AI Drives Genomics

Trade in Whisky;

This week I’ll be revisiting biotech and genomics, but before we get there, I will address a few other things happening in the markets.

Commodity prices have fallen back, which has crushed inflation expectations and saved the bond markets. Those thinking the new UK prime minister-in-waiting, Andy Burnham, has been given the green light by the bond market should think again. As I highlighted last week, and rightly or wrongly, the collapse in the oil price has cooled inflation fears, thus reducing bond yields. Burnham may turn out to be a lucky PM.

UK Growth Surge?

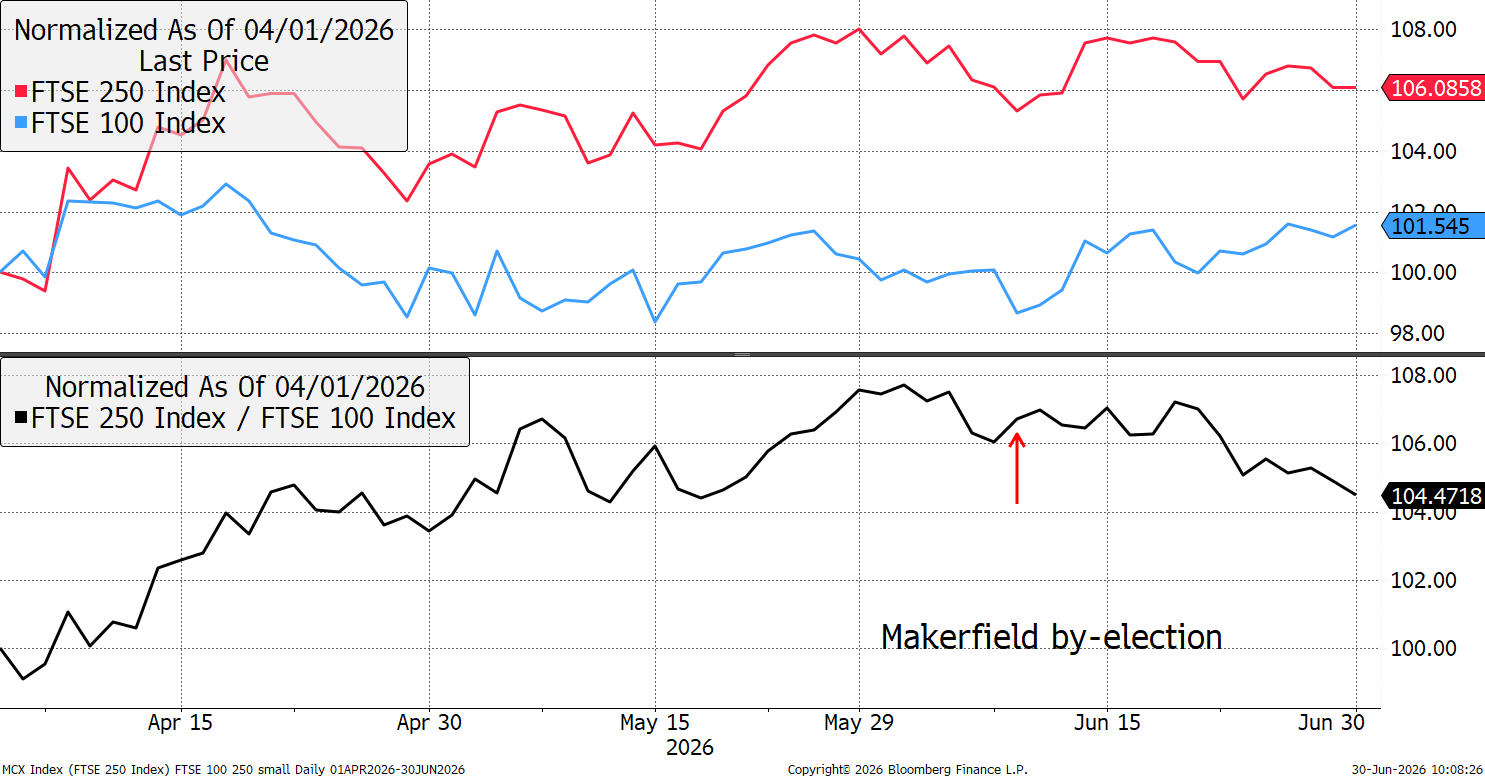

I also highlighted a more relevant test – the FTSE 100 versus the FTSE 250. Policy that is expected to see a boost to growth would likely see the FTSE domestic mid-caps beat the more global FTSE 100. Early days perhaps, and the modest slide in the FTSE 250 may be mere noise, but there was certainly no evidence of an impending surge in UK growth. I have no doubt that would have happened under a well-received set of growth policies.

FTSE 250 versus FTSE 100

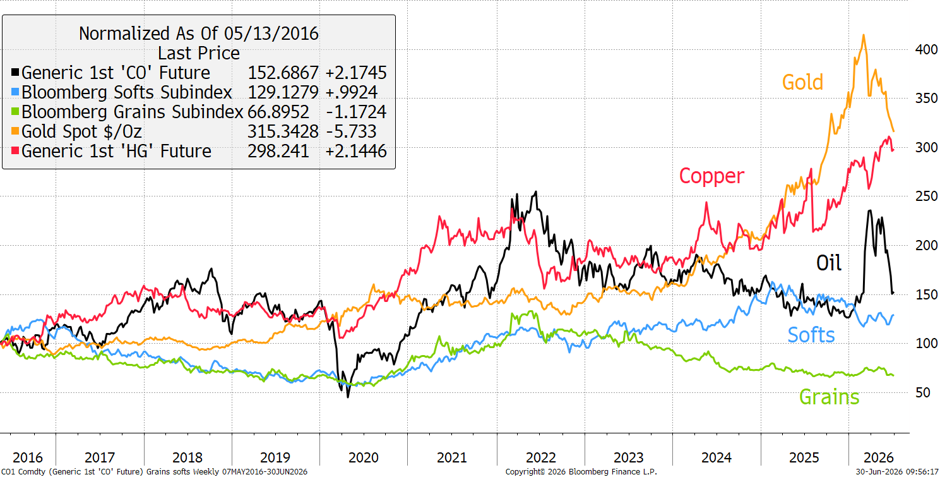

Commodities

Late last year, and earlier this year, I started to reduce gold following the surge and diversify into the commodity laggards such as oil and agriculture. Although gold is the long-term outperformer, due to its monetary role, the idea is that commodity returns have a history of being somewhat mean-reverting. That means gold leads and the others should follow.

Major Commodities – Past Decade

Gold has come back quite considerably, but as I wrote last week in Atlas Pulse, I still believe gold is in a bull market. The fall in inflation expectations, which has also boosted the dollar, has been a headwind.

Copper has recovered strongly, while softs commodities (sugar, cotton, cocoa, coffee) have been stable. Yet oil and grains (wheat, corn, soybeans) have fallen back as expectations for peace in the Straits of Hormuz have grown.

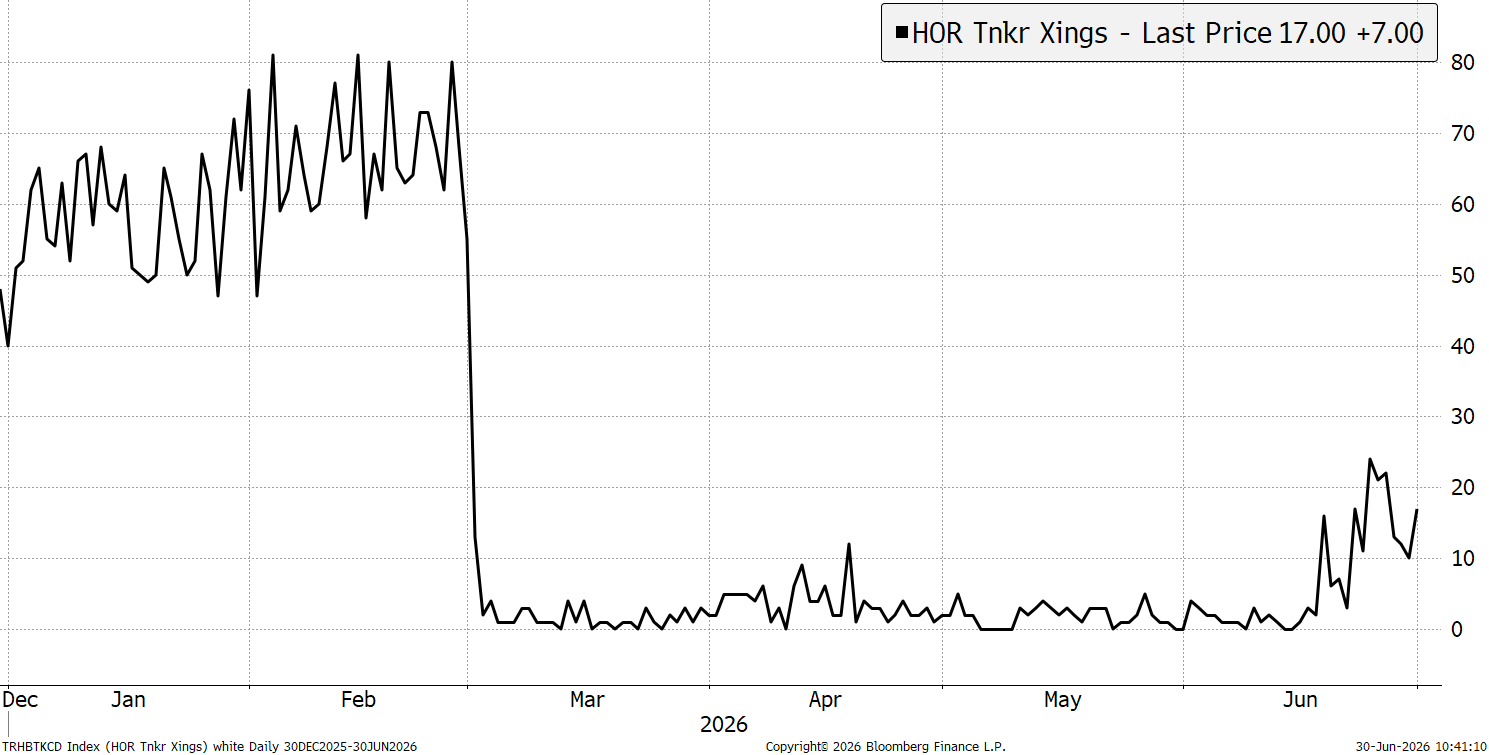

Oil Update

I believed oil and grains to be historically cheap, regardless of the supply disruption. Yet that disruption is real, and the Straits are only reopening slowly. Add to that the drawdown in oil inventories in the USA, and more importantly, China, and the oil price reaction is surprisingly optimistic.

Straits of Hormuz Tanker Crossings

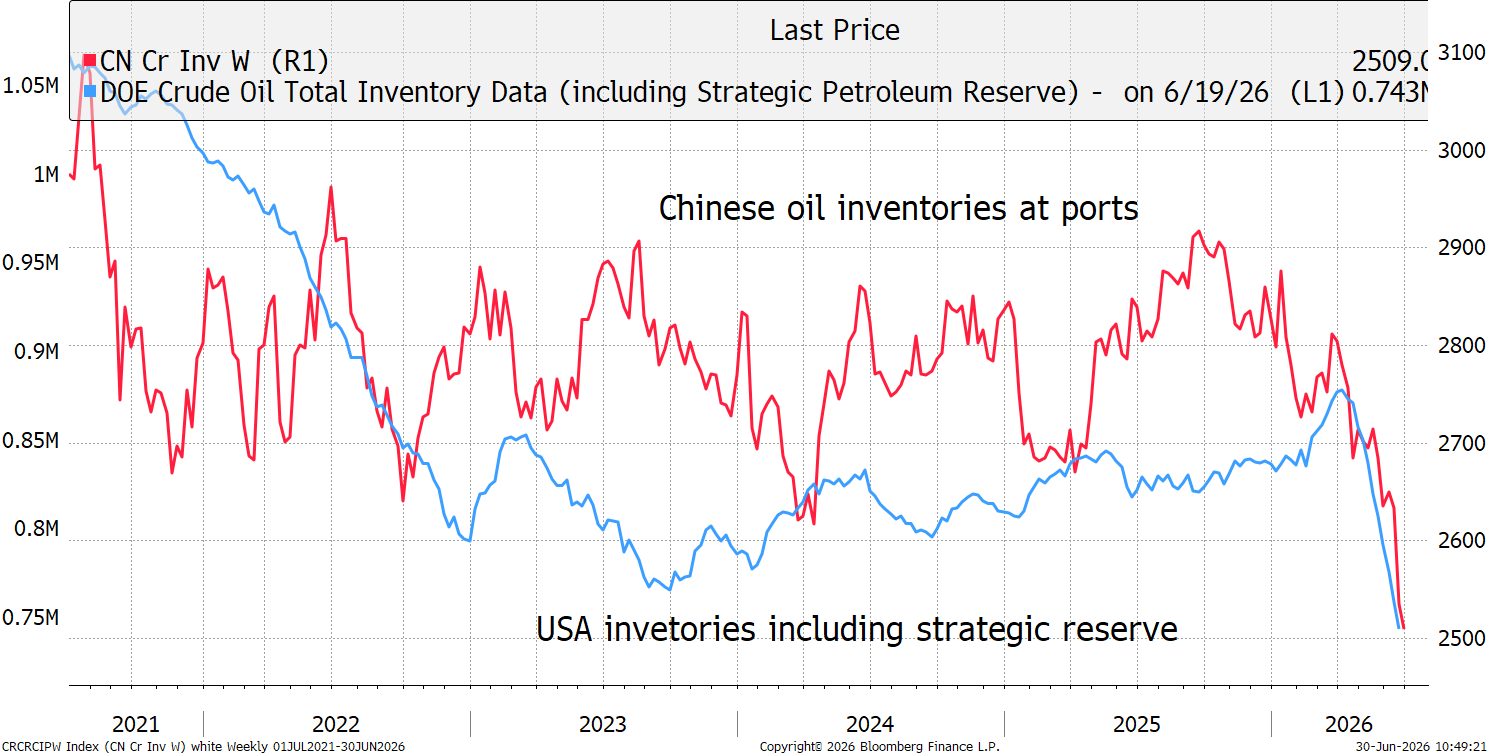

There is something funny going on, where there is no clear explanation as to when normal oil supplies resume, without drawing down inventories further. US levels are down to 1984 levels, and China’s (five years of data) are also falling rapidly.

Oil Inventories in the USA and China

There is also increased oil supply coming from Russia, which has risen by perhaps one million barrels per day, which is finding its way to Asia. Recall that sanctions were eased, not just by the USA, but even the UK. The UK government must have had a fit when they realised there was no choice but to comply, as sanctioned oil has become deeply embedded into global supply chains. Moreover, there are problems for Russian oil infrastructure, as it has become Ukraine’s strategic goal to destroy it.

While the price of oil has come back, I feel it is too early to tell whether this is a genuine long-term reaction representing a major shift in the oil market, whereby the Straits have become irrelevant, or just financial trickery. The latter still seems likely.

The pinch points are heavy fuels such as jet fuel and diesel, which drive the world economy. They remain firmer than crude oil and are not selling off as deeply. I still feel much more comfortable holding oil than not. I am fully aware that following the gold rush, commodities have been a drag on performance.

On agriculture, 2026 has been a good season for production in the main growing regions, despite the early surge in fertiliser prices. Supply has remained ample, the panic is behind us, but the bull case is supported by very low prices.

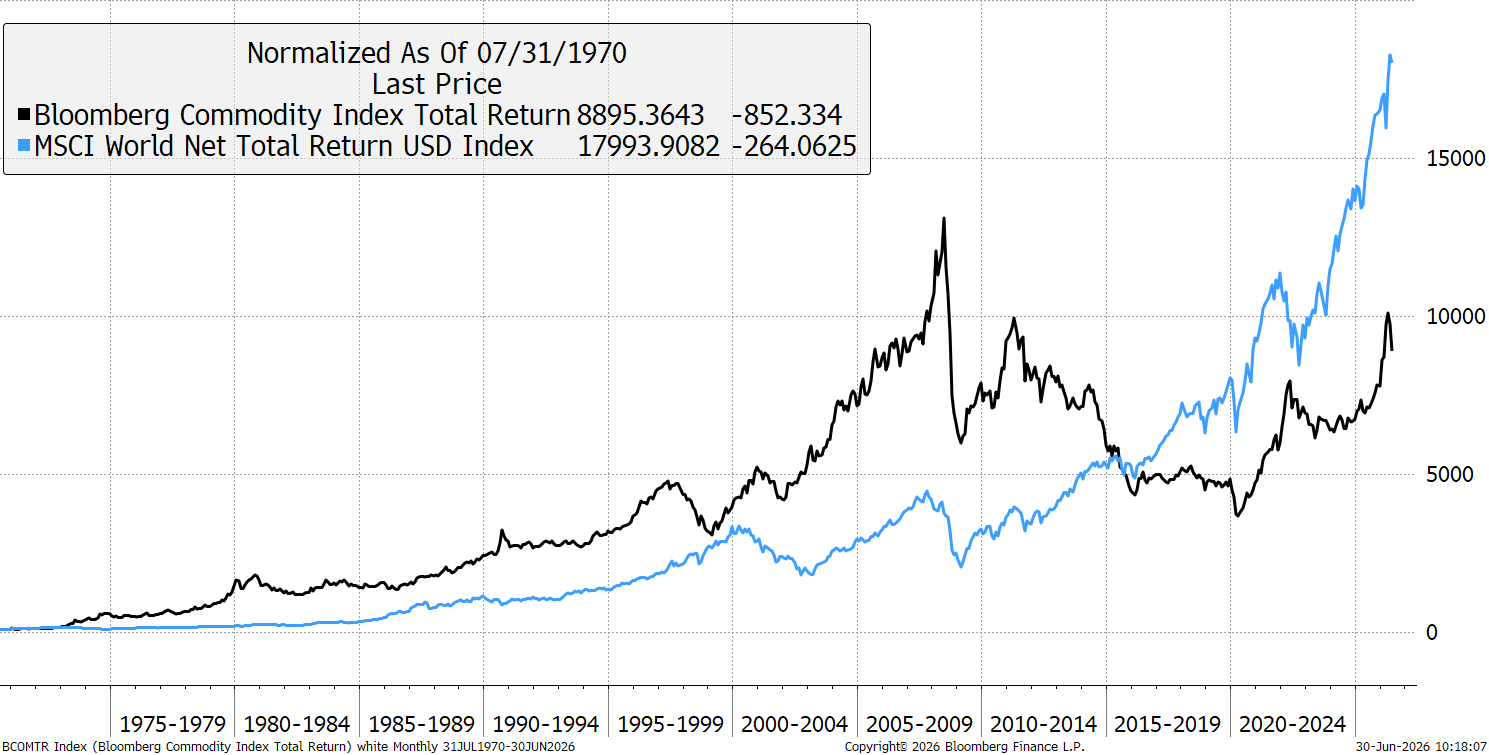

Longer term, commodities have been no slouch against the stockmarket but have lagged behind since 2008. It is their ability to offer diversification that I find so compelling in making them an important part of portfolios.

Commodities Versus Global Equities since 1970

The case for a bullish outlook seems strong. The caveat could be that demand is falling as the underlying economy is weaker than we currently believe. With much of growth connected to the AI boom, it is thinly spread across the population. This has been true for some time, and house prices are falling around the world, while the consumer tightens their belt. I think sustained slow growth remains the norm rather than a slump.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd