The International Toll Booth

The "SaaSpocalypse" was based on an uncertainty shock.

An industry which had a very narrow set of possible outcomes (very high retention, stable pricing regimes), suddenly saw its range of possible outcomes expand. This explosion of uncertainty has been reflected in a dramatic downward repricing.

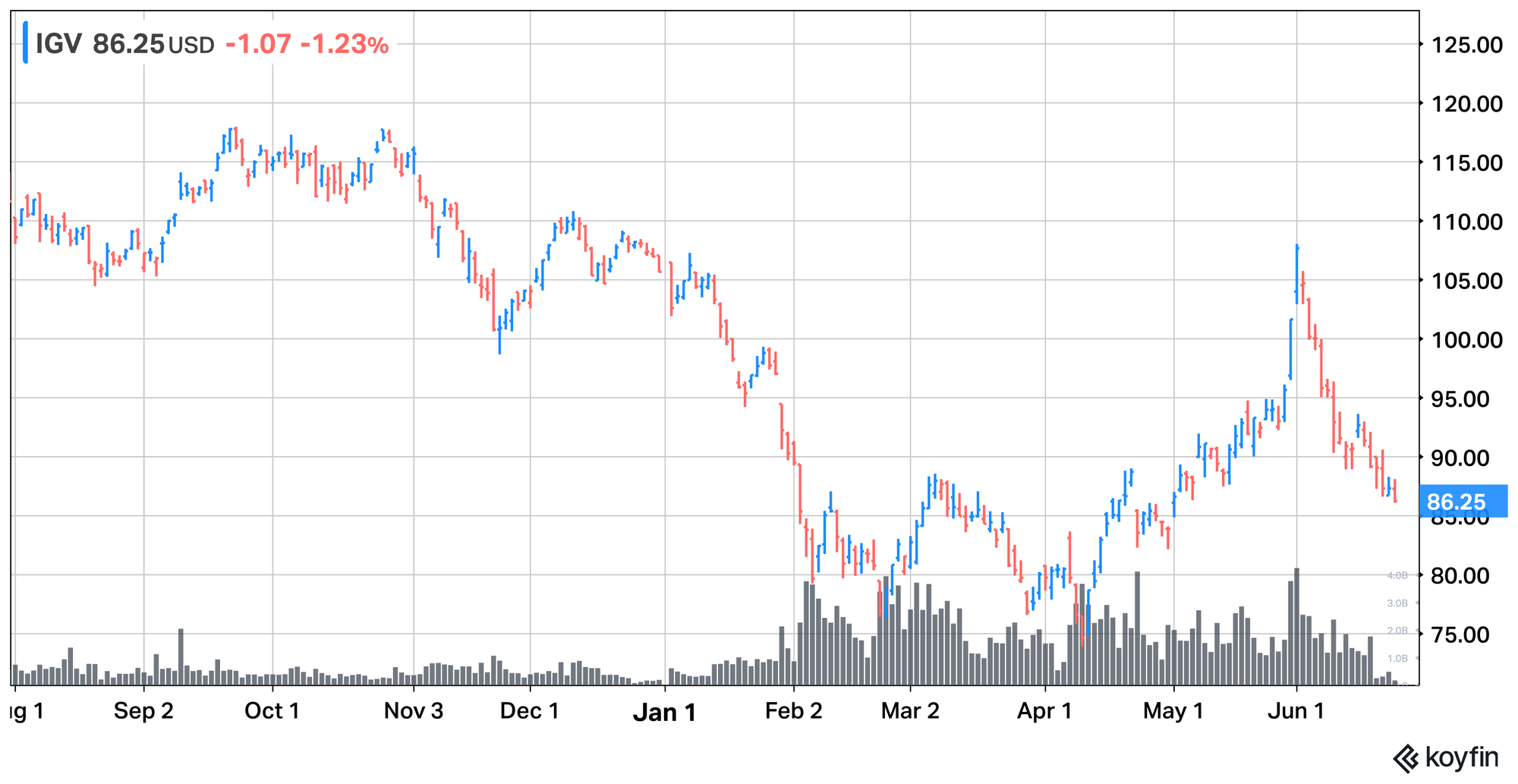

Software Stocks' 35% Fall

The Nomad Partnership, which returned around 1000% in 14 years under Nick Sleep and Qais Zakaria, had a concept they called The Cone of Uncertainty. Here, what mattered was not simply the most likely pathway/outcome, but the number/breadth of possibilities around that. A narrower spread was preferable.

It’s possible that the average expectation for growth in the software industry is largely unchanged from a year ago, but that the confidence in that average is what has diminished. Thus, it is not simply the base case that matters, but the extremity of the bull/bear cases either side of it, and their relative likelihoods. Instead of expected growth rates of 8/10/12 percent, with a 90% chance of 10 and 5% of the others, it’s now 0/10/20, with a 33% chance for each. Same average, wider cone. These numbers are illustrative only, to outline a framework for how to think about the selloff in SaaS companies.

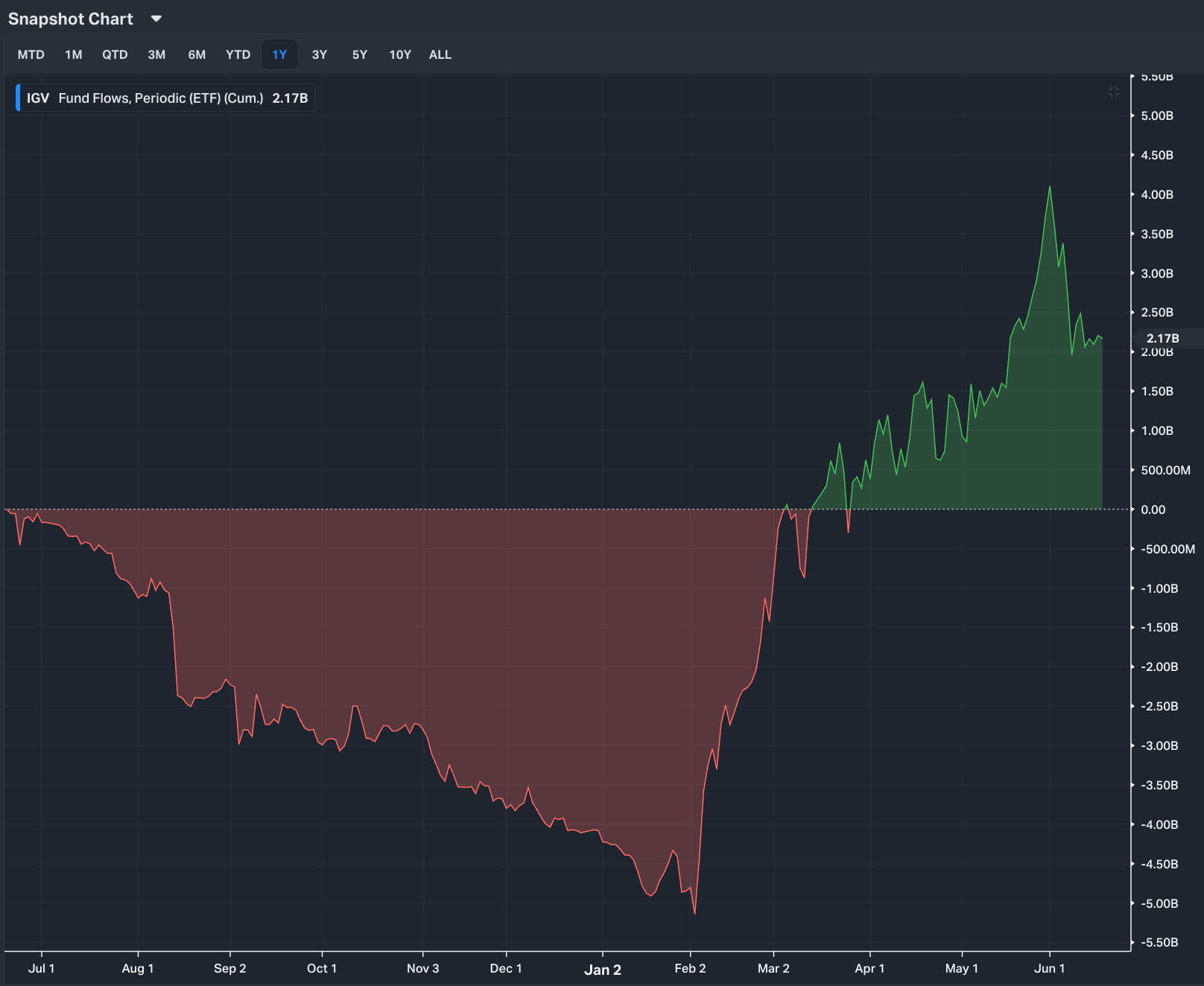

Fund flows into IGV, the American software ETF, were negative from mid-2025 all the way to February this year. Interestingly, on February 3, those outflows switched to inflows. The ETF didn’t actually bottom, in price terms, until April 10, after which it surged by 45% in just 10 weeks, before falling back again in June.

Software ETF Outflows Turn to Inflows

Since software companies capitulated in February 2026, investors have had four months to assess the situation. In that time, it has been possible to build the first outlines of how AI is actually impacting these companies and industries. We are moving away from panicky speculation, and starting to add colour in certain areas, re-gaining a more confident footing about the likely future pathways. The Cone of Uncertainty is narrowing again. As the last two weeks have seen renewed weakness for some software companies, others have shown more resilience, reflecting their more essential nature.

Today, we add our 23rd stock to the quality portfolio, which is now over 90% invested. Following this addition, there will be room for two more stocks. With broad geographic and sector diversification, it is exposed to high-quality companies at low prices around the world in multiple sectors. It has a defensive posture, preferring companies with low debt, great cultures, essential products, and attractive economics. Portfolio volatility is low, and it has little exposure to the riskiest sectors of the market, where downside potential is high.

ByteTree Quality is building a resilient portfolio for long-term investors, and today, we make another promising addition.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd