ByteTree BOLD Index Monthly Rebalancing Report;

The 21Shares ByteTree BOLD ETP (BOLD) invests in Bitcoin and Gold. BOLD combines the world’s two most liquid alternative assets on a risk-adjusted basis. Due to their naturally low correlation, the diversification benefits of holding both assets have been unusually high. Bitcoin prefers risk-on market conditions, while Gold prefers risk-off.

The target weights last month were 28.1% and 71.9% (Bitcoin to Gold). Price changes over the month led to the last day’s weights at 30.9% Bitcoin and 69.1% Gold. This means the latest rebalancing has seen 1.1% added to Gold and reduced from Bitcoin to meet the new target weights.

BOLD Performance

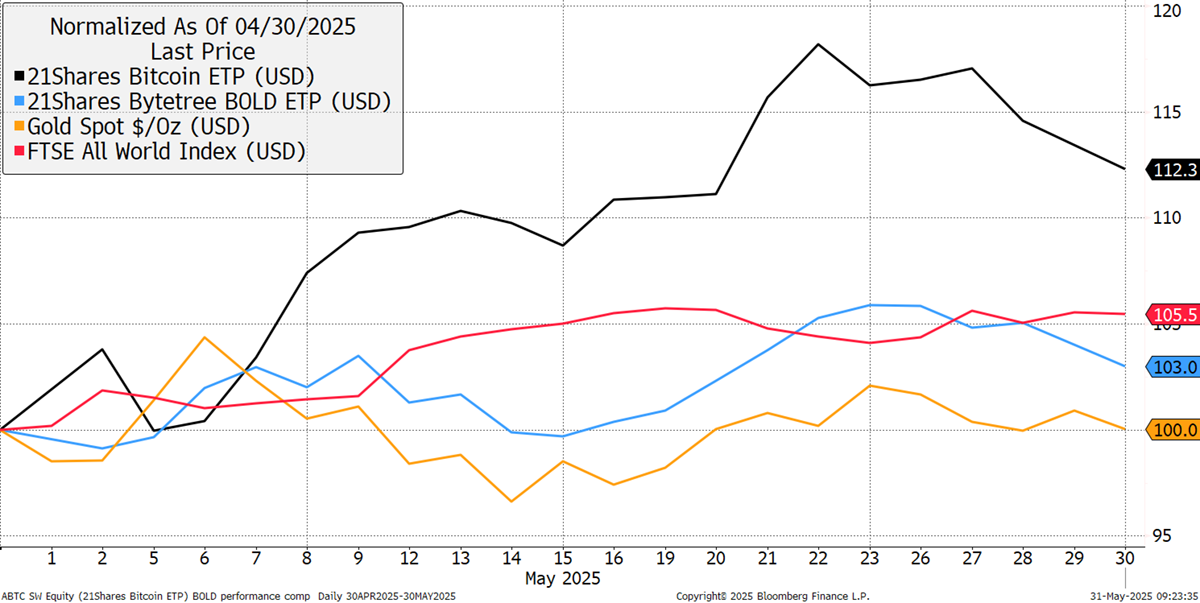

In May, BOLD rose by 3.0%, Bitcoin rose by 12.3%, and Gold was flat, while global equities rose by 5.5% in USD terms. The US dollar was down 0.1%.

Bitcoin, Gold, BOLD, and Equities in USD – May 2025

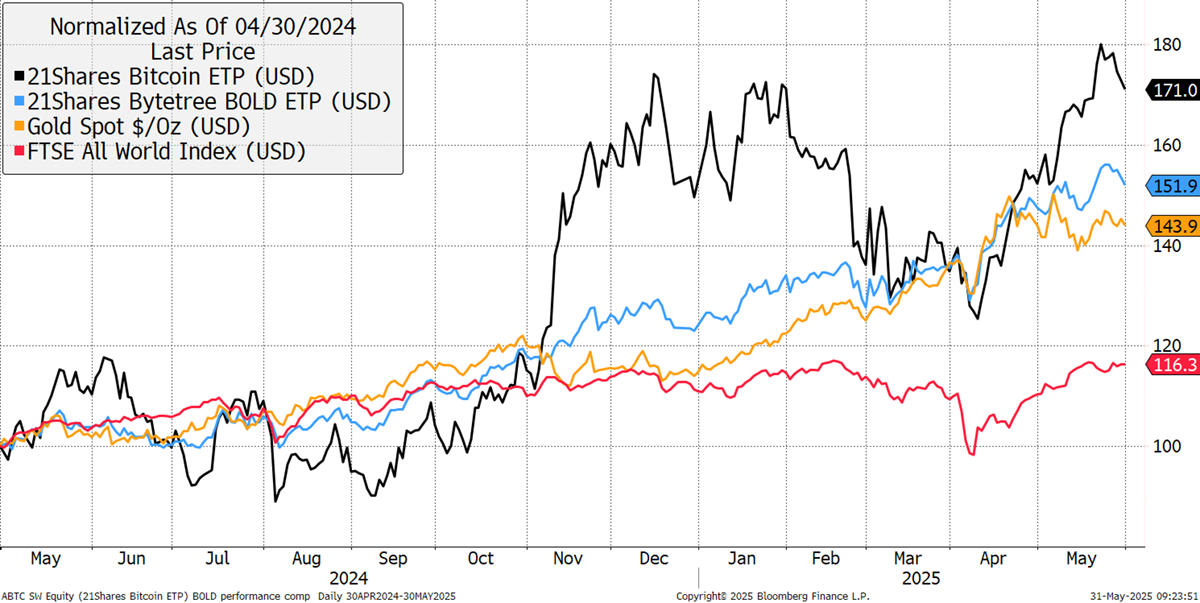

Over the past year, BOLD has returned 51.9%, while Bitcoin has returned +71%, in contrast to Gold with a +43.9% gain, while equities have risen by +16.3%. It is notable how Bitcoin and Gold have broken away from US equities.

Bitcoin, Gold, BOLD, and Equities - Past Year

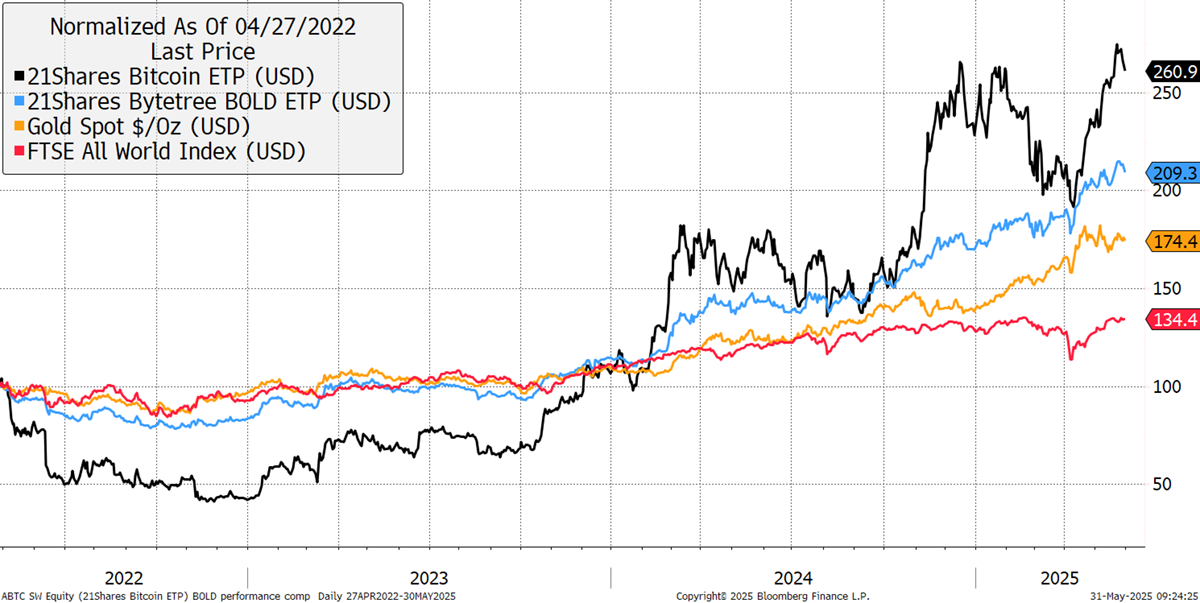

Since the 21Shares ByteTree BOLD ETP’s inception on 27th April 2022, BOLD has returned +103.3%, Bitcoin has returned +160.9%, Gold is up +74.4%, while equities have risen by +34.4%.

Bitcoin, Gold, BOLD, and Equities - Since Inception

US Treasury Crisis Drives Bitcoin and Gold

Government bond markets are in crisis. Debt levels are too high, and governments are being squeezed by the cost of servicing their debt. This has pushed bond yields higher as the market struggles to cope with the vast levels of new debt issuance.

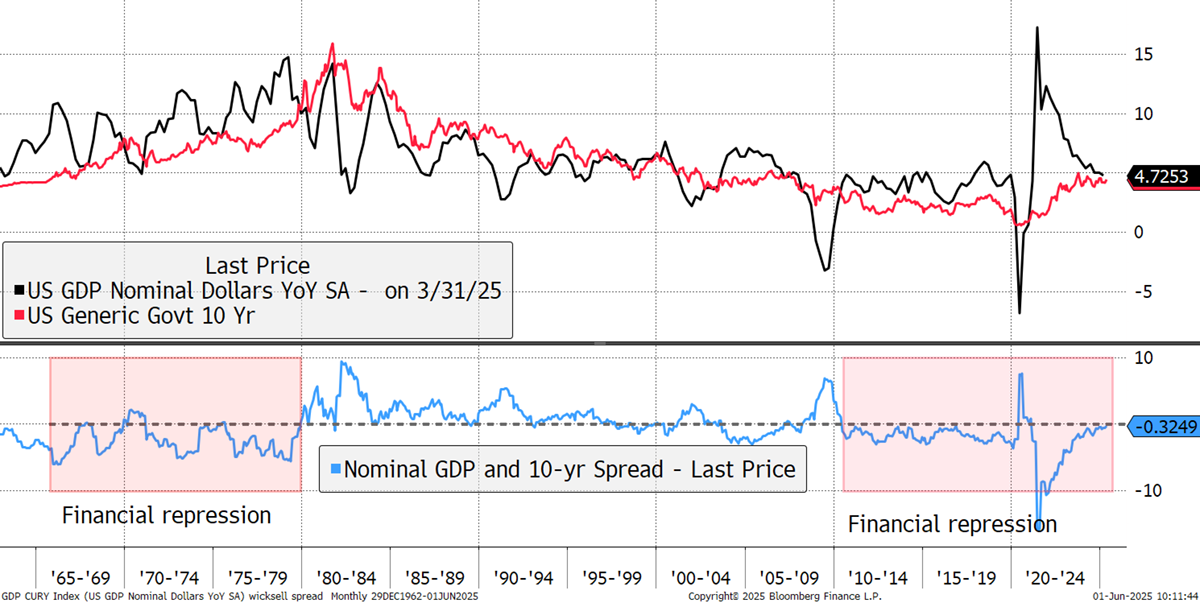

However, there is another explanation for the bond yield, and that comes from growth, or more specifically, nominal growth, the combination of real growth and inflation. This is known as the Wicksell Rule, where the nominal growth rate should roughly equal the 10-year yield. For the first time since the pandemic, and after huge financial disruption, this is once again true. The bond yield at 4.2% can also be explained by the level of nominal GDP growth.

The Wicksell Rule - US Treasuries and Nominal GDP Growth

Notice that in the 1970s, we were in an era of financial repression where the 10-year was below nominal GDP. This brought the debt burden from WWII down to low levels. That was repeated after the 2008 financial crisis but came to an end during the pandemic. The debt surged, along with inflation, which caused the service costs to escalate rapidly. The solution was to raise interest rates to maintain confidence in the bond market and fight inflation. The trouble is that to reduce government debt by inflation, the yield needs to fall, or the level of growth needs to rise.

The US administration is trying to boost the real growth part of nominal growth and contain inflation to try and restore financial repression. This is the only way to reduce the debt burden in the long term.

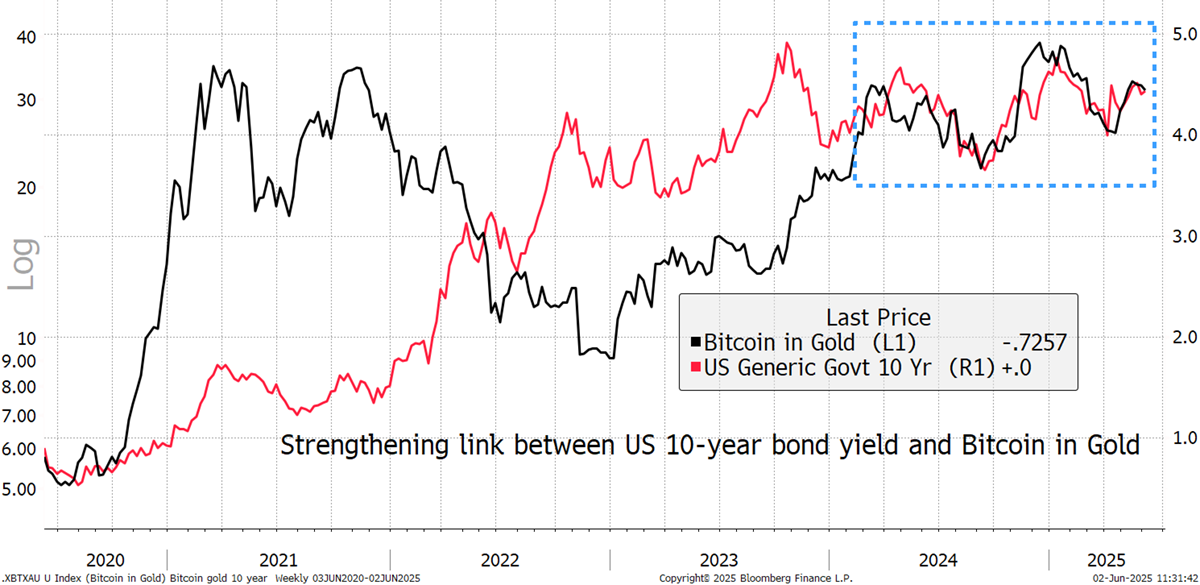

What is most interesting for Bitcoin and Gold watchers is how the 10-year yield is driving the price of Bitcoin vs Gold. This has always been true to an extent, as rising yields generally reflect growth, and falling yields a slowdown. Gold is risk-OFF and prefers falling yields. Bitcoin is risk-ON and prefers rising yields. The relationship has tightened considerably.

The Impact of Bond Yields on Bitcoin and Gold

Not only do we have ETF flow data (see below) to help understand the Bitcoin vs Gold relationship, but now we can confidently point towards the bond yield.

BOLD watchers don’t need to worry much about bond yields because it seems either Bitcoin or Gold is doing the heavy lifting at any time. We shouldn’t mind which, but it’s nice to know that the bond volatility works in BOLD’s favour.

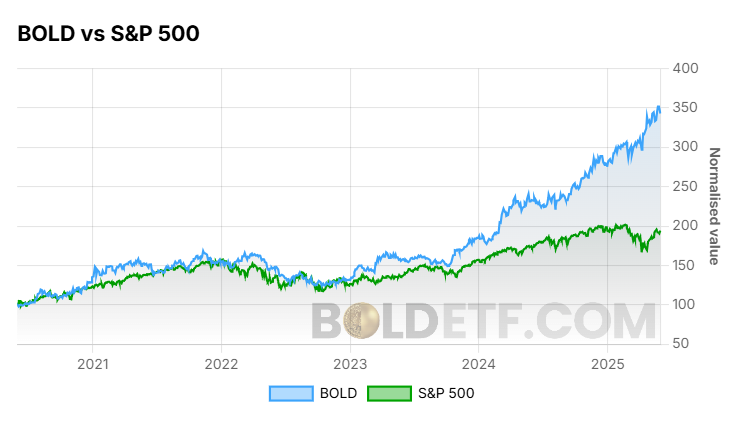

BOLD vs S&P 500

Monthly Rebalancing of the BOLD ETP

BOLD allocates to Bitcoin and Gold on a risk-adjusted basis using past volatility, which is calculated using daily price movements. The less volatile asset, which has lower daily price moves, gets a higher weight in the index at the end of the monthly rebalancing.