Could Inflation Exceed Napier’s 4%?

Trade in Soda;

Tomorrow sees the US inflation report. The scare in 2021 turned out to be transitory after all, but it took longer to cool than the authorities would have liked. More to the point, it never fell below the 2% target, though it came close.

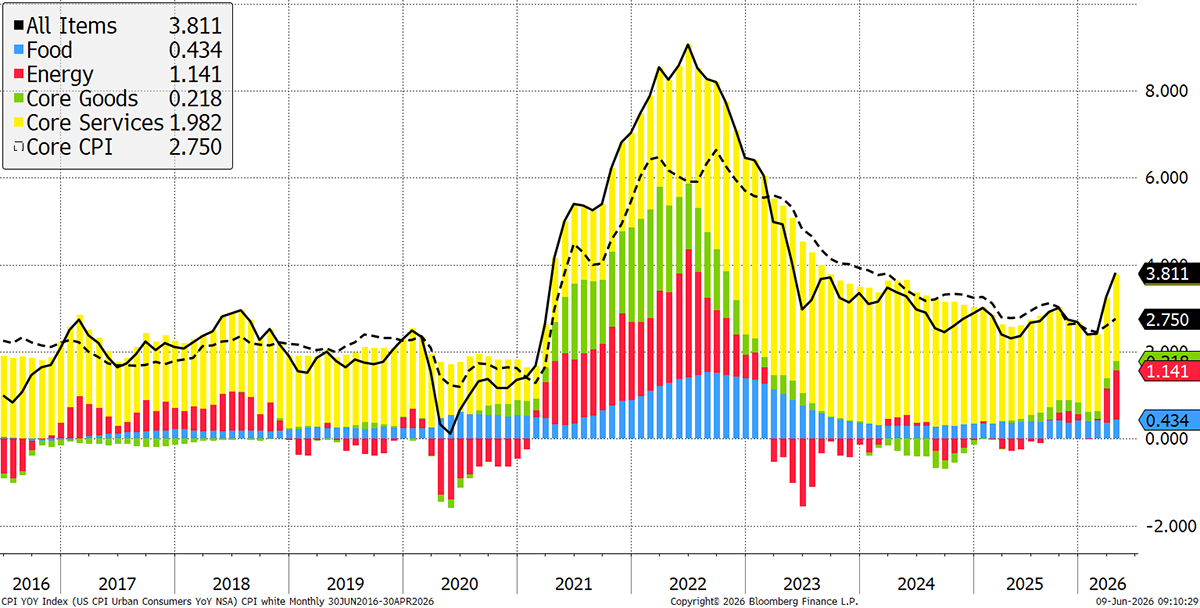

US Consumer Price Inflation

The market forecast is for 4.2% CPI tomorrow, but back down to 3% in a year’s time. This is important because higher inflation means higher rates, but the consensus forecast is still for no change in rates. Once again, the current inflation wave is deemed to be transitory. The primary culprit is the oil price due to the blockade in the Strait of Hormuz, where oil and oil products (red bar above) have been confined for over three months.

Still, the core inflation (black dash), which excludes energy, is also rising due to goods and services. While our masters can be sure that energy prices will fall when the Strait reopens, that hasn’t happened yet and may not for some time.

Will the Fed Hike Rates?

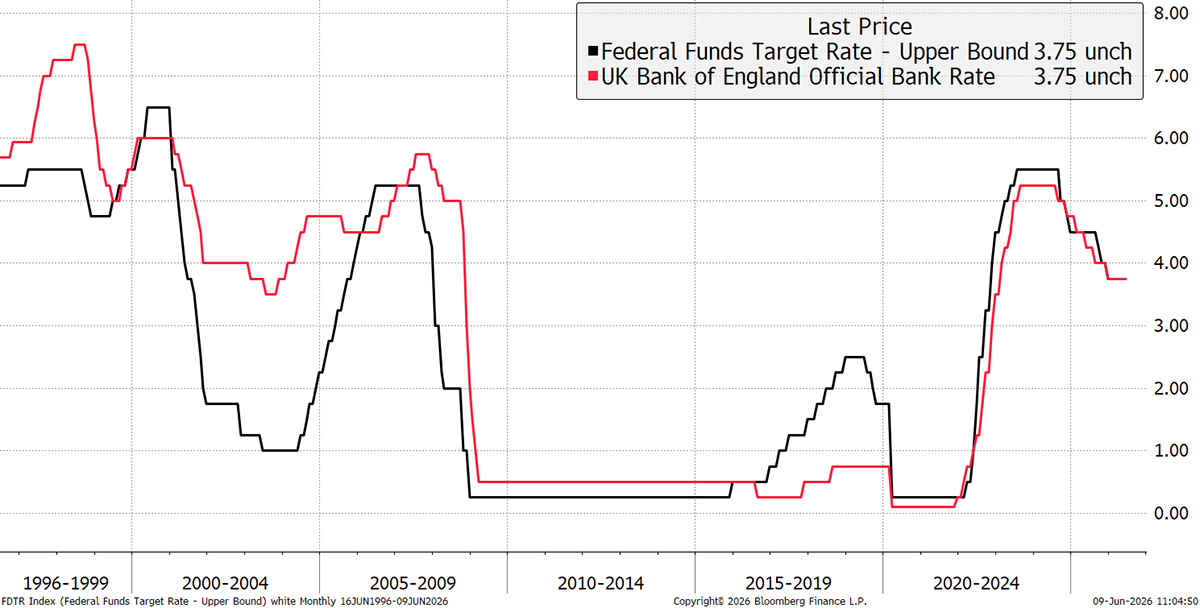

The following Wednesday, 17 June, sees the next meeting of the Federal Reserve. Interest rates are 3.75%, and once again, no change is expected. That said, there was disquiet last Friday when the market had its worst day in a while, with semiconductor stocks falling 10.4% on the day. Two things held up, the US dollar and quality stocks, with most other prices down, including gold.

UK rates have mimicked US rates, so it is important for us as well. There is some growing disquiet that inflation may be an understated risk, and that rates should rise sooner rather than later.

US and UK Base Rates

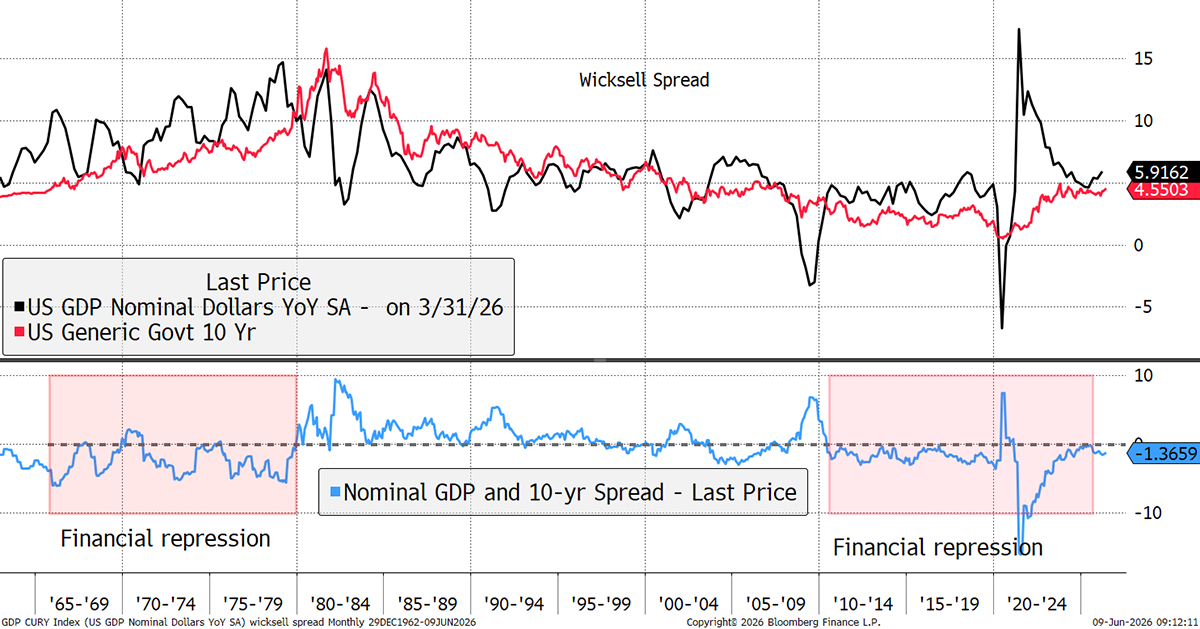

At the heart of it was a strong jobs report, which shifted interest rate expectations higher towards the end of this year. Essentially, the capex boom in the USA, driven almost entirely by the costly rollout of artificial intelligence, is boosting the economy. US nominal GDP growth is 5.9% (growth plus inflation), which, according to the late economist Knut Wicksell, should lead to higher bond yields.

The US Wicksell Spread

The Wicksell spread (blue) is the gap between nominal growth (black) and the 10-year bond yield (red). This is once again negative and probably too low. At -1.3%, it is priced for a slack economy, rather than a boom. This is deemed inflationary because borrowing is cheaper than it should be.

Beware of 4% Inflation

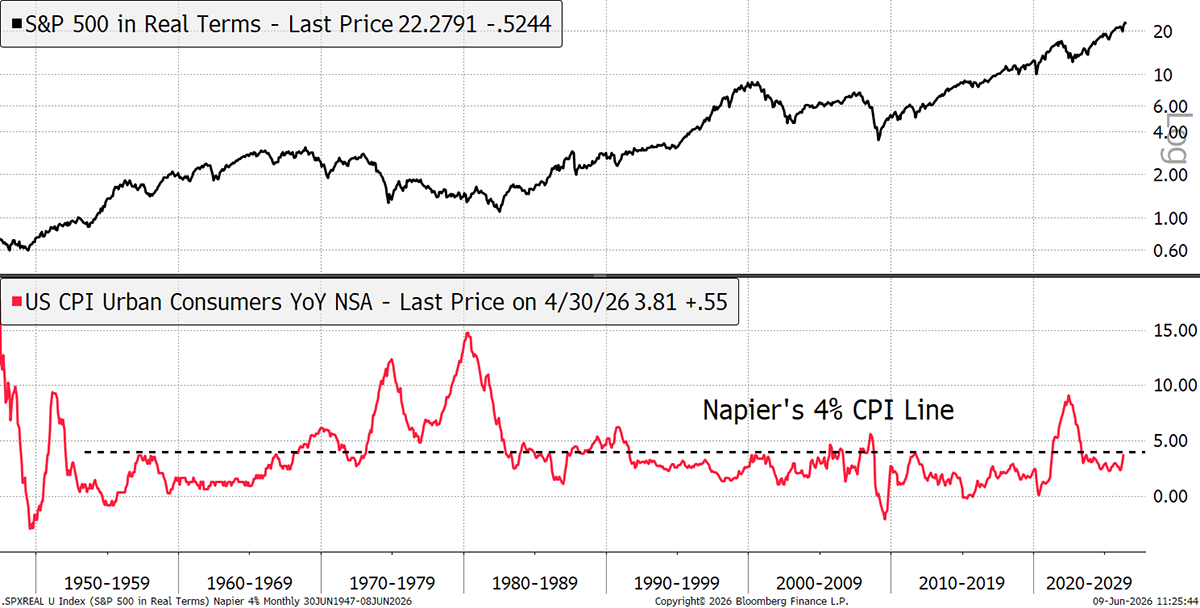

The accomplished market strategist, Russell Napier, wrote an excellent book, The Anatomy of a Bear Market, where he looked at the history and causes of past bear markets. One of his key findings was that when inflation exceeded 4%, the stockmarket started to wobble.

I show the S&P 500 in real terms (after inflation) against the US CPI. CPI rose above that 4% level in the late 1960s, much of the 1970s, just before the 1987 crash, in 2000 (3.6%), in 2008, and in 2021. It is a good track record.

Equities and Napier’s 4% CPI

The thesis is that high inflation robs investors of returns. Put simply, inflation is devalued money, so if companies are trying to make money, their output is also devalued. There are other impacts, such as cost pressures, which dent margins, and an increase in the cost of borrowing. The market history shows us that inflation is not well-received by the stockmarket.

The Oil Risk

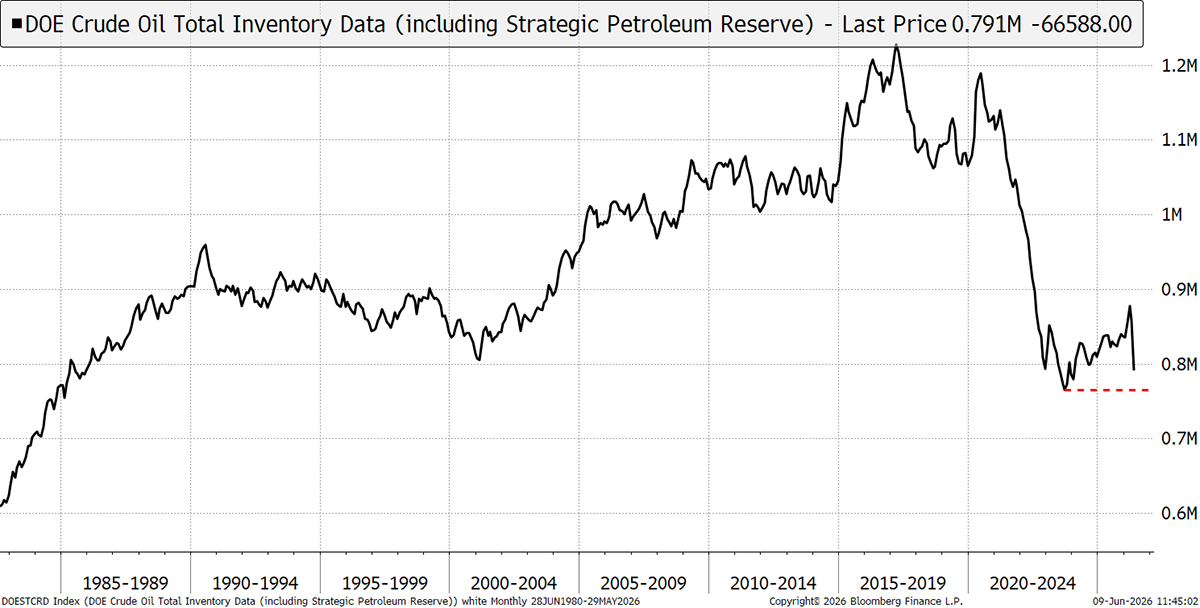

Oil remains the key risk, and the market is complacent. It is remarkable that the Middle East has been removed from the oil supply, and the impact has been so slight. The two main reasons are falling US inventories, including the strategic reserve, and falling Chinese imports. The latter is somewhat mysterious, but the assumption is that they are also drawing down their reserves.

In just two weeks, US inventories will have fallen to a new low, at levels last seen in the 1980s. Perhaps the system is so agile that it can cope for a while, but the debate rages on. The commodity experts highlight that a dwindling oil supply is a huge risk and will lead to a price spike, while the financiers and politicians believe there is nothing to see here and that this will soon pass.

US Total Oil Inventories since 1982

I agree with the view that when the Strait reopens and the market has had time to rebalance, we will return to a low oil price. That might possibly be lower than before the crisis, given the marginal efficiencies learned during the disruption. But the risk during the interim is high. Not only would an oil spike cause an inflation surge, but shortages would be hugely damaging for the economy.

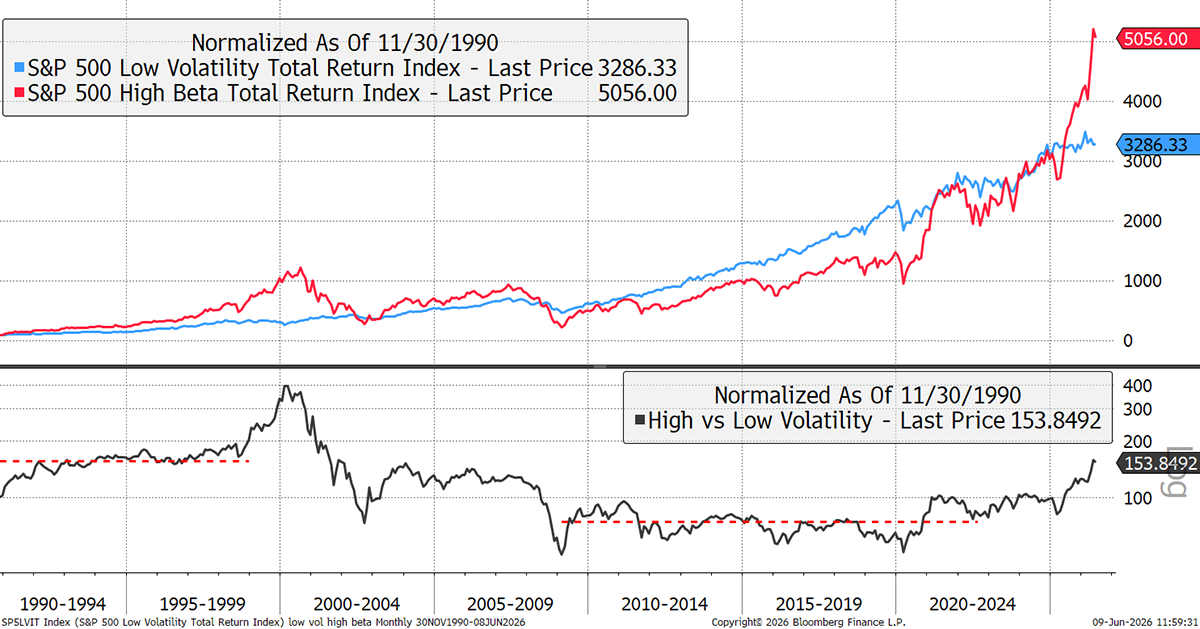

The Church and the Casino

In last week’s market selloff, one of the few things to appreciate on the day was the dollar, the other being quality stocks. I have shown this chart several times in the past to highlight Buffett’s point that the stockmarket is a church (blue) with a casino (red) attached. Investors can choose whichever they prefer. Recently, the casino has been much more generous than usual.

Low Volatility vs High Beta Stocks

Low volatility is a good proxy for quality, and I started to embrace these safer stocks last autumn with the launch of ByteTree Quality, as the market became more elevated. I have also included some of the quality stocks in the Whisky Portfolio for balance, and have added suitable quality funds to the Soda Portfolio. Quite simply, it is where you want to be when things go wrong, as last Friday proved.

The black line (above) shows the spread between low-volatility stocks and high-beta stocks, i.e. stocks that tend to rise faster than the market when the going is good. The horizontal lines show the pre-boom averages in the 1990s and the post-2008 environment. In 2000, high beta managed to rise 2.5x, and this time, 2.1x. However you measure it, this market is red hot.

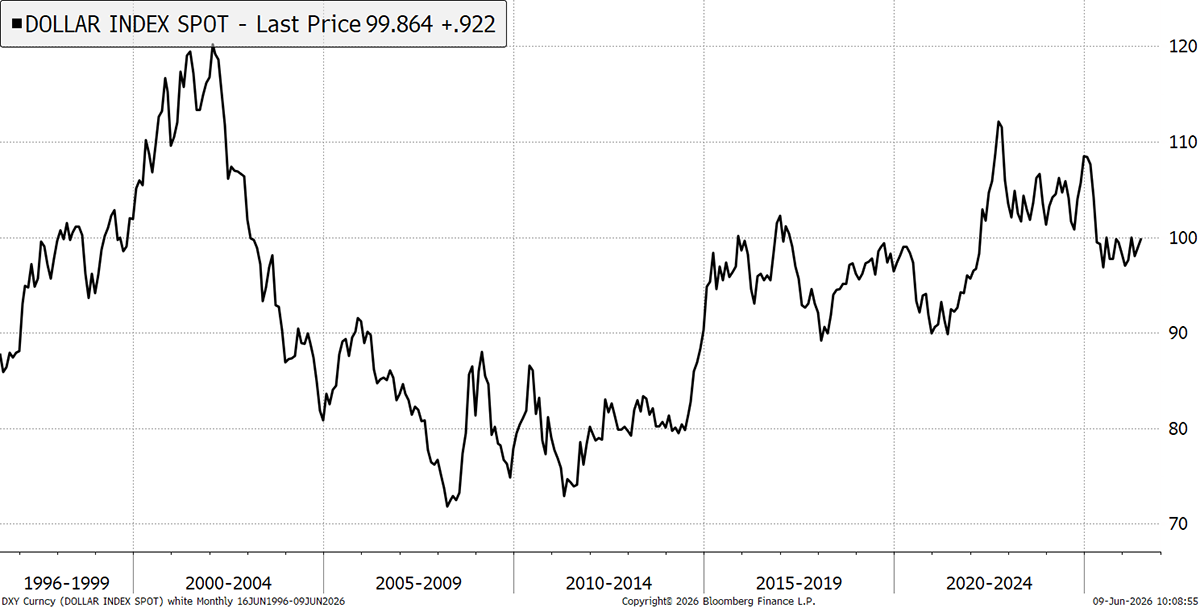

The Dollar Bounce

Many of the good times in recent years have coincided with a falling dollar. For example, the 2022 bear market low coincided with a dollar peak. The bull that followed coincided with a weaker dollar. It might not look like much, but last Friday’s market shake-up followed a 1.1% rise in the dollar. It is early days, but it is starting to look like an uptrend, which would be boosted by a rate hike, or even sooner, on the anticipation of a rate hike.

US Dollar Index

These small clues are important because I believe it is essential to own assets that are resilient when the market turns down. The Multi-Asset Investor portfolios are light on dollars, and I want to boost exposure.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd