Trade in Whisky;

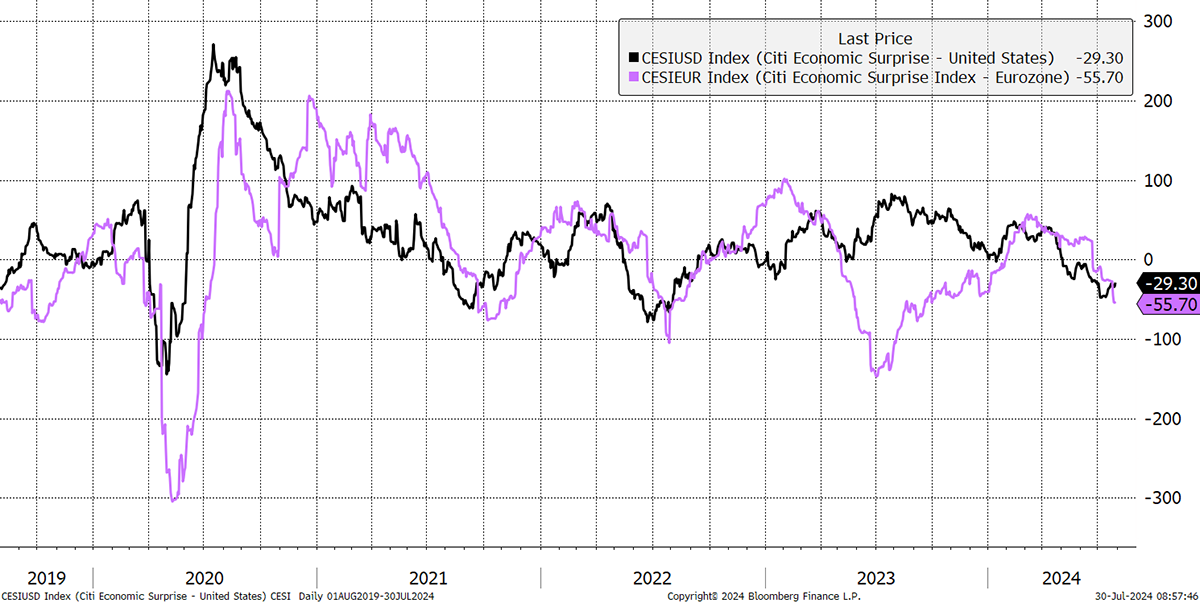

Consumers are feeling the pinch, and with another bout of political uncertainty, parts of the stockmarket are starting to feel the pressure. Either that, or it’s just the summer, which is the weakest part of the year for stockmarkets. Yet this summer, the economic surprise indices are pointing down in both Europe and the USA at the same time.

Negative Surprise

The surprise indices observe the economic data as it comes in, such as employment, tax receipts, inflation, trade and so on. It then decides whether it’s positive or negative, according to what was expected. Finally, it adds or subtracts from the index to give the result. Rising is deemed to be positive, and falling, negative. While early 2023 saw a strong USA and a weak Europe, late 2023 saw a strong Europe and a softer US. This time, they are falling simultaneously.

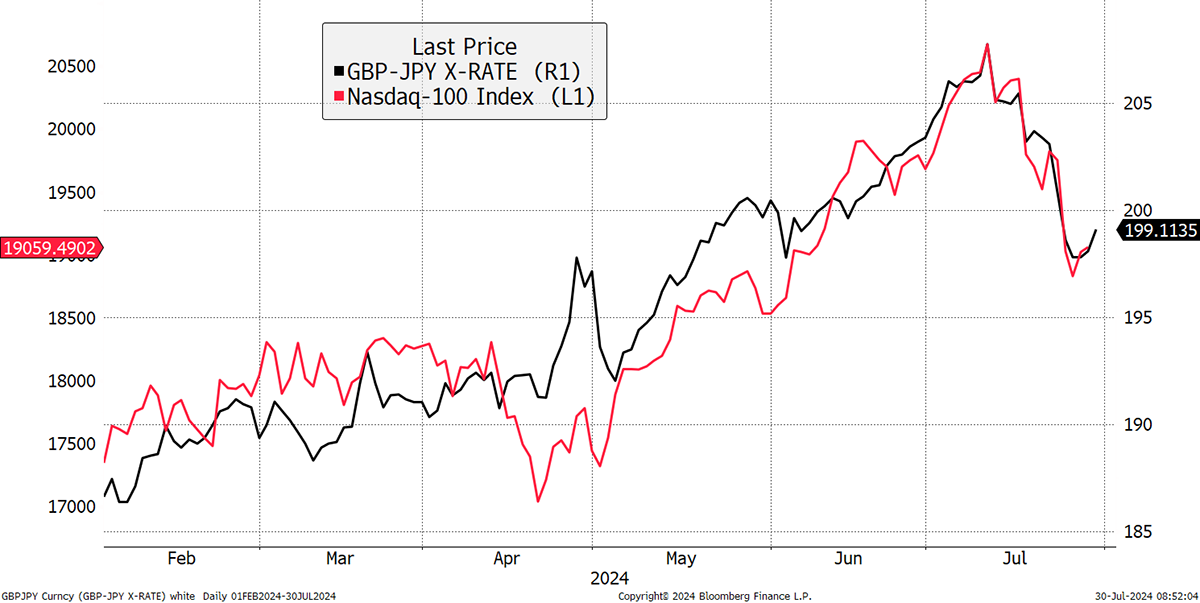

That has translated into a dip in the leading technology stocks (red), which has been countered by an upturn in the yen (black inverted). The nature of the close inverse correlation demonstrates how it is reasonable to expect the yen to continue to perform should stockmarkets get into trouble. Furthermore, the Bank of Japan meets on Thursday, and 14 out of 48 economists polled by Bloomberg think the first interest rate hike in many years is coming. If Japan is increasing rates, and the US is cutting, the yen will soar. High time.

The NASDAQ and the Yen

If things are cooling, then why not just own the long gilt? I have considered that, but there is political risk attached, as I am sure you have read in the papers. More importantly, the yen is much less volatile than the long gilt yet has so much more potential to rally when the economy cools, with far less downside in a rate hiking cycle. See 2008 for more oomph and 2022 for less risk.

The Yen and Long Gilts

I am not suggesting I am pleased with how the yen trade has turned out, but the case remains strong, and none of the reasons have changed to keep on holding it.

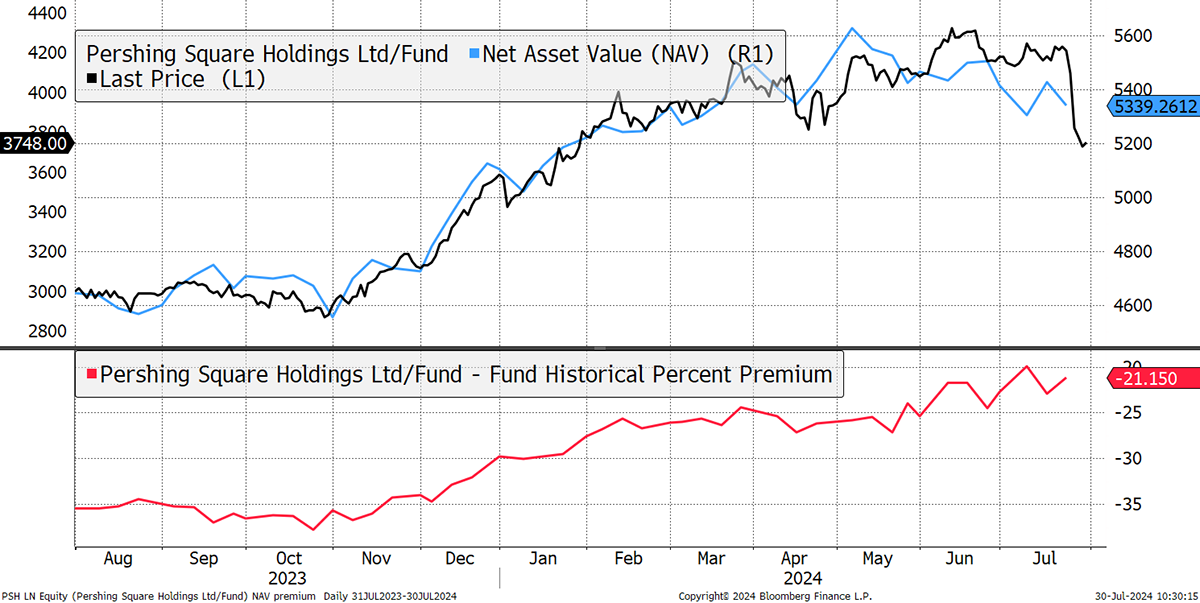

There were other notable moves in things like Pershing Square (PSH) which sold off sharply last week. PSH was impacted by weakness in consumer stocks. Their largest holding, Universal Music (UMG Netherlands) fell 29%, and their second holding, Chipotle Mexican Grill (CMG) fell by 26%. The strange thing is that PSH shares are only down by 15%, which is why the discount appears to have tightened. The next NAV will be released tomorrow, and that will reflect the price drop.

Pershing Square

We bought PSH on 14 November 2023 at 3,048p and sold it on 2 July 2024 at 4,150p. It worked out well, but most of the gain came from the narrowing of the discount.

I have another sale today, and despite having several options for reinvestment, I am happy to stand back until the markets offer a more compelling set-up.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd