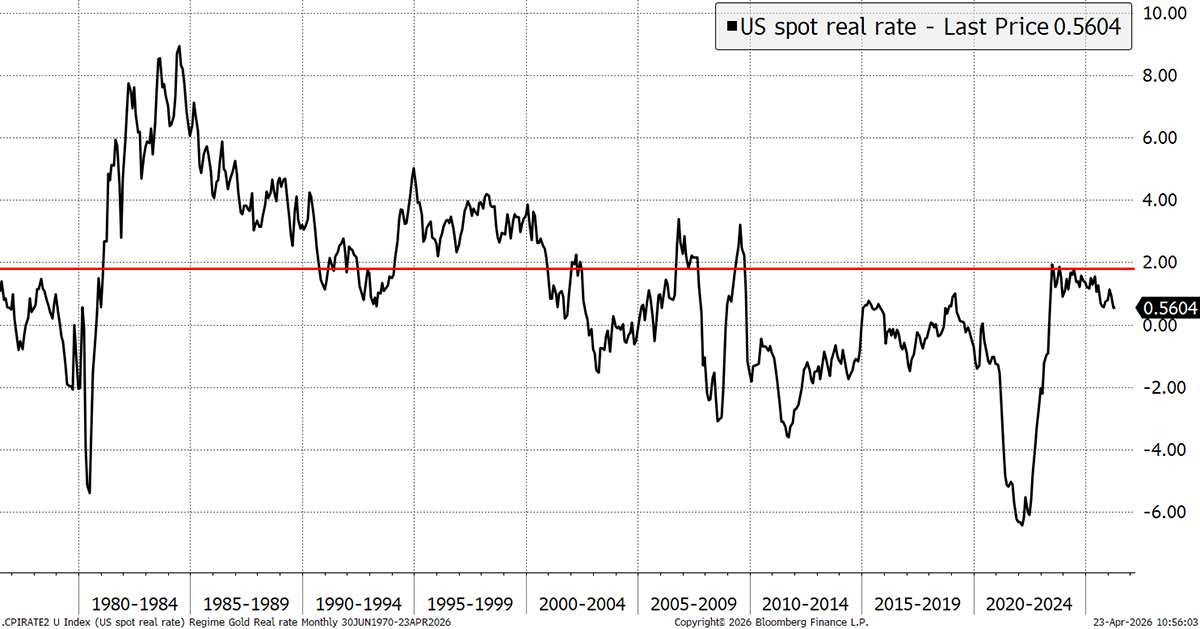

The final model was based on gold’s holding costs. I use the US 2-year bond yield less the 12-month change in CPI to determine the short-term real interest rates. I determined that a reading below 1.8% was generally supportive for the gold price, while a reading above was detrimental.

The idea is that 1.8% is the real return investors can get from a low-risk investment in short-dated treasuries. Anything below 1.8% is an acceptable carry cost, and when real rates are negative, gold becomes particularly attractive, as the alternative is paltry. When real rates move above 1.8%, the pain threshold kicks in, as investors can generate a real return with minimal risk.

US Real Interest Rates

Real rates are 0.56% on this measure. CPI is currently 3.3% and rising, while 2-year rates are 3.8% and are probably following the oil price. Higher inflation, with lower rates, is the best monetary backdrop for a rising gold price.

Gold Dial: Combining the Scores

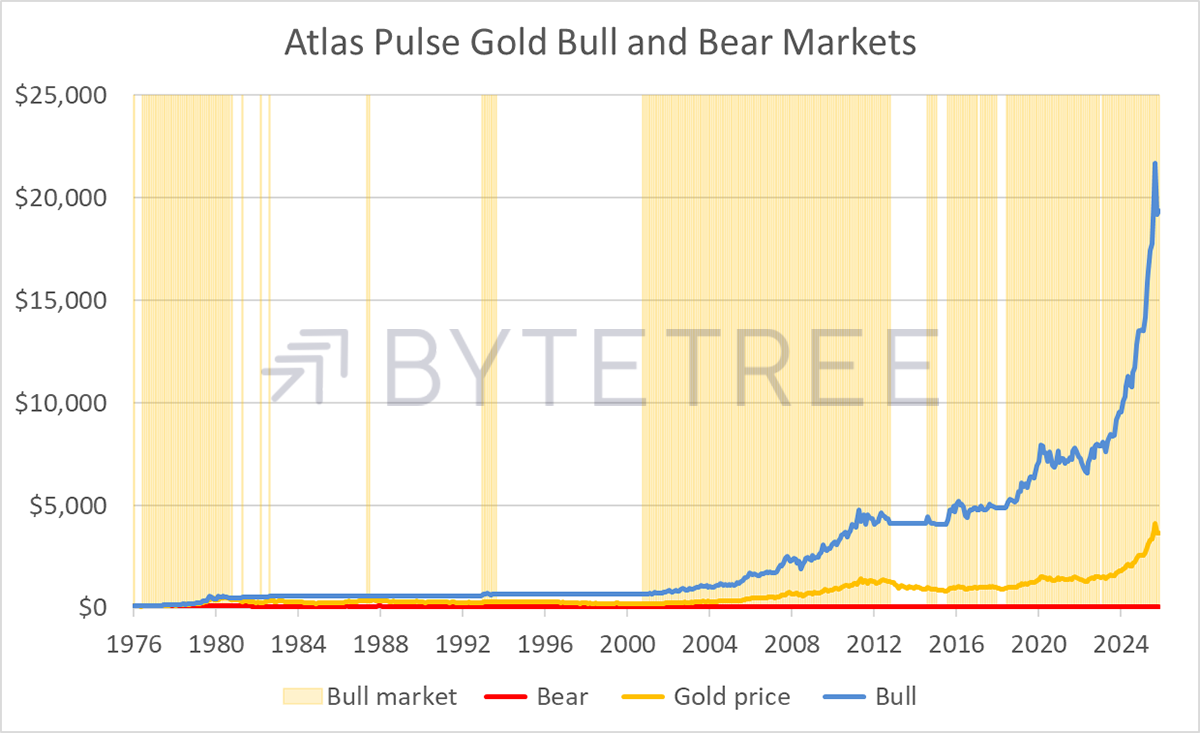

The next part combines the scores. With all three models currently positive, the total score is 3 out of 3, which is a confirmed bull market. In fact, the model is generous and considers a score of 2 or 3 a bull market. A score of 1 is neutral, and 0 is a bear. If you invested $100 in gold since 1976, it is now worth $3,667. However, if you had only been long during the shaded bull periods, that becomes $19,357. The bear scenario? That $100 is now worth $46.

Gold: Bull and Bear Markets

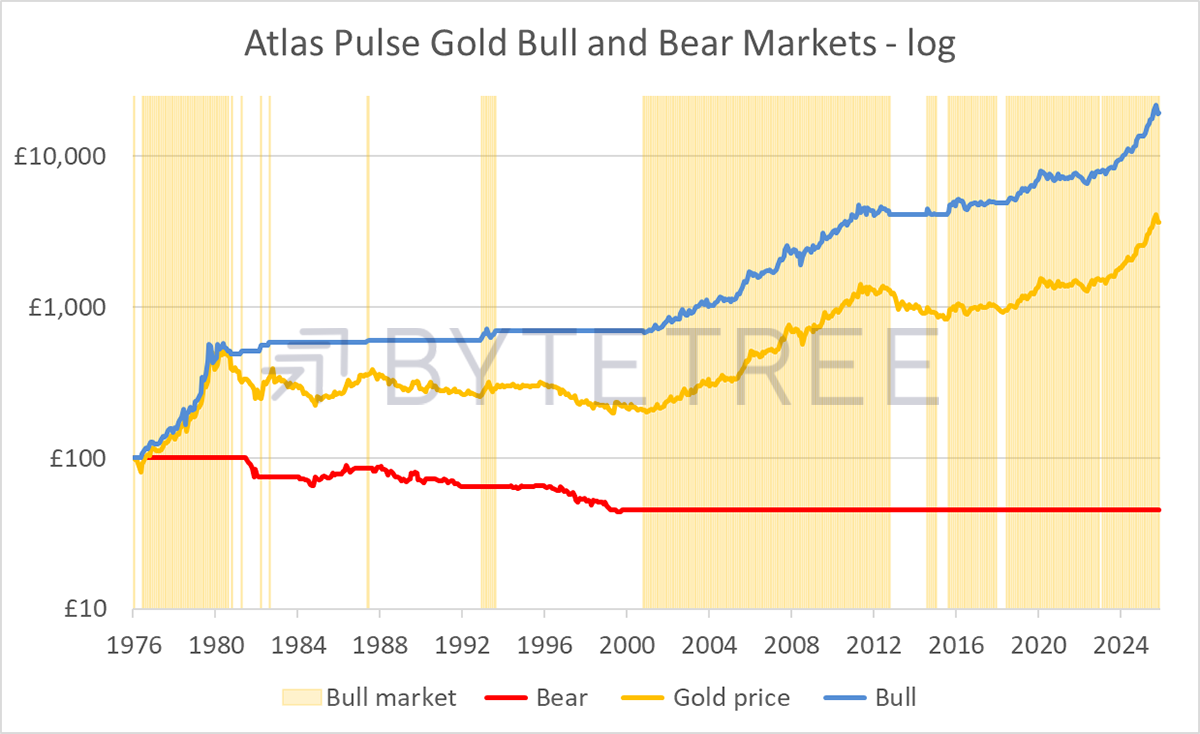

Using a log scale, it becomes clearer. Note that I haven’t shown neutral (score of 1), which has similar results to bear. The bottom line is that this simple idea highlights times when it is best not to own gold. Miss them, and the differences are startling.

Gold: Bull and Bear Markets – Log Scale

Gold Dial: Historical Forecasts

Since the model was created, it forecast the demise of gold in late 2012, and only became interested again in 2015, and much more so in late 2018. I was never tempted to downgrade the dial in the 2021 gold lull, because the underlying case remained positive, with the only negative being that gold was failing to keep up with the stockmarket. On other measures, it was still bullish, and a score of 2 is enough to keep us interested.

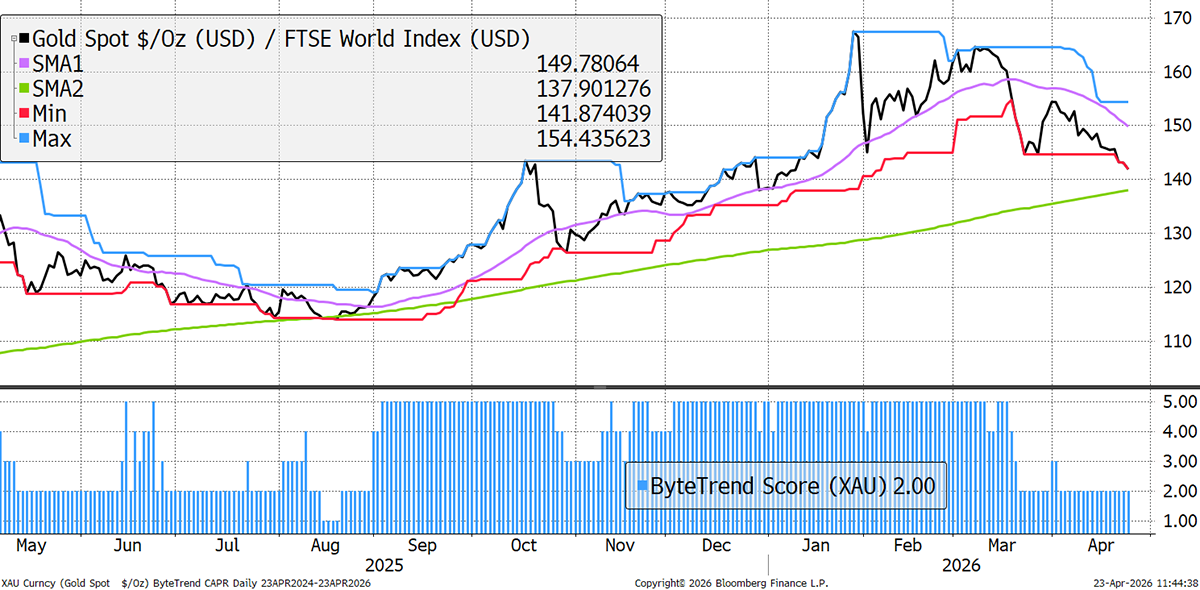

Yet gold had a major price peak on 28 January 2026, touching $5,595 intraday, and now just $4,692, having touched $4,009 on 23 March. That was the most overbought (extended from trend) reading since 1979, and the price is sliding against the stockmarket. I show the gold price relative to global equities. The persistent ByteTrend daily score of 5 has now dropped to a 2, meaning that the price is sliding, with only the 200-day moving average demonstrating a strong medium-term trend.

Gold ByteTrend Score Relative to the World

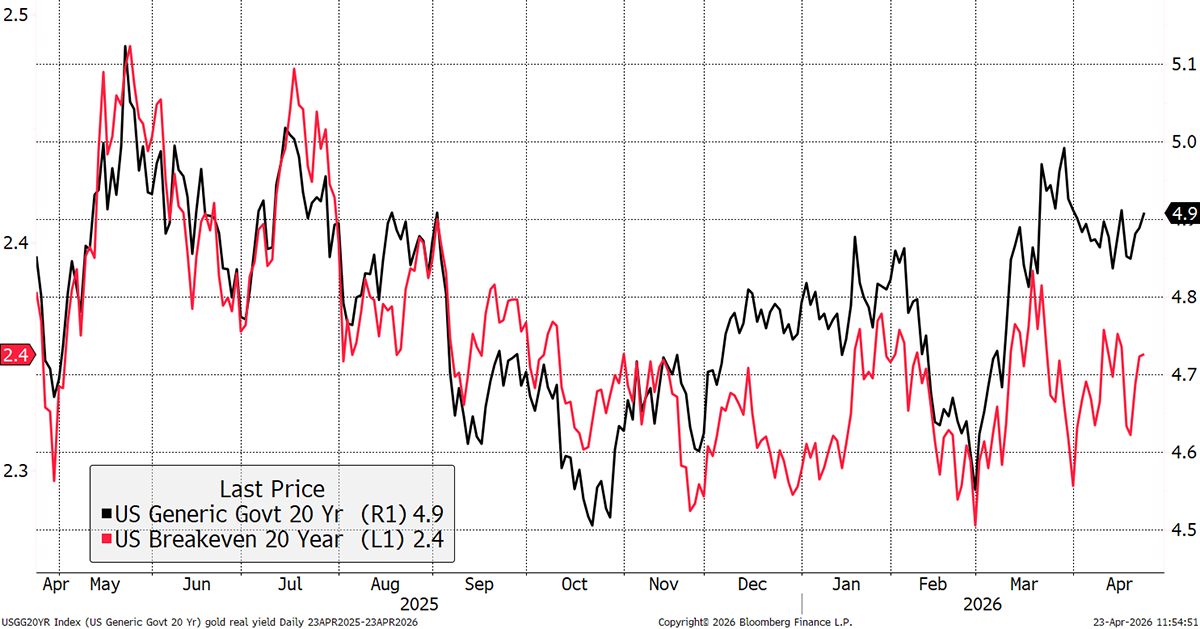

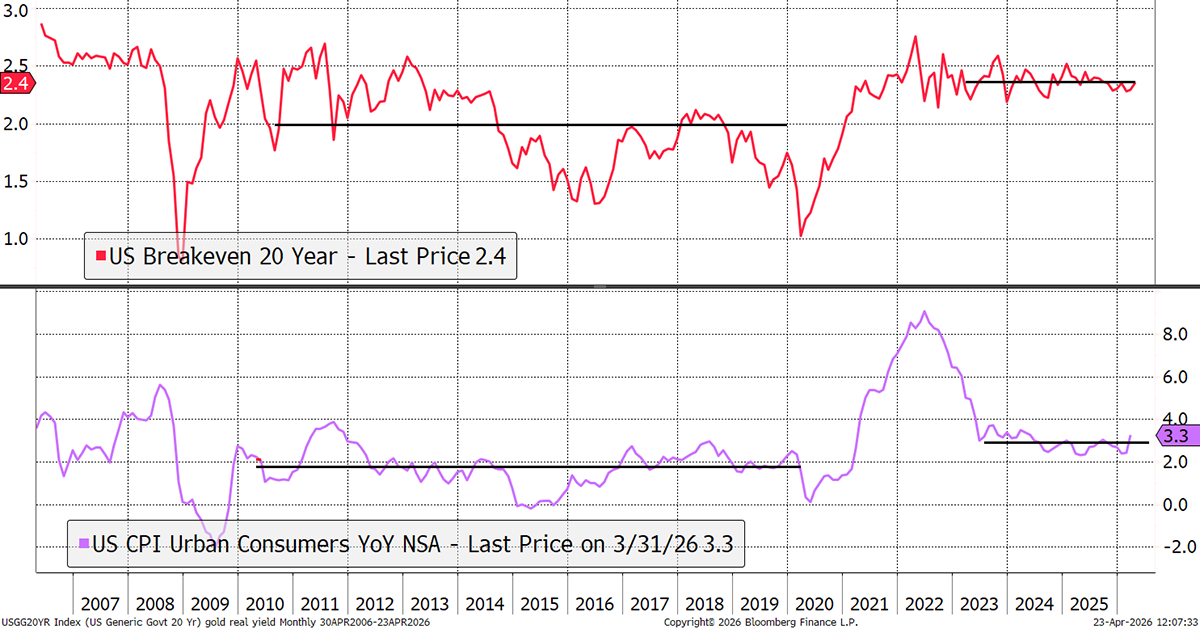

It means that gold has once again lost its relevance in the new market environment. This may be temporary and hopefully is. While the real yield measured above is positive, the more immediate longer-term measures are proving to be a headwind. The war in Iran has led to 20-year bond yields rising, while 20-year inflation expectations remain muted.

20-Year Bond Yields and Inflation Expectations

Deduct inflation (red) from the yield (black), and we have the 20-year real yield (blue below), which historically is most closely linked to the gold price. They are moving inversely, which is a good thing when real yields are falling, but not so when they are rising. What’s happening in the bond market is driving the gold price.

Gold and 20-Year Real Yields

Gold’s relationship with real yields is long established but has been less visible during the recent boom. It is back with vengeance, and the bulls need to respect the bond market. For some reason or another, the US bond market does not think long-term inflation is a cause for concern. The 20-year inflation averaged 2% when CPI averaged 2% between the financial crisis in 2008 and the pandemic. Since 2023, in the aftermath of the Ukraine/money printing shock, CPI has averaged 2.9%, while the 20-year inflation has been a lower 2.4%. The bond market does not think the huge debt burden, oil shortages, renewed money printing, and so on, are inflationary. I have little doubt that when they do, gold will surge.

CPI versus 20-Year Inflation Expectations

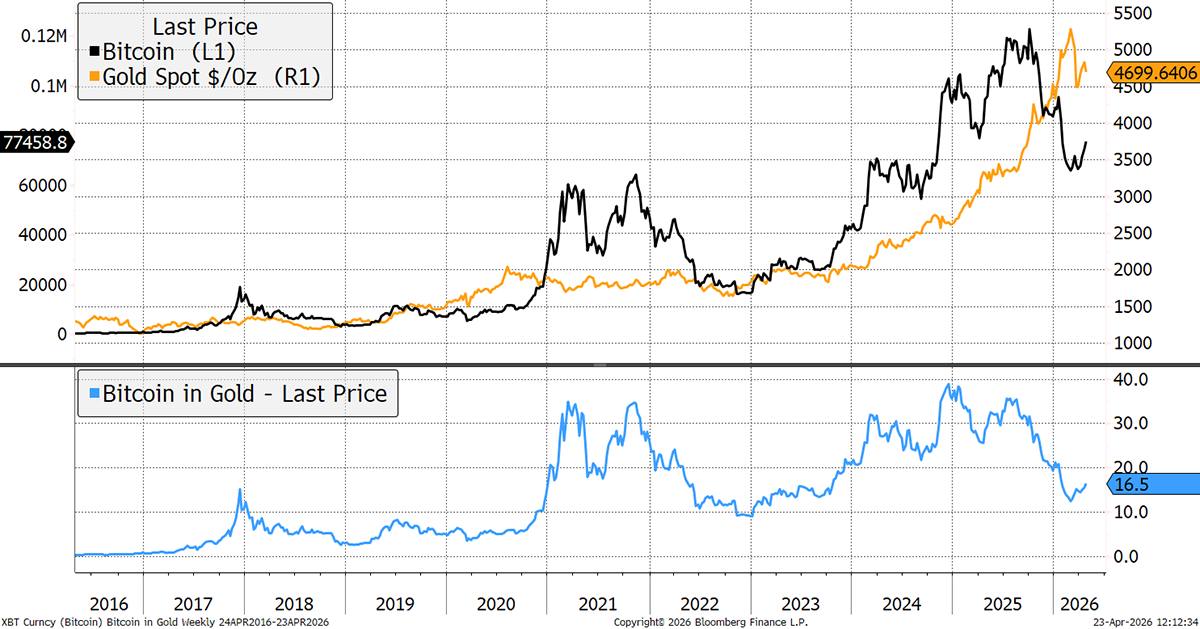

Just as gold has made a short-term peak, Bitcoin has made a trough. Once again, these complementary assets are working together, taking turns to carry the baton. The price of Bitcoin measured in gold (blue) was 15 ounces last month, and today, it is 16.5 ounces. Whereas gold needs real rates to be falling, Bitcoin is quite happy for rates and inflation to be rising, alongside commodities, financials and heavy industry.

Bitcoin and Gold

I believe Bitcoin is at the trough of the cycle and starting to recover. It crashed late last year alongside software stocks and is now seeing renewed signs of strength. Morgan Stanley launched a Bitcoin ETF two weeks ago, and Goldman Sachs stated their intent to follow suit. Just last week, Charles Schwab, the largest independent broker in the US, announced they are launching a crypto spot trading service. The good times lie ahead.

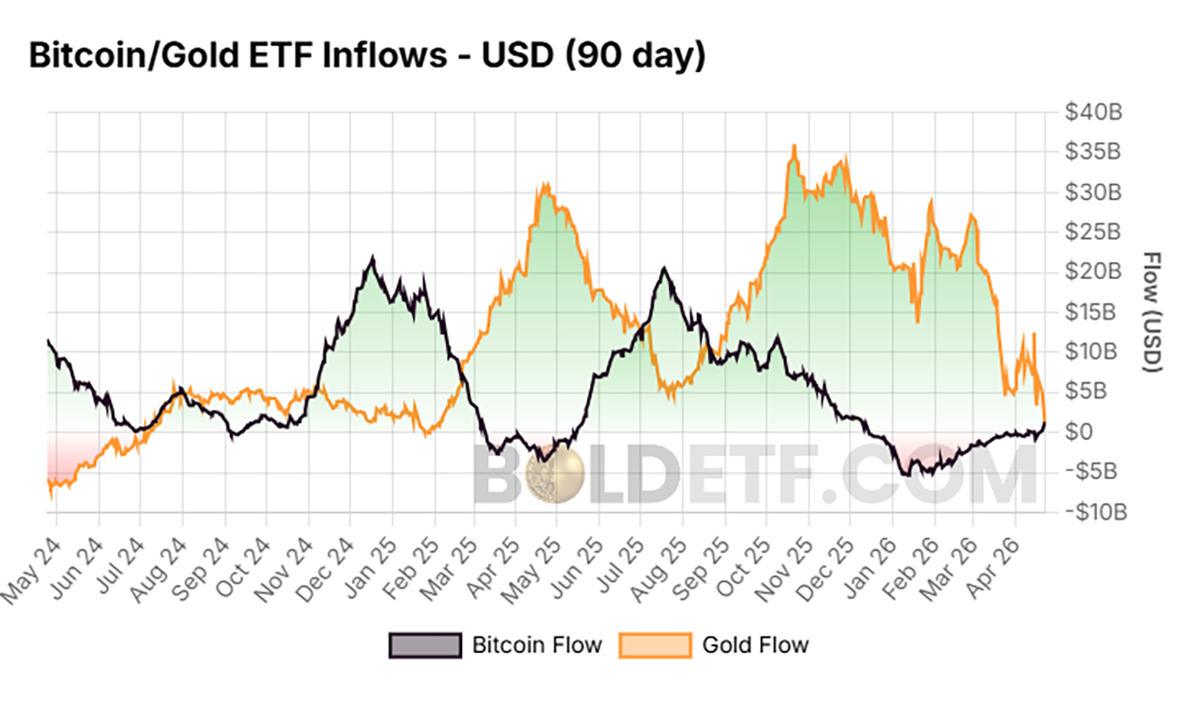

Our flow data on BOLDETF.com shows that over the past 90 days, the gold flows have shrunk from a record $35 billion to $0, while Bitcoin outflows have stabilised and moved into positive territory. Imagine what the price will do when the inflows resume.

Bitcoin and Gold ETF Flows

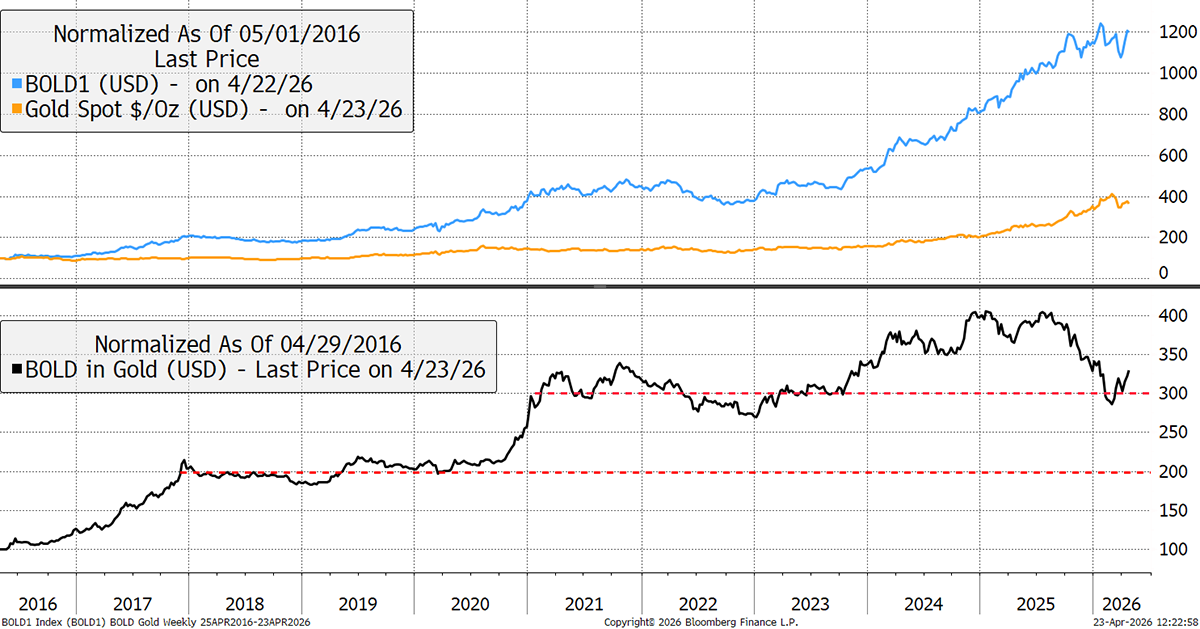

BOLD turns four on Monday, 27 April, and there’ll be a celebratory note this weekend. I created BOLD for two main reasons. Firstly, it was a simple way for investors to own Bitcoin in a much calmer manner. Secondly, and most importantly, it recognised that these were complementary assets and are better together than apart. The risk management through asset allocation and monthly rebalancing adds too much value to ignore.

Over the past four years, gold investors would have been only slightly better off in BOLD than gold, but I sense that is about to change. Bitcoin rallies can be powerful and typically happen when gold has been soft, as they best perform in different macroeconomic conditions. They are printing money again, and this time it will go to Bitcoin more so than gold.

Gold vs BOLD

So long as Bitcoin remains relevant, which I think it will be for decades, BOLD will beat gold over the long term. That point is obvious, but there are good times and bad times to make the switch. With gold stretched and Bitcoin just getting started, this is a very good time to make the gold to BOLD switch.

I have never said that before.

If you object or are unable to invest in BOLD, you can follow the Bitcoin and Gold weights for free on our website. For BOLD product details on the 21Shares Bitcoin Gold ETP, and for strategy information from ByteTree, please visit BOLDETF.com.

Summary

Gold has had one hell of a run since Atlas Pulse last upgraded gold to a bull market at $1,249 in December 2018. The long-term case is intact, but the short-term pressures from the bond market are clear. Time to consider diversifying into Bitcoin.

Thank you for reading Atlas Pulse. The Gold Dial remains on Bull Market.

Charlie Morris is the Founder and Editor of the Atlas Pulse Gold Report, established in 2012. His pioneering gold valuation model, developed in 2012, was published by the London Bullion Market Association (LBMA) and the World Gold Council (WGC). It is widely regarded as a major contribution to understanding the behaviour of the gold price.

Please email charlie.morris@bytetree.com with your thoughts.