It’s been a busy week for the central banks and data releases. The Federal Reserve held rates steady while giving strong signals for cuts in September. The Bank of England cut by 0.25%, and the Bank of Japan hiked for the first time since 2007. With all this sudden disparity, it’s likely a good time to own a macro hedge fund, but make sure it’s a good one because most aren’t.

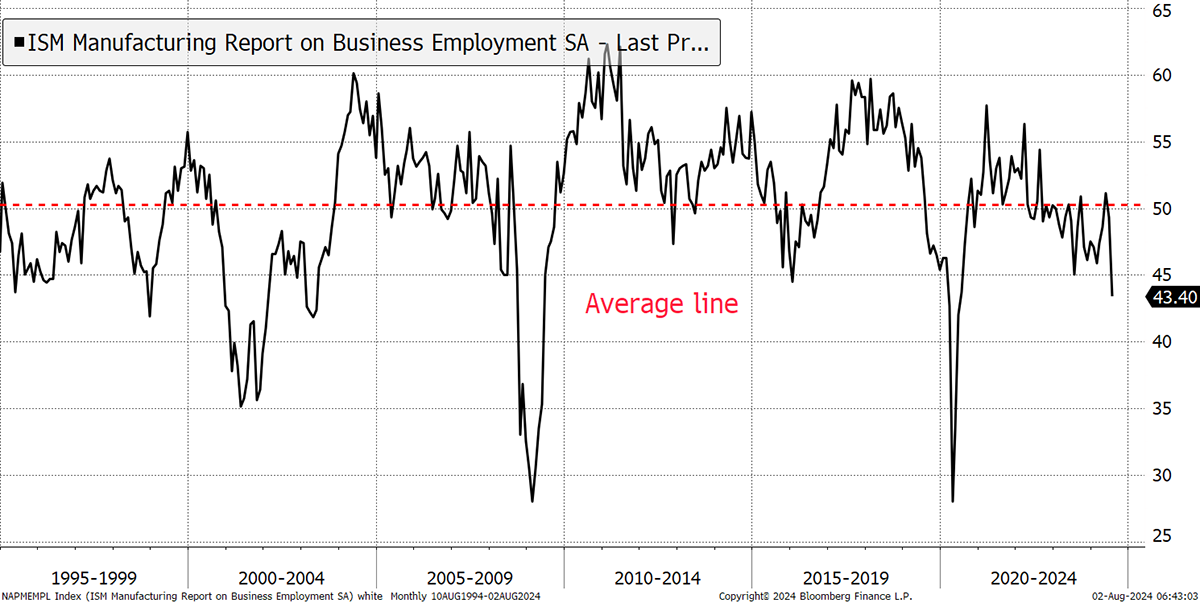

Then, the US employment data was released yesterday, and it keeps pointing towards a slowdown. Bloomberg’s John Authers interpreted the negative market reaction as a sign that the Fed has made a policy error by leaving the cuts for too long. Business employment is contracting, which heightens the risk of a recession.

Weak Employment Data

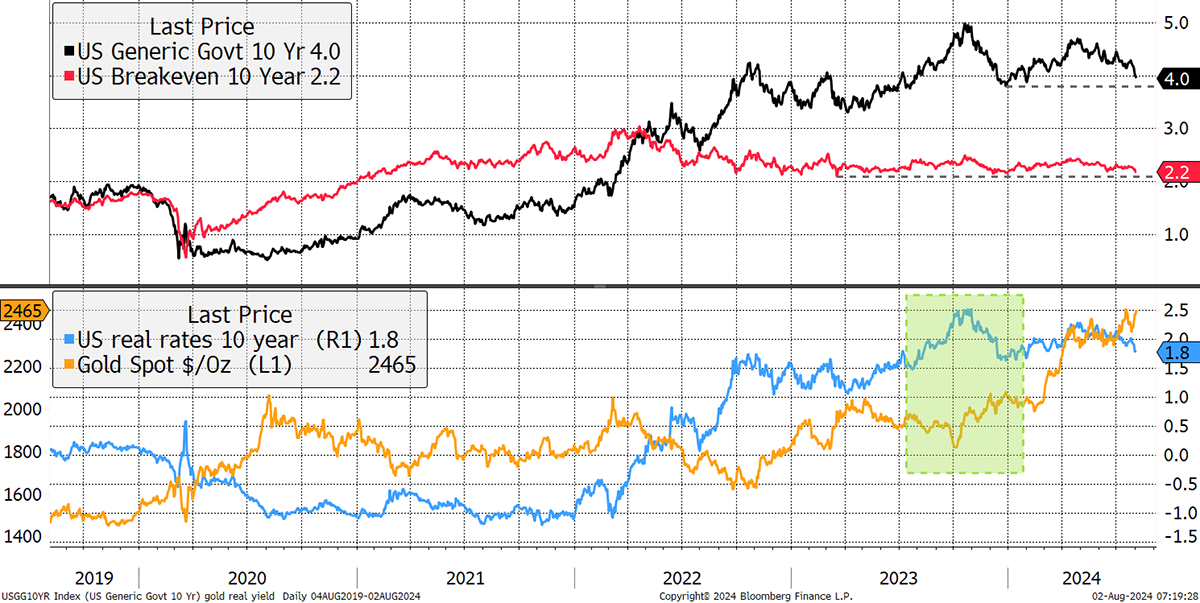

Looking at the bond market, the 10-year treasury yield fell, along with inflation expectations (breakeven rates). However, it is notable that neither line has yet made a new low below the previous major low. That tells me it’s not yet time to panic.

Yet what is bad for the economy can be good for gold. The real rates (rates less inflation) are now falling again, and the inverse relationship has kicked in. In truth, it never went away despite predictions of its demise. But gold did reject a brutal bond bear market in recent years and is seemingly the only asset that seems to embrace the carnage around us.

Gold and Real Yields

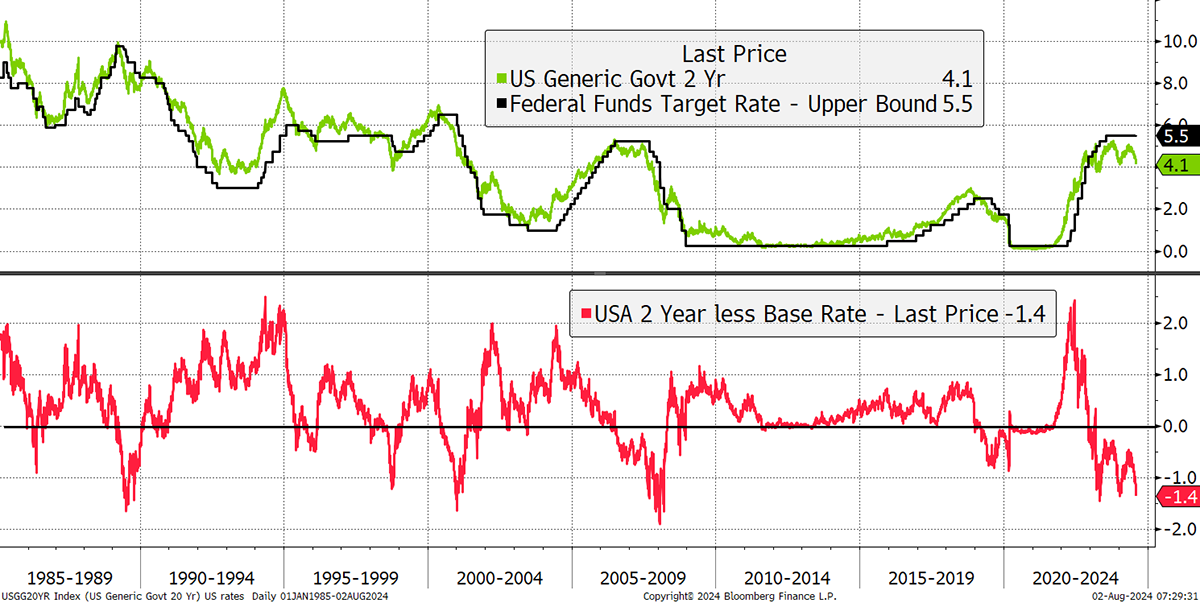

The shorter-term two-year yield and the base rate (set by the Fed), highlight how the market believes the Fed are behind the curve. For over a year, the two-year has traded around 1% below interest rates, implying the market expects cuts. Previous occasions include the late 1980s housing bust, the 1997 Asian Crisis, 2000 Dotcom, and the 2008 banking crisis.

The Fed Is Behind the Curve

With China slowing down as well, there is no longer a natural offset that has been so supportive in recent decades. Some believe carnage is coming; others are more sanguine because they believe the might of stimulus will soon kick in. Then there’s the US dollar, which normally rises when things get tough, and it isn’t. Could that be an early sign that the stimulus helicopters are on the way? A weak dollar is a blessing for global markets.

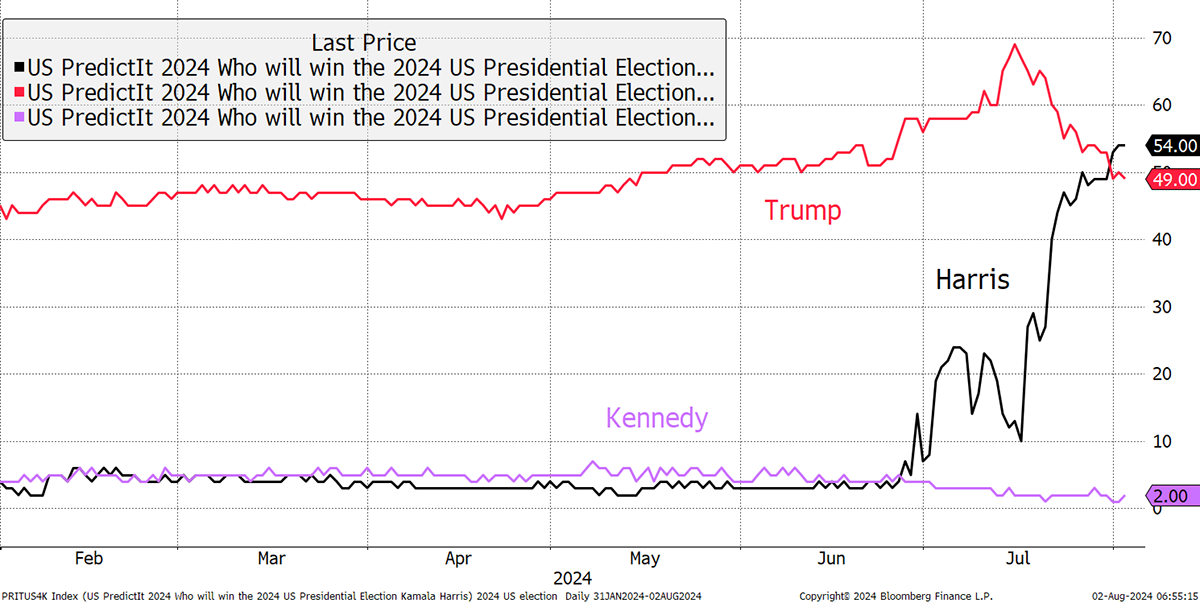

If the uncertainty from the macro isn’t enough, then consider the politics. The markets have also felt the pressure of disruption. Knowing that Trump was going to win was a known-known, whereas Harris is a known-unknown, and she’s in the lead.

Harris for President

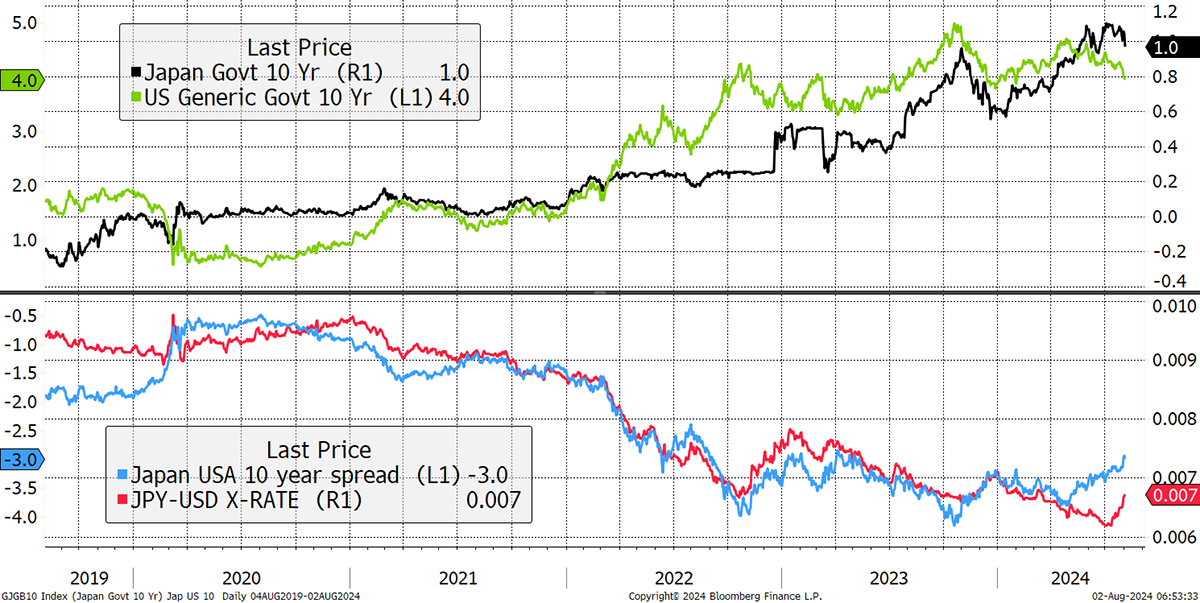

This brings us to the yen, the other major external factor other than China. The spread between US and Japanese rates is finally closing. This is coming from both directions, as US rates are falling while Japanese rates are rising. I showed the extraordinary cheapness of the yen last week. This week, I show the currency against the yield spread. The yen has a long way to go.

Rates and the Yen

A Week at ByteTree

In Venture, I recommended a German speciality pharmaceutical business, which is growing quickly and expanding across Europe.

In Whisky, I took profits in Pakistan equities which have done well over the past year. I also discussed Pershing Square (PSH) which we sold last month.

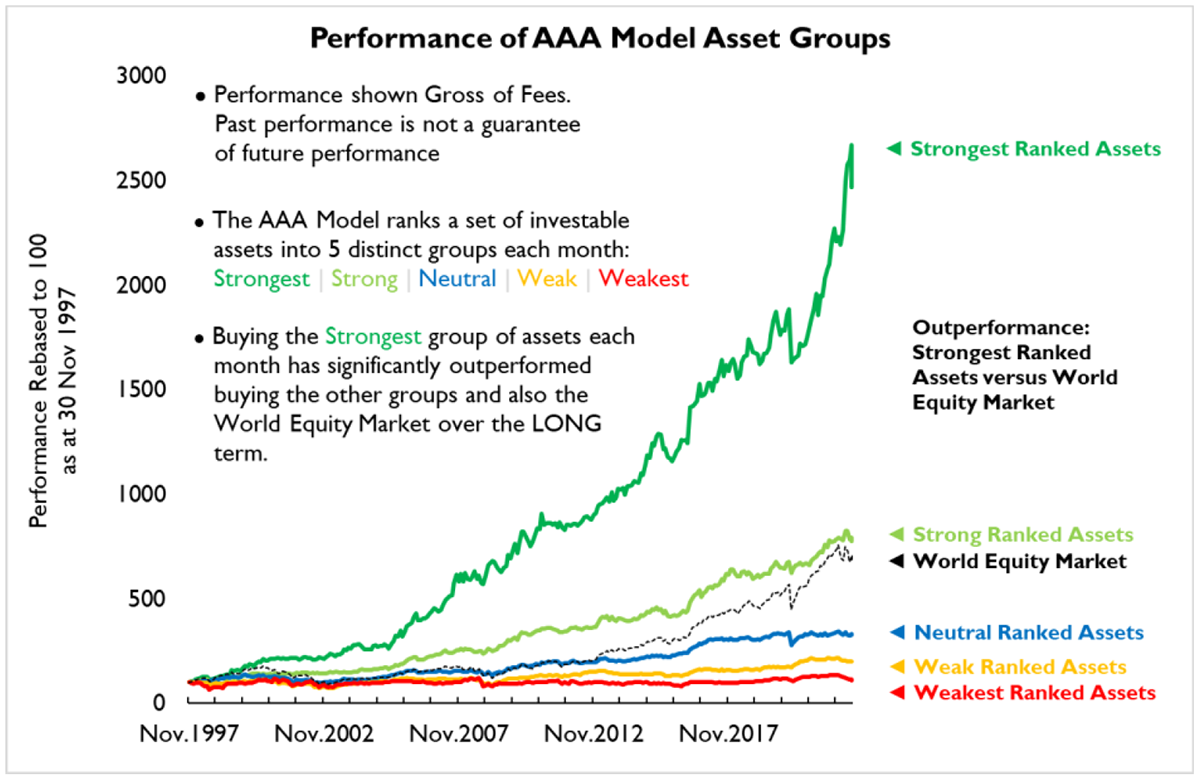

In The Adaptive Asset Allocation Report (AAA), Robin and Rashpal told us, “the future is not what it used to be”, another fine quote from Yogi Berra. They covered the retreat in technology stocks, the yen, rates, and gold. In each case, with a fresh perspective. It’s always a great read with stunning long-term performance.

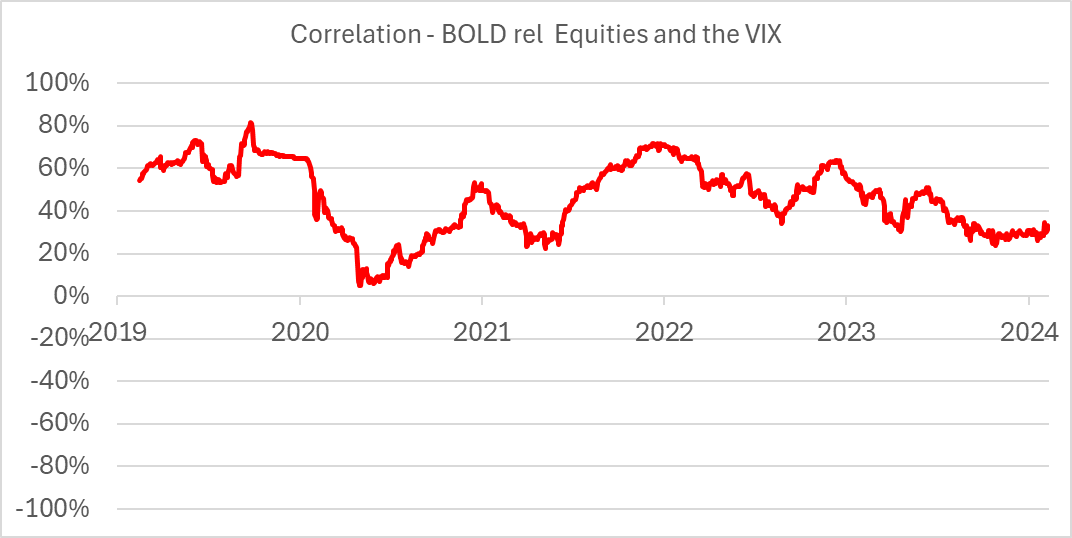

I also covered the rebalancing of the BOLD Index. I explained why I believed that BOLD seems to have it all, as it blended gold’s defensive qualities with Bitcoin’s habit of making money (albeit in a chaotic manner). Not just that, but BOLD’s performance against the stockmarket has a positive correlation with the VIX, a sort of market panic index.

It seems that BOLD beats the stockmarket on the way down by being more defensive, and hold’s its own during the bull runs. That makes it a defensive, high-quality asset. Remarkable.

Finally, in crypto, we discussed what would be the catalyst for the next major crypto rally, and a Presidential Decree would surely help. The analysts also looked at Akash (AKT), Internet Computer (ICP), Raydium (RAY) and Helium (HNT). Akash has been reaping the benefits of the AI boom, while Raydium is basking in Solana’s strength.

I’m off on holiday for a week. My wife is driving, while Clemmie, Cosmo and I will be going by sea. I hope it’s not too far to go, but I will have my laptop with me and will send a short note if the wind picks up.

Have a great week!

Charlie Morris

Founder, ByteTree