Stay Cautious

I hope you all had a relaxing Easter break. I can’t remember the last time I was so delighted that the UK market would be closed for four days.

Things have been moving quickly, and we find ourselves in a binary situation. There is either a monumental oil shock coming, or there isn’t. If there is, stockmarkets will likely suffer, as the economy tips into recession. If there isn’t, a swift recovery is possible, but I think that is unlikely as the world digests the damage done. It seems more likely that a sluggish market environment follows.

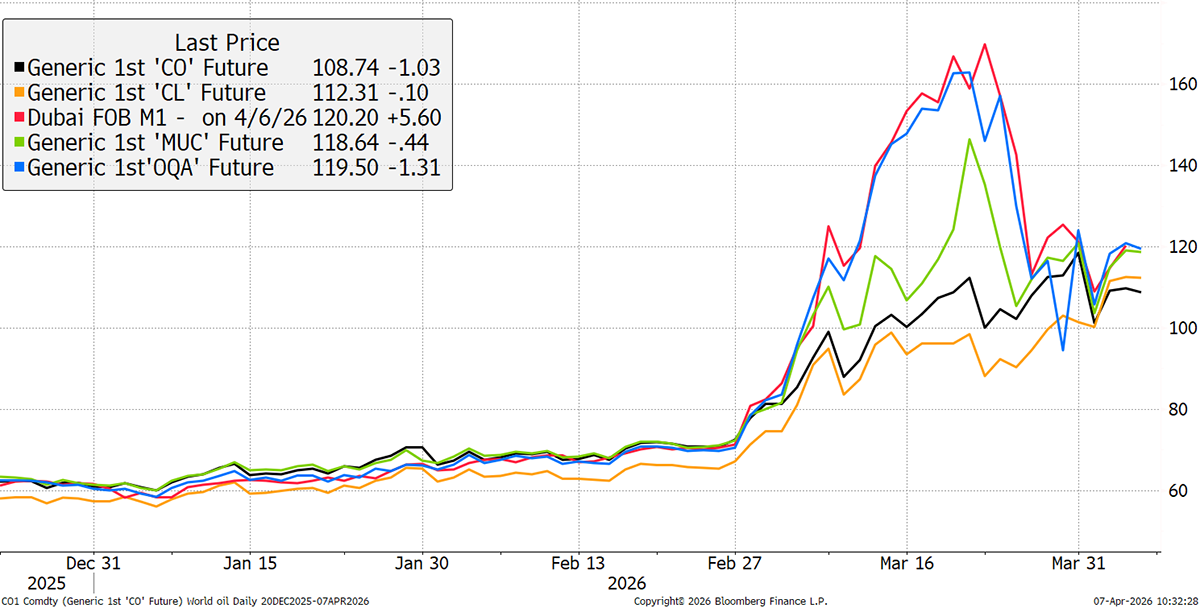

There have been some recent developments in oil. The first is that the different oil benchmarks in the Middle East, such as Dubai and Oman, have again converged with Brent (global price) and WTI (US price). Some of this price disruption is financial, whereby traders have anticipated better functioning markets in the future, but the other part is physical, as the local markets have cooperated and diverted to pipelines and other workarounds. The system is still under pressure, but the market is now functioning more effectively.

Oil Benchmarks Converge

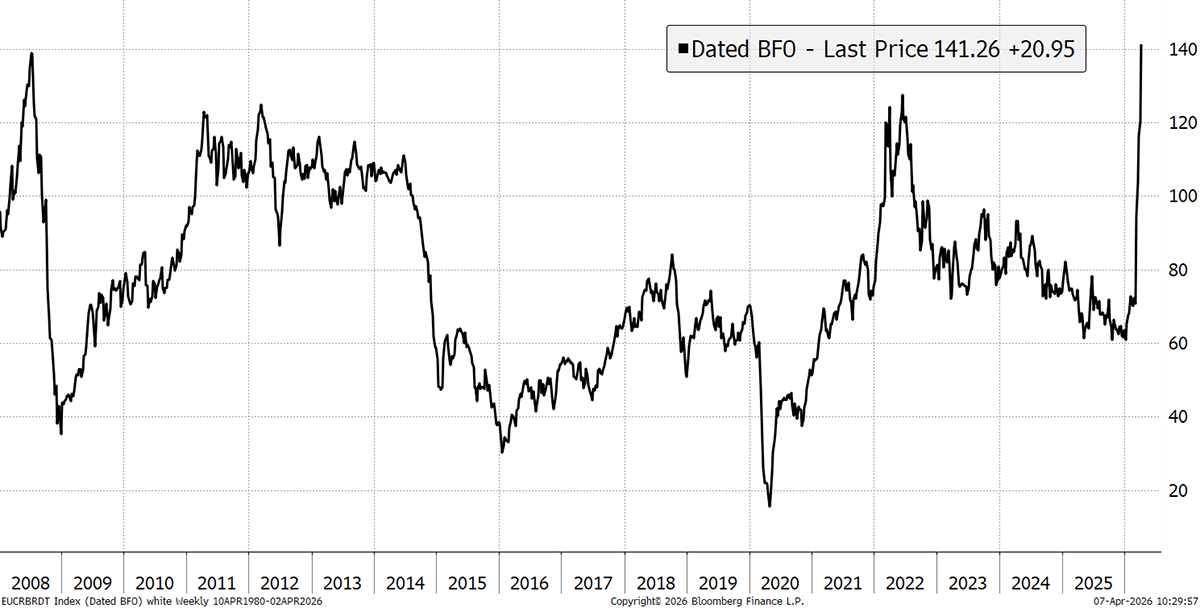

On the other hand, we see “Dated Brent” trading at all-time highs. This is a measure of the physical spot market rather than the financial futures market. That means it measures actual oil cargoes as opposed to cash-settled financial derivative transactions. Dated Brent is above the levels of the early war in Ukraine and the peak in 2008. There continues to be considerable stress in energy markets, which will not calm down until the Strait of Hormuz reopens.

Dated Brent

Jet fuel stocks are falling rapidly, and flight cancellations have begun. Air New Zealand, United, SAS, and Vietnam Airlines are among the many to announce cancellations. The last lockdown saw ultra-low oil prices as travel was curtailed; perhaps the next one is the exact opposite, but with the same effect.

From the Strait of Hormuz, it takes a tanker around 20 days to reach the Far East, 20 to 30 days to reach Europe, and 35 to 50 days to reach the USA. The physical shortages are only just starting to kick in, and even if the situation is resolved and the Strait is reopened, there will still be a lag before things return to normal.

