The Church and the Casino

Trade in Whisky;

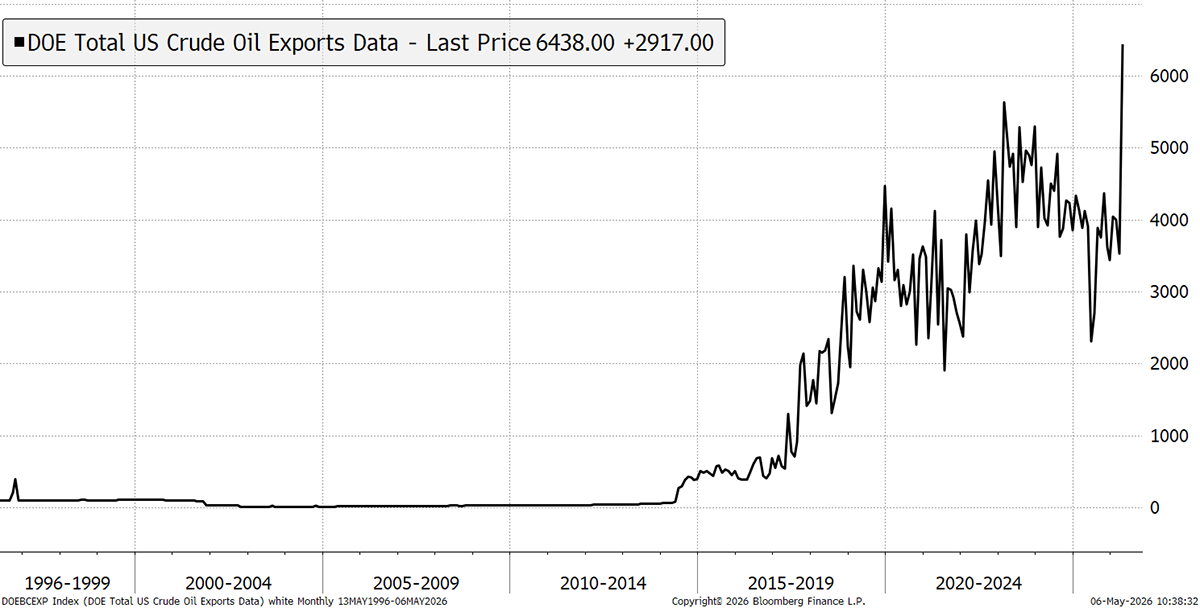

The stockmarket is up today, as yet another peace deal with Iran is in the pipeline. These announcements keep on coming whenever the oil price makes a new high, as it did last week. Yet the Strait remains closed. The only winner, at least economically, seems to be the USA, which has stepped in as the supplier of last resort. They have exported 250 million barrels since the war began, making them the largest crude exporter.

US Oil Exports

The longer-term price of oil remains high, and now indicates that whatever happens, the price will remain high for the rest of this year. According to Bloomberg News,

“US inventories are quickly depleting, with total oil and fuel stockpiles drawing down for four straight weeks to below historical averages. Meanwhile, America’s oil producers are struggling to keep up.”

In recent days, Iran resumed attacks on the UAE’s critical oil infrastructure. Yet the ceasefire officially holds, and the US has downplayed the prospect of returning to an active war.

It is a reminder that commodity prices will remain high due to supply disruption. Meanwhile, the stockmarket continues to rise in an unusual environment where the consumer is weak but capital investment, especially in digital, remains high.

While the US market is enjoying its relative shelter from the other side of the world, markets are basking in the sunshine, yet not fully digesting the risks. In a recent interview with CNBC, Warren Buffett said:

“The market always feels like a church with a casino attached. People can move between the church and the casino. There are more people in the church and more people in the casino, but the casino has gotten very attractive to people… it isn’t our ideal environment to invest record cash… but we’ve got the right management, and we can we pick our spots.”

It is at times like these that we need to listen to people like Buffett. He took over as the CEO of Berkshire Hathaway (BRK) in 1970, where the AGM took place over the weekend. At 95, Warren Buffett has handed the reins to his new CEO, Greg Abel, who trained as a chartered accountant, and investors want to know what he will do with their $380 billion of cash reserves.

In 1992, Abel joined CalEnergy, a geothermal electricity producer. In 1999, BRK acquired a controlling interest. Abel first came to Buffett’s attention following the acquisition of the UK’s Northern Electric, now called Northern Powergrid Holdings. Abel climbed the ranks, becoming CEO of MidAmerican Energy (later Berkshire Hathaway Energy) in 2018. In 2021, Buffett named Abel as his successor, and he was made CEO in January this year. Buffett remains the chairman.

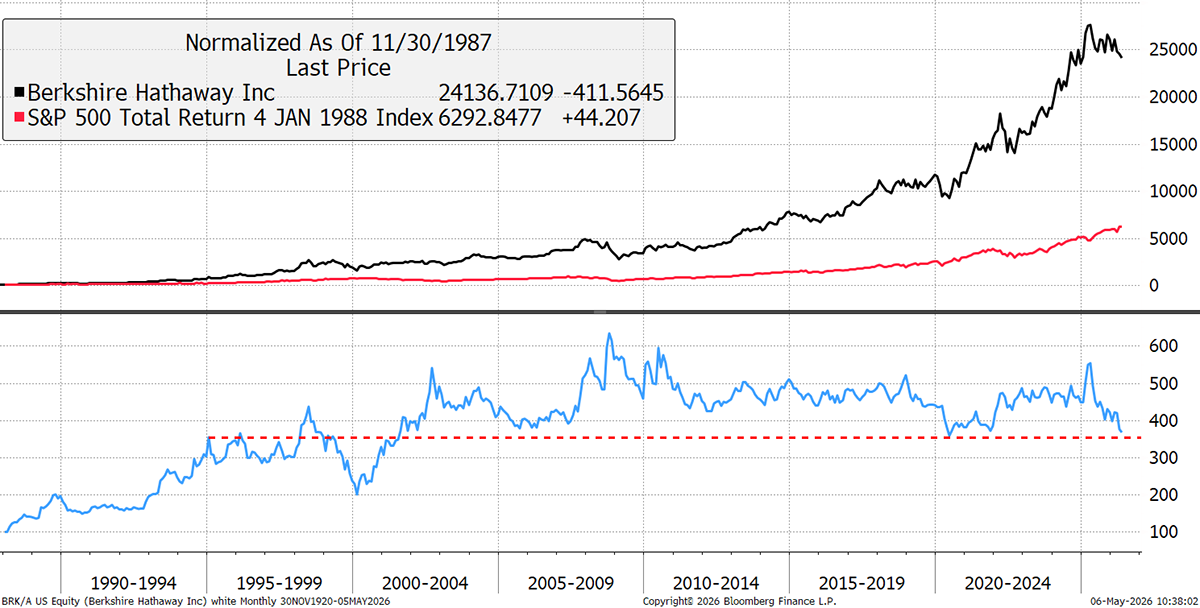

BRK was once considered an investment company, built on Buffett’s remarkable capital allocation skills. But, as the company grew, it has morphed into a conglomerate. Since 1987, BRK has beaten the market by 4x, but the surprise is that most of the gains had happened by 1994.

Berkshire Hathaway vs the US Market (inc. Dividends)

Still, for a diversified conglomerate to keep up with the US market in a technology environment is no mean feat. While the early performance came from good stock picking, the later returns were driven by insurance operations and a growing collection of private companies.

The AGM was a major test for Abel, and his performance was exemplary. The tone was different, but the message was clear: continuity without theatrics. Abel outlined BRK’s capital allocation discipline, saying the company has found attractive businesses but has passed on them because valuations were too high. Sitting beside Ajit Jain, the head of insurance operations, he projected the kind of steady, complementary dynamic that some investors likened to Warren and Charlie. Buffett’s brief appearance, including a nod to Tim Cook’s success at Apple following on from Steve Jobs, was a reminder that transitions can be successful.

BRK is comprised of insurance, private companies, an investment portfolio, and cash. At $330 bn, the equity investment portfolio looks a little thin these days, certainly when compared to the $1 trillion BRK market cap. The largest holding is still Apple, but 78% of the shares have already been sold. There are also stakes in American Express, Coca-Cola, Bank of America, Chevron, Occidental Petroleum, Moody’s, and Chubb, alongside the Japanese trading companies.

The private companies are split between the railway (BNSF), utilities and energy, and Manufacturing, Service and Retailing. Some of the main brands include: Fruit of the Loom, Duracell, See's Candies, Dairy Queen, Pampered Chef, Acme Brick, Benjamin Moore, Johns Manville, Shaw Industries, MiTek, Apparel/Footwear: Brooks, Justin Brands, H.H. Brown, Nebraska Furniture Mart, Jordan's, R.C. Willey, Star Furniture, Precision Castparts (aerospace), Lubrizol (chemicals), Marmon (diversified), McLane (distribution/logistics), NetJets (fractional jet ownership), FlightSafety (aviation training), Pilot Flying J (travel centres), Clayton Homes (manufactured housing), Berkshire Hathaway Automotive (dealerships), Oriental Trading.

It is quite something, and while the market waits for the $380 billion cash pile to be spent on a major acquisition in a mega deal, it is much more likely that they acquire many more smaller businesses.

The most important driver of the excess returns comes from the insurance operations. BRK uses its pristine balance sheet to underwrite risk around the world. They do so at a large scale and at the right price, with a discipline never to chase business. Their track record has been highly profitable, often from taking advantage of major disruptions. For example, after the 9/11 terrorist attacks, it was BRK that kept the planes flying. In 2008, when AIG went down, BRK stepped in. You can be sure they’ll be active in the Strait of Hormuz, at the right price, that is.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd