Navigating Crypto: ByteTree’s Guide to 18,000+ Cryptocurrencies

When most people talk about crypto, they're really just talking about two: Bitcoin and Ethereum, and maybe a handful of others. But the crypto industry is a vast universe of more than 18,000 tokens across hundreds of categories.

Even after you strip out the dead, the dormant, and the obvious scams, you're left with roughly a thousand tokens that are doing something economically meaningful; each with its own design, value proposition, and risk profile. Lumping them all together as "crypto" is a bit like lumping every stock on the Nasdaq under "tech." It hides everything that actually matters when you're trying to decide what tokens to own.

This Token Takeaway will walk you through the different token categories and explain what tokenomics is and why it's the single most important aspect to understand before you enter the market. We will also run through some of the core valuation metrics used by industry professionals, including some that we use for ByteFolio, our crypto model portfolio.

Introduction: The Shape of the Market

To set the stage with current numbers, the total crypto market capitalisation sits at around $2.6tn, spread across more than 18,000 tokens tracked by CoinGecko. Bitcoin alone accounts for about 58% of the total market, with a market cap of roughly $1.5tn, while Ethereum is a distant second at around 10%, sitting at about $280bn. Stablecoins make up another 10.8%, totalling around $288bn. In essence, that means Bitcoin and Ethereum collectively account for nearly 70% of the entire market cap, with the remainder split across the other 18,000 tokens.

What Makes a Cryptocurrency?

Before we get into categories, we need to define what makes a cryptocurrency. In a nutshell, a cryptocurrency is a digital asset secured by cryptography that lives on a ledger, but that is where the common thread ends.

Decentralised, public crypto, i.e. the original design embodied by Bitcoin and Ethereum, runs on a ledger that no single entity controls: the supply is set by code, transactions are validated by a distributed network, and no bank, government, or company can unilaterally mint, freeze, or seize tokens.

This universe has since broadened to include centralised crypto assets, where an issuer retains meaningful control. Stablecoins like USDT and USDC sit here, as do tokenised real-world assets. The latter are issued by entities like BlackRock, where the issuer controls minting, redemption, and (in some cases) blacklisting.

Bitcoin is the archetype. It has its own blockchain, its own consensus mechanism (proof-of-work), and its supply is capped at 21 million by code. BTC, the token, is also the fuel for Bitcoin transactions, where every transfer pays a fee in BTC to the miners securing the network. No one can change the supply schedule or rules without network consensus.

Ethereum extends that model. While it has its own blockchain too, its native token, ETH, pulls double duty as a store of value and fuel. You don’t just spend ETH for peer-to-peer transactions but also to execute smart contracts on the network. That second function is what unlocked everything that came after: DeFi, NFTs, stablecoins, and the entire altcoin universe.

The distinction between a chain's native token and the thousands of tokens built on top of a chain brings us to categorisation.

Token Categories

Why categorise at all? There are two reasons. First, different categories of tokens derive their value from completely different sources. A stablecoin's value comes from a peg, a Layer-1 token's value comes from network demand for blockspace, and a perpetual decentralised exchange (perp DEX) token's value comes from trading fees. Treating them as the same asset class is a quick way to lose money.

Second, categories rotate. Capital in the crypto universe flows in narratives. AI and meme tokens were red-hot in 2024, Real-World Assets caught a bid through 2025, and perp DEX tokens have been the breakout story over the last eight months. If you don't know which bucket a token sits in, you can't read the rotation.

In this next section, we have listed the 10 largest and most relevant categories by market cap. We'll also address the overlap between them at the end.

1. Layer-1s & Smart Contract Platforms

Layer-1s, or L1s, are the base-layer blockchains, with examples like Bitcoin (BTC), Ethereum (ETH), Solana (SOL), BNB Chain (BNB), and Avalanche (AVAX). The native tokens are used to pay transaction fees, secure the network through staking or mining, and (in the case of programmable chains) act as the unit of account for everything built on top. This is by far the largest category by market cap.

2. Layer-2s & Scaling Solutions

Layer-2s, or L2s, are networks that run on top of an L1. While they inherit the L1’s security layer, their core purpose is to improve transaction speed and optimise costs. Examples here include Arbitrum (ARB), Optimism (OP), Polygon (POL), and Base (no token yet). Their native tokens typically govern the platform and, in some designs, accrue a share of sequencer revenue.

3. Stablecoins

Stablecoins are tokens designed to maintain a fixed value, typically pegged to the US dollar. Examples include Tether (USDT), USD Coin (USDC), USDS, and EURC, with the latter being pegged to the EURO rather than the USD. Stablecoins are the rails for trading and on-chain payments, and this market alone is around $300bn.

While stablecoins are viewed as digital cash, it is also worth flagging that they come in flavours: fiat-backed (USDT, USDC, EURC), crypto-backed (USDS), gold-backed (PAXG), and algorithmic (mostly graveyard but think Terra’s UST). Notably, they have also become a meaningful holder of US Treasuries.

4. Liquid Staking & Restaking Tokens

Liquid staking and restaking tokens refer to the receipts you get when you stake your ETH (or SOL, etc.) and want to keep using it on-chain. Examples include Lido's stETH and Rocket Pool's rETH. The token represents your staked position plus accrued yield and, most importantly, it's tradable. Restaking extends the idea by letting that same staked ETH secure additional protocols for additional yield.

5. DeFi (DEXs & Lending)

DeFi is the original altcoin category, covering protocols for swapping, lending, and borrowing without a counterparty. Examples include Uniswap (UNI), Aave (AAVE), Sky (SKY), and Curve (CRV). Token holders typically govern the protocol and, in some cases, receive a cut of the fees.

6. Perpetual DEX Tokens

These tokens are decentralised exchanges for perpetual futures, which is also the highest-fee-generating sector of crypto right now. Examples include Hyperliquid (HYPE), EdgeX, and Aster. Hyperliquid alone has reported annualised revenue north of $700m, making it one of the standout performers of the past year. Many of these tokens have direct buyback or fee-share mechanics, so the value accrual is unusually clean.

7. Real-World Asset (RWA) Protocol Tokens

Two different things are typically referred to as Real-World Assets (RWA) in the same breath, but the distinction matters. The actual RWA tokens are on-chain representations of off-chain assets. These are yield-bearing dollar tokens like Ondo's USDY, BlackRock's tokenised Treasury fund BUIDL, or tokenised private credit and real estate. They earn yield from the underlying asset itself.

By contrast, RWA protocol tokens are the governance tokens of the platforms that issue and manage those assets. These include Ondo (ONDO), Maple Finance (SYRUP), and Centrifuge (CFG). Holding ONDO doesn't earn you a treasury yield, while holding USDY does. The protocol tokens accrue value from fees, governance rights, and/or (in some cases) a share of the platform's fees.

8. AI Tokens

AI tokens are a loose category for projects that combine crypto with AI infrastructure, model marketplaces, or compute networks. Examples include Bittensor (TAO), Render (RENDER), and ASI Alliance (FET), previously Fetch.ai.

9. Memecoins

Memecoins are tokens whose value is derived primarily from cultural attention rather than cash flows or technical innovation. Examples include Dogecoin (DOGE), Shiba Inu (SHIB), and Pepe (PEPE). In terms of their tokenomics, they're usually very simple: fixed supply, no revenue, no governance.

Memecoins were all the hype in 2024, particularly benefiting protocols like Solana, but the sector has evolved significantly since then. Whatever your view on them, they still account for tens of billions in market cap, and remain a non-trivial segway for how retail flow enters the market.

10. Privacy Tokens

A privacy token’s core purpose is to obscure transaction details on-chain. While the open public ledger is a design choice for Bitcoin and Ethereum, privacy tokens exist for those who prefer to keep their transactional activities private. Examples include Monero (XMR) and Zcash (ZEC).

While last on our list, it is one of the earliest spin-off sectors in the crypto industry, with Bytecoin being the first in 2012. It’s a small but persistent category, increasingly squeezed by exchange delistings and regulatory pressure.

The Overlap Problem

In addition to the 10 defined categories, there is overlap between categories and with governance and utility tokens. Except for stablecoins, almost every token mentioned so far is also a governance token. Additionally, most tokens can be placed into broader ecosystems that span multiple categories.

ETH is an L1, a store of value, the gas token for every L2, and a yield-bearing asset via staking. HYPE is a perp DEX token, its own L1 token, and a governance token. ONDO is an RWA protocol token, a governance token, and an ecosystem token.

Governance Tokens

"Governance" and "ecosystem" are useful descriptors of what a token does, but since most tokens belong in this club, it’s not useful as a category. Most tokens wear several hats; the question worth asking is which hats matter most for value.

Utility Tokens

“Utility token" gets used a lot, but the nutshell definition is a token that has a required, non-speculative function inside its protocol. ETH is a utility token because you must pay gas in ETH to do anything on Ethereum. SOL is also a utility token because you need it to transact on Solana.

The reason the distinction between governance and utility tokens matters is the demand story. Tokens with genuine utility have a structural source of demand that doesn't depend on belief. Tokens without it are mainly governance and speculation plays, and they tend to underperform when sentiment turns.

Tokenomics

Tokenomics is the economic design of a token: how it's issued, how it's distributed, what it's used for, and what mechanisms (if any) cause its value to accrue to holders. There are four factors that matter, and in this next section, we will go through them in turn.

1. Supply Mechanics

In terms of supply mechanics, there are three numbers to internalise for any token:

- Circulating supply: what's in the market right now.

- Total supply: what's been issued, including locked and unvested tokens.

- Max supply: the hard ceiling, if there is one.

Bitcoin has a fixed max of 21 million BTC, and that scarcity is a key feature. On the other hand, Ethereum has no max supply, but ETH has been net-deflationary at times due to fee burning (EIP-1559). Solana has an uncapped supply but with declining inflation.

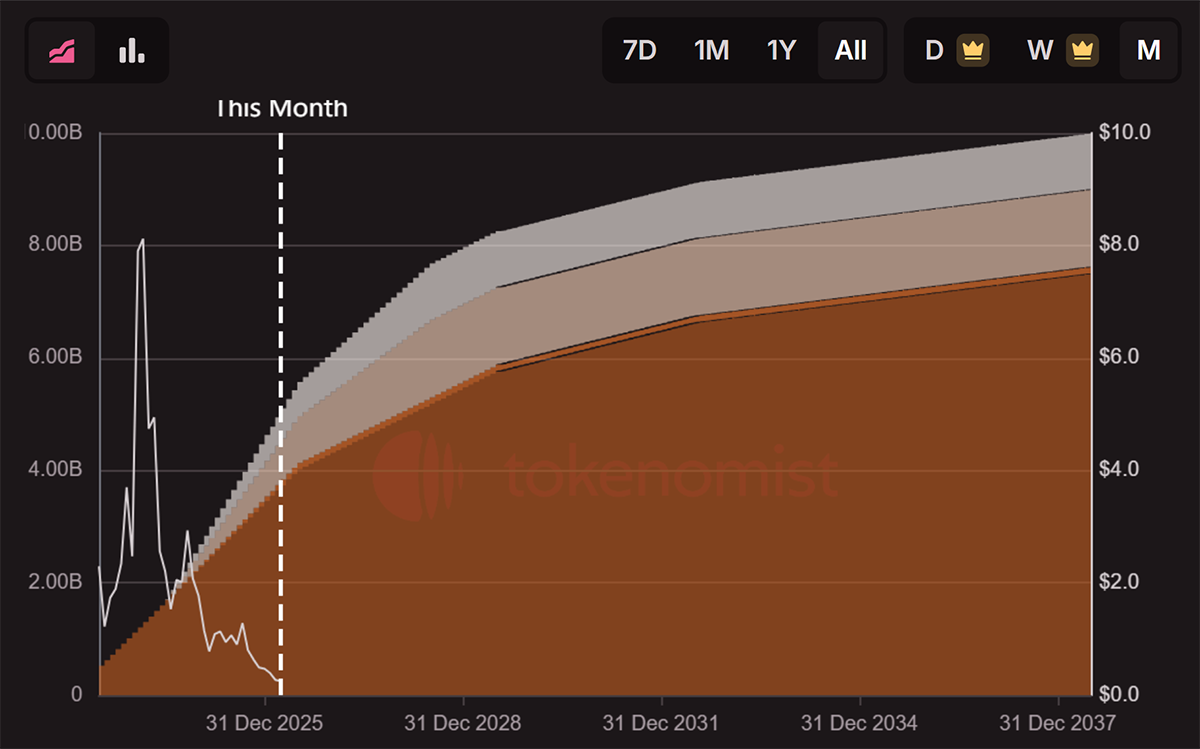

Many tokens have aggressive emission schedules, with the circulating supply doubling or tripling within a few years. Worldcoin (WLD), for instance, launched with around 522 million tokens in circulation in July 2023, and by December of that same year, the supply had nearly doubled to 1 billion. The current circulating supply is still just 3.3 billion out of a 10 billion max cap, meaning roughly two-thirds of all WLD has yet to enter the market.

WLD Release Schedule

2. Inflation, Deflation, and Unlock Schedules

Inflation in crypto comes from two sources: ongoing emissions (block rewards, staking rewards) and unlocks (team, investor, and treasury allocations that vest into circulation).

Emission schedules are typically known in advance, but that doesn't mean they're necessarily priced in. Markets often underprice the steady drag of high emissions until the damage is done, and unlocks are even worse. A token with 15% circulating supply and a four-year cliff vesting curve will face years of structural sell pressure regardless of how good the protocol is. This is one of the most underrated reasons "fundamentally good" tokens chop sideways for years; the supply just keeps coming.

Deflationary mechanisms work the opposite way. These include token burns from fees (ETH), buyback-and-burn programs (HYPE), or supply caps (BTC). Consequently, the deflationary mechanism creates structural demand or shrinks the float.

3. Value Accrual

Value accrual is the mechanism by which protocol revenue reaches token holders, i.e., how they capture value. In practice, it comes down to two approaches.

The first is a staking yield on Proof-of-Stake chains. This is where you lock up the native token to help secure the network, and in return, you’ll earn a combination of issuance plus a share of transaction fees. Ethereum, Solana, and most other L1s work this way.

The second is a buyback-and-burn or buyback-and-distribute program. This refers to how the protocol uses its fee revenue to buy tokens on the open market, either burning them (shrinking supply) or distributing them to stakers (paying you directly). Hyperliquid is the cleanest current example.

4. Utility and Demand Drivers

Beyond value accrual, the question is: why should you hold or use the token? Is it required for gas, as it is for ETH, SOL, and BNB? Is it required for staking to secure the network, as is the case for most L1s? Does it grant access to something you can't get otherwise, like a license, a ticket, or a service? Or is it just speculation?

Naturally, tokens stack better when they have multiple, independent demand drivers. For example, ETH has gas, staking, DeFi collateral, and store-of-value demand, all compounding together. This is why it survives narrative droughts that kill single-purpose tokens.

Crypto Valuation Metrics

Once you've got a handle on what a token does and how its tokenomics work, the next question is valuation. Is it cheap or expensive relative to comparable tokens? Is this a good entry point?

In the following table, we list some of the valuation metrics we use when evaluating a token for ByteFolio. Regular ByteFolio readers will undoubtedly be familiar with most of them.

| Metric | Formula | What It Measures | Best Used For |

| FDV / TVL | Fully Diluted Valuation ÷ Total Value Locked | How much the market values a protocol per dollar of capital deposited. | DeFi protocols |

| FDV / Revenue | Fully Diluted Valuation ÷ Annualised Protocol Revenue | A crypto-native version of price-to-sales. | Any protocol that generates fees |

| Real Reward Rate | Staking Yield − Token Inflation Rate | Are stakers earning or being diluted by emissions? | L1s |

| OI / FDV | Open Interest ÷ Fully Diluted Valuation | Protocol liquidity relative to the size of the native asset. | Perp DEXs |

| ADV / OI | Average Daily Volume ÷ Open Interest | Trading activity relative to outstanding contracts; a turnover measure. | Perp DEXs |

These metrics allow us to compare a $500m-FDV perp DEX with a $5bn-FDV perp DEX on equal footing. For example, the FDV/Revenue multiple, i.e. crypto price-to-sales, helps determine which token is doing more business per dollar of valuation. For the price side of the equation, ByteTrend.io provides a trend-based scoring system that complements these valuation multiples.

ByteTrend is a unique, powerful trend-following system developed by ByteTree. Built on common technical indicators used by finance professionals, it identifies leading, neutral, and lagging trends in financial markets. This means that you can screen the trends for hundreds of crypto tokens on a single platform, giving you a great starting point for your next investment opportunity.

Behind the scenes, we are currently building ByteTrend 2.0, which will introduce new tools and refine existing ones. Stay tuned for more information over the coming months.

Conclusion

Crypto is messy by design: 18,000 tokens, 100s of overlapping categories, and a market that rotates narratives every few months. While the industry has gained some key entities that help make sense of the noise, like CoinMarketCap, CoinGecko and, of course, ByteTree, the infrastructure is still small compared to TradFi. The temptation may be to retreat to BTC and ETH or chase whatever is pumping, but you’d be missing out.

The crypto framework isn’t that complicated, and if you come from a TradFi background, the concepts are similar or the same, just with a different name. Start by determining which category a token belongs to and, since most tokens wear several hats, identify the additional categories it overlaps with. Then, evaluate its tokenomics, including supply, distribution, unlocks, value accrual, and demand drivers. Once you've done the groundwork, you can compare the token to peers using the right multiples.

Consistency pays off and already puts you ahead of most market participants. But, as Charlie Munger once said, “It’s simple, but not easy”. In practice, it can be complicated, time-consuming work, and easy to get wrong. If that sounds like something you’d rather avoid, then you are in the right place. This is exactly where ByteTree’s services excel, and we are thrilled to have you here.

Go beyond the framework.

If this guide is the map, ByteTree Digital is the navigation system.

Our ByteFolio model portfolio shows how we apply these principles in practice, while Token Takeaway breaks down the tokens, sectors, and narratives that matter most.

No noise. No narratives for the sake of it. Just disciplined positioning in a fast-moving market.

Get direct access and put the framework to work.