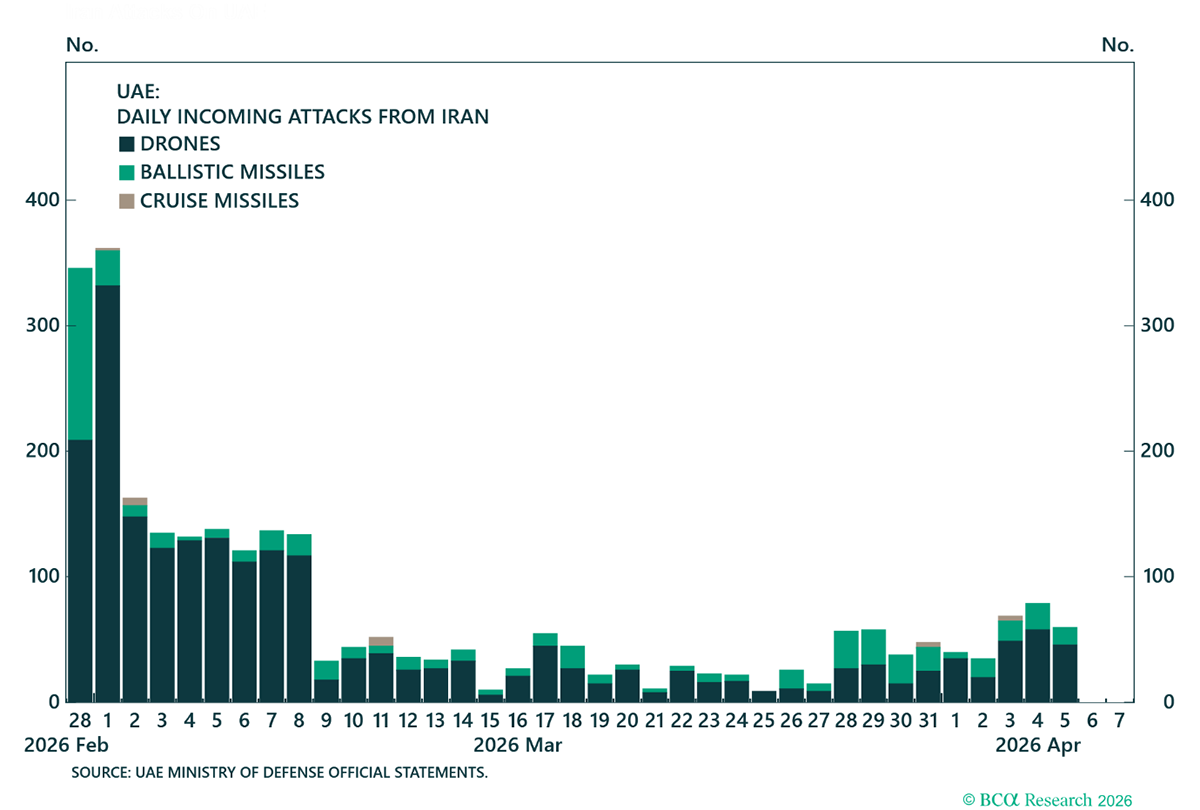

Financial markets are supposed to be efficient in measuring these things. But I have had my doubts ever since the failure of Lehman Brothers, when the markets assumed that all would be well right up to the moment of bankruptcy. I sense that the markets are pricing in victory, yet there are no signs that Iran has been neutralised. These drones and missiles are causing huge damage, some of which will take years to fix.

Iran Attacks on the UAE

Naturally, a regional war or disruption will not impact global corporate profits over the long term, but it may have a significant impact over the short term. We have seen bond yields rise in March, which scared markets because that directly impacts profitability and, more importantly, the discount rate. When rates rise, the fair value of a long-term investment falls. That can have a long-term impact on market returns.

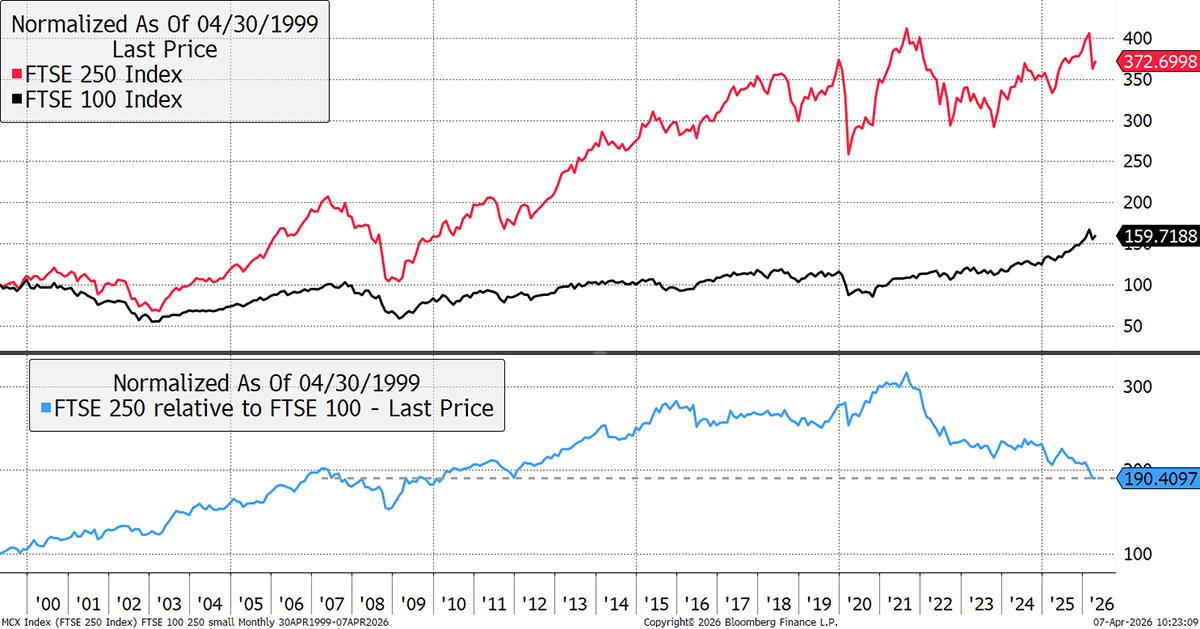

We all know that the FTSE 100 is an index that is laden with natural resources and banks. That makes it well placed for the current environment. It is interesting that the FTSE 250, the UK mid-cap index, is in a much harsher place. Since the summer of 2021, the FTSE 250 is down by 10% while the FTSE 100 is up by 46%. This is a huge lag, which began when rates started to rise.

FTSE 100 vs FTSE 250

The FTSE 250 represents the domestic UK economy, without much exposure to banks and resources. It is the home to REITs, Retailers, and Housebuilders. It is not going well, warning us that higher rates and an energy shock will hurt.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd