Animal Spirits

In 1999, Pets.com was one of the most famous bubble stocks, commanding a huge market cap with little to show for it in business terms. It went public at $11 a share in early 2000, near the peak of the dotcom bubble, with backing from Amazon and Merrill Lynch, and went bankrupt a year later. Today, a different bubble is forming.

Our mission for the ByteTree Quality Portfolio is to identify outstanding companies trading on surprisingly low valuations. We are currently in a narrow bull market, dominated by a few dozen AI-related stocks, and capital is being sucked away from the edge and into the middle. The edges that are left dry of capital form the anti-bubble, and it’s an excellent hunting ground for long-term investors who, sensibly, are unwilling to enter this remarkable tech hardware rally so late in its run.

Our next company dominates a market segment that has been with us for millennia and will remain a major feature of human life forever. The industry saw a few years of demand pulled forward during the pandemic, for reasons that will become clear. However, that meant when 2023-2025 came around, demand dropped, as it had already been met. Then, coming out on the back of the Covid whiplash, the company faced another issue: the weak US consumer.

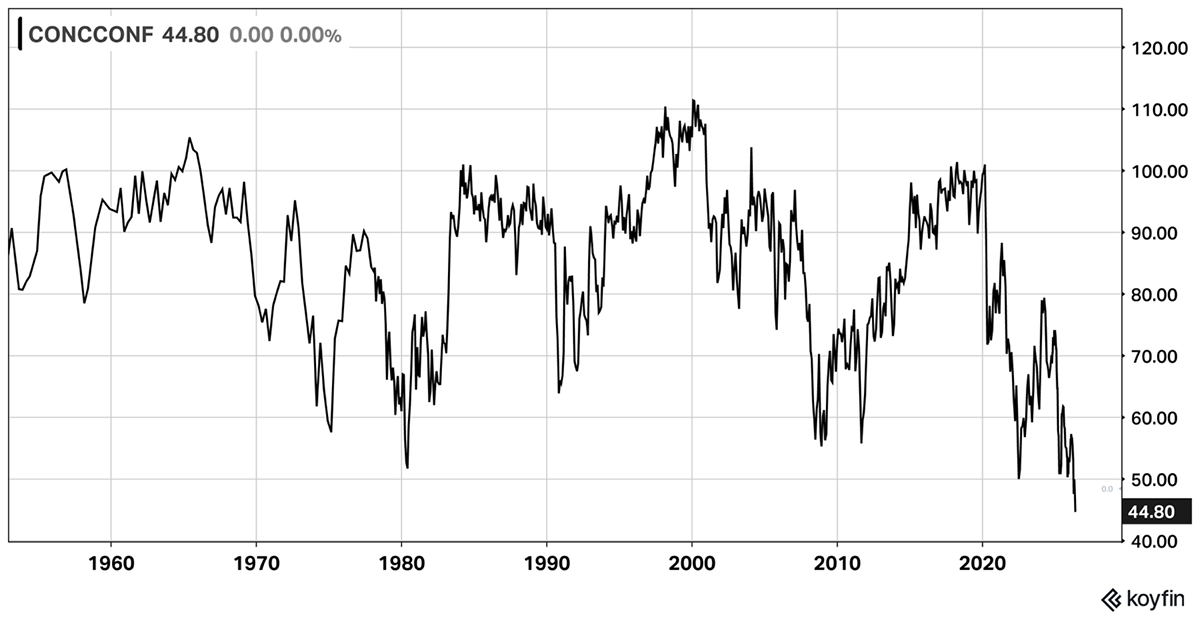

Consumer sentiment in America has never been this low. The prospect of another round of inflation, caused by higher energy prices following the Iran War, has tipped them over the edge. While the stockmarket has boomed, Wall Street has thrived while Main Street has suffered. In fact, this is the lowest reading on the University of Michigan’s Consumer Sentiment survey since WW2, driven by the cost of living, with “57% of consumers spontaneously citing high prices as eroding their personal finances”. It wasn’t that long ago that the “remarkable” US consumer was seen as the only thing propping up the stockmarket, but those days are gone.

US Consumer Confidence

Today, we make a new addition to the ByteTree Quality portfolio, which stands to benefit should this record-low confidence turn around, just as it always has before. Along with lockdown-specific dynamics, weak confidence has made this company’s formerly glowing sales record look underwhelming in the short term. Having historically grown at 4-8%, last year’s growth fell to 2.5%.

However, what is important is that the reaction to this has been exacerbated by two things. Firstly, the high valuation reached during the good times, and secondly, the stockmarket’s preference for high-growth, AI-related stocks. Together, these have taken the stock down by two-thirds. As a result, it is now at its best-ever valuation multiples and is a good place to invest for the long term.

They say that predicting the rain counts for nothing – building the ark does. The Quality portfolio is now over 80% complete, having added 21 of the targeted 25 positions. We see excess and irrational behaviour at the centre of this bull market, and are putting the final few beams into the ark.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd