The Money Supply Boosts Markets

These are curious times in financial markets. The war in the Middle East has had a ceasefire, but the constraints in energy markets continue to build. There are fears of shortages, particularly in Asia and Europe, which could lead to high fuel and fertiliser costs and, potentially, economic stagflation. Yet stockmarkets have shrugged it off.

The oil price remains high by recent standards, but it is well below what would be deemed as shock levels. You can partially explain that with a short war thesis, despite continued disruption, and I’ll get to that. But the real surprise is the collapse in equity volatility. The VIX Index has dropped back to 18, which is just below pre-war levels. The markets are now unconcerned.

The VIX Is Below Pre-War Levels

While we humans react negatively to bad news, it’s one of those times to remind ourselves what drives financial markets. They are a price discovery system, and the answer is money. If there is more money in circulation, much of it finds its way into stockmarkets. March saw a contraction in the global money supply (G20 nations), which has sharply reversed since the ceasefire announcement in April. The money supply, at $116.6 trillion, has made a new all-time high.

Global Equities and the Money Supply – Past Year

Long-term, the link with equities and the correlation are close. Since 2004, the money supply has grown by 390% while the World Index is up by 352%, but if you add dividends, 507%.

Global Equities and the Money Supply – Since 2004

While the link is close, and explains much of long-term performance, it hasn’t always been right. The blue line shows the relationship between stocks and the money supply. In 2007, the drop was 53%, and in 2020, 36%. It reminds us that while many real events, such as wars and crises, are sometimes glazed over by stockmarkets, at other times, they really do matter.

The 2008 drop was clearly a reset following a period of exuberance. From 2010 to 2022, the range was between 60 and 80. Since 2024, this has broken into a higher range, whereby stockmarket are now rising faster than the money supply.

The new money has come from two sources. The first is China (upper blue), which has increased its money supply to boost growth following the real estate crash. It seems every country is increasing their money supply, albeit at different speeds.

Money Supply by Country

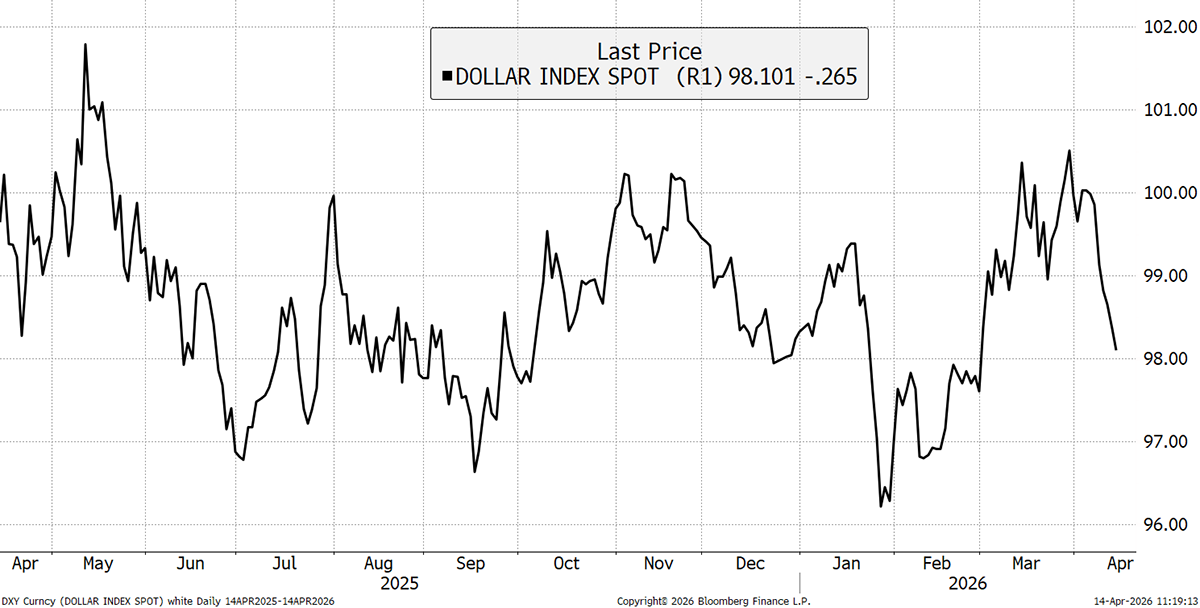

The other source of new money has come from a fall in the US dollar. This has been a sharp drop since the ceasefire announcement and has buoyed markets. The sharp fall in January buoyed the surge in gold, but the recent fall and the one last May did more for stocks.

Dollar Index

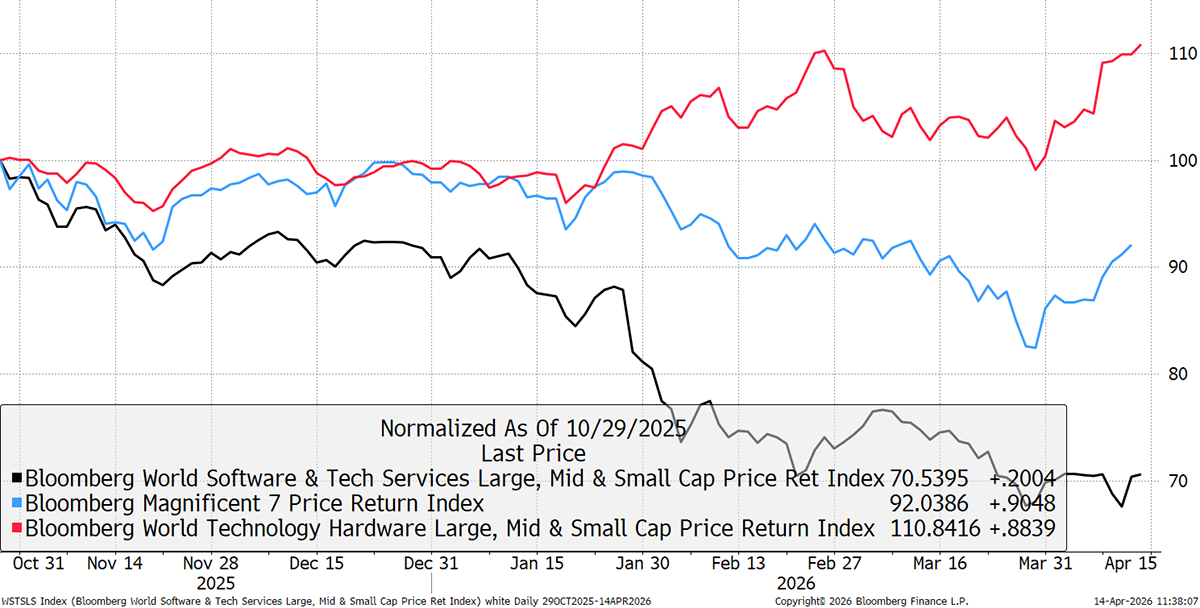

That said, the standout winner since the ceasefire has been technology stocks, specifically hardware over software. The race for chips and computers hasn’t let up, while software continues to be deemed an AI loser. The large US tech companies are in between but are no longer market leaders, as heavy investment in data centres is now seen in a negative light.

Technology Stocks in 2026

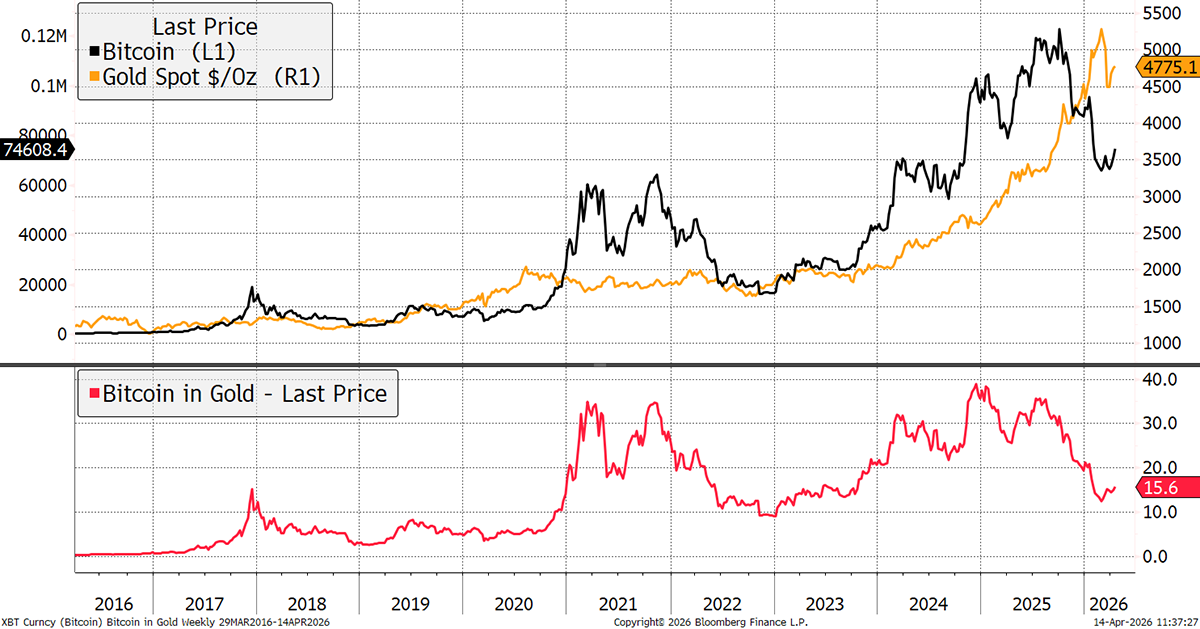

The recent boost in technology, which isn’t directly affected by the war in Iran, helps explain why Bitcoin seems to have turned the corner relative to gold. A Bitcoin was worth just 12.4 ounces of gold in February and is now worth 15.6. My hunch is that Bitcoin takes the limelight back from silver.

Bitcoin vs Gold

While the money supply boost partially explains why stockmarkets are trading higher in the face of disaster, sometimes these can dislodge, just as they did in 2008 and 2020, as shown earlier. It is helpful to understand why stocks have taken the ceasefire so well, but it doesn’t mean it can’t reverse.

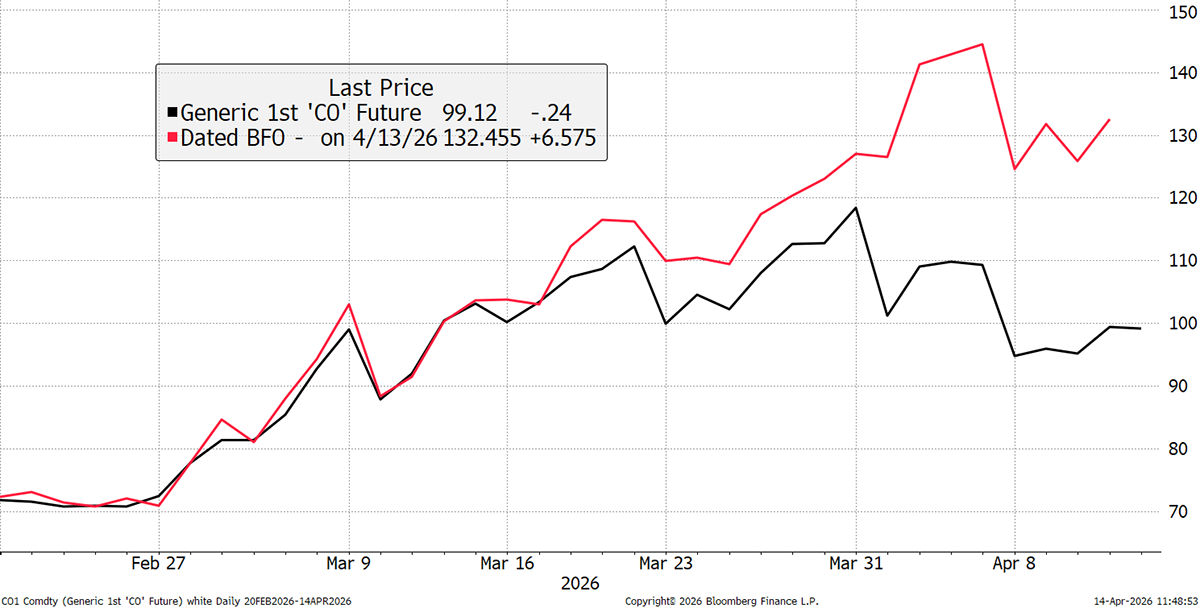

The Brent Crude Oil Futures (black), held in the commodities positions, remain close to $100. Presumably, financial markets see this as transitory, just as they did during the early Ukraine War. They are looking through the problems, knowing that all will be well in the end, so don’t price in a supply shock that will be short-lived. The physical market (red) is telling us that in the real world, rather than the financial world, oil is trading at a higher price than when the ceasefire was announced.

Brent Crude Physical vs Financial Futures

There is a sense that the markets can ignore oil because, in a year or so, it won’t matter. The US has won, or at least Iran has lost, and the oil will flow in good time. The oil tankers are heading to the US, Canada, and Brazil. Europe is taking more gas from Russia, Venezuela will boost production, and in the UK, we are increasing solar capacity. There are workarounds in the Middle East, with new pipelines in the making. Consumers are buying electric cars, and in a few years, oil demand will have taken a dive. There’s also the idea that the US blockade makes it much worse for Iran than the US, and in the end, the markets have learned that Trump always chickens out (TACO).

That underlines the prevailing market view, which is optimistic, but what if it is wrong?

Perhaps the money supply can lift markets for a while, but the physical oil shortages take time to bite. The energy shock is still in its early stages, and a recession follows high energy prices. The blockade of the Straits of Hormuz, whoever is doing it, is a lose-lose situation. If the world doesn’t get its energy, the planes will sooner or later be grounded. The fact that the airline stocks have rebounded, at least slightly, supports the idea that the market believes in the rosy scenario. The longer we have to wait for the ships to sail, the more likely it is that the world will face a recession.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd