ByteTree Quarterly Investor Letter - Q1 2026

Since 2013, our mission has been to help people invest more effectively. We do this by delivering actionable, high-quality, contemporary investment guidance at an affordable price.

With all the information out there, we help investors by distilling our advice into model portfolios, thoroughly explaining the reasoning behind every new investment recommendation. In this Q1 2026 update, I shall review our core product, The Multi-Asset Investor.

Letter from Charlie Morris, CEO

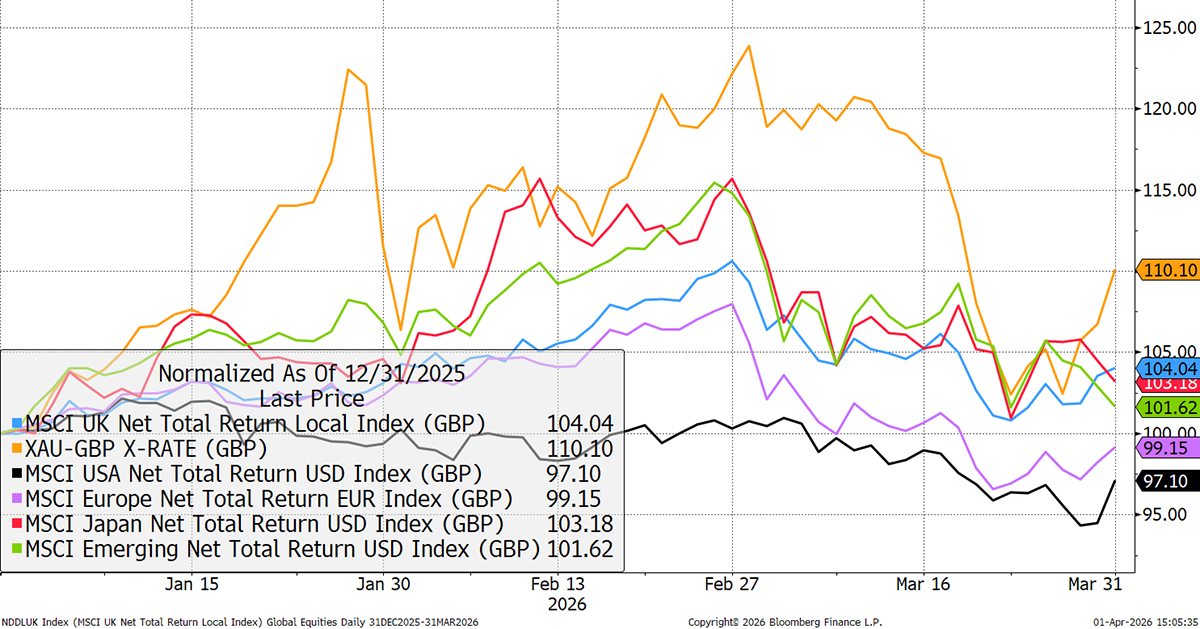

Things were going well in January, especially for non-US equities, right up until the moment the first missile was fired. At that point, markets sold off sharply, with gold bearing the brunt.

Global Equities and Gold in 2026

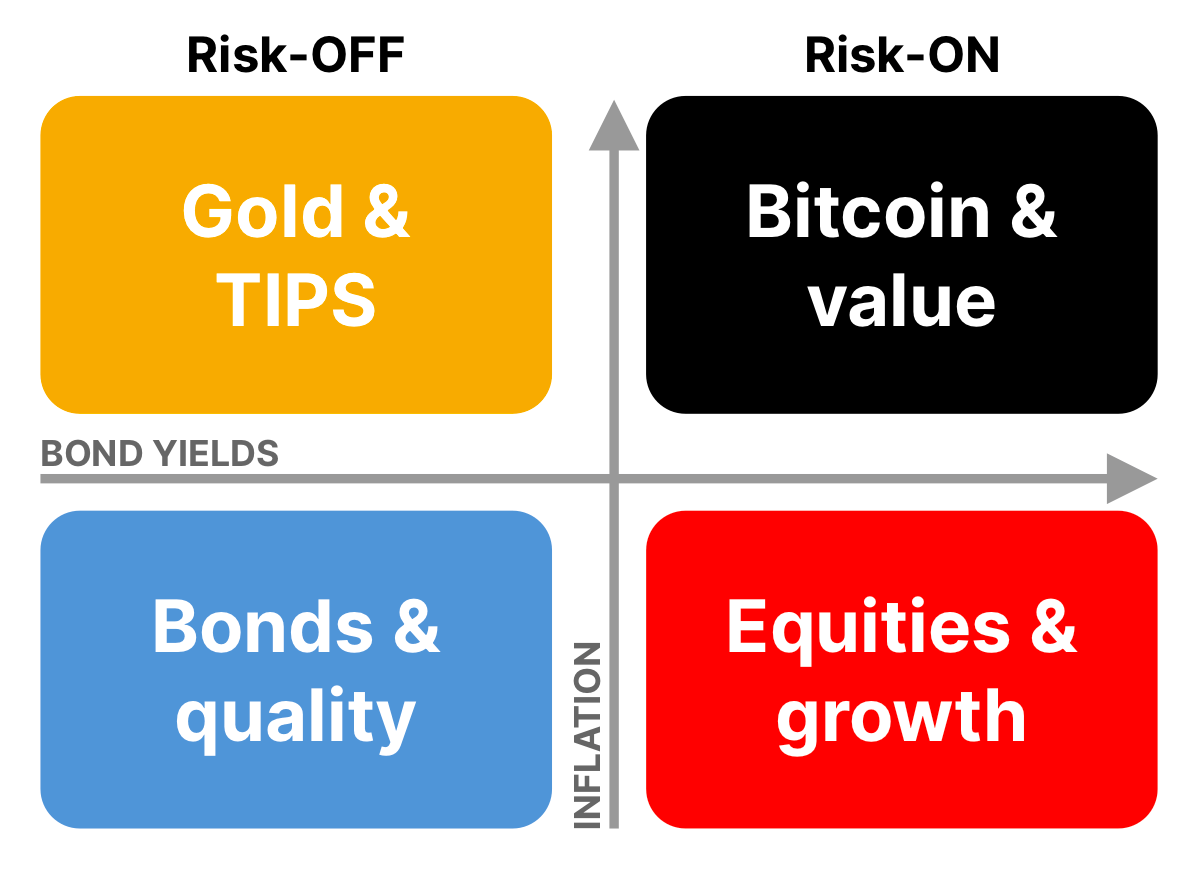

The oil shock changed everything. The markets had been looking forward to cooling inflation and the rate cuts that would follow. Bond yields surged alongside the oil price, causing an abrupt shift in the prevailing market dynamics. With reference to the ByteTree Money Map, the market turned from blue to black in a heartbeat.

The ByteTree Money Map

My reaction was to reduce risk in the face of the unknown. As I wrote in What Happened in 1974?, oil shocks can trigger major bear markets, just as they did in 1974, 1981, and 2008.

As we entered this crisis, the Soda Portfolio had volatility of around 7%, which was 1% above its benchmark, the FTSE Private Balanced Index, and mainly as a result of holding gold. Following equity risk reduction and introducing further diversification, it is back in line with the market at 9%, as overall price volatility has risen.

This Whisky Portfolio is the satellite strategy designed to accompany a core holding in the Soda Portfolio. Whisky’s volatility was 12% in February, which was slightly above its benchmark, the FTSE 100, at 10%. Today, it is 8%, while the FTSE 100 has surged to 19% since hostilities began.

This is simply about capital preservation during a period of increased risk. As I wrote in the report linked above, the 1970s saw equities slump alongside bonds. Yet I also highlighted that an equivalent oil price today would be above $150 or $200, and that hasn’t happened. Indeed, on Tuesday, Trump’s recent announcement caused the oil price to fall back, triggering a rally in equities. Then his following announcement largely reversed it. What to believe?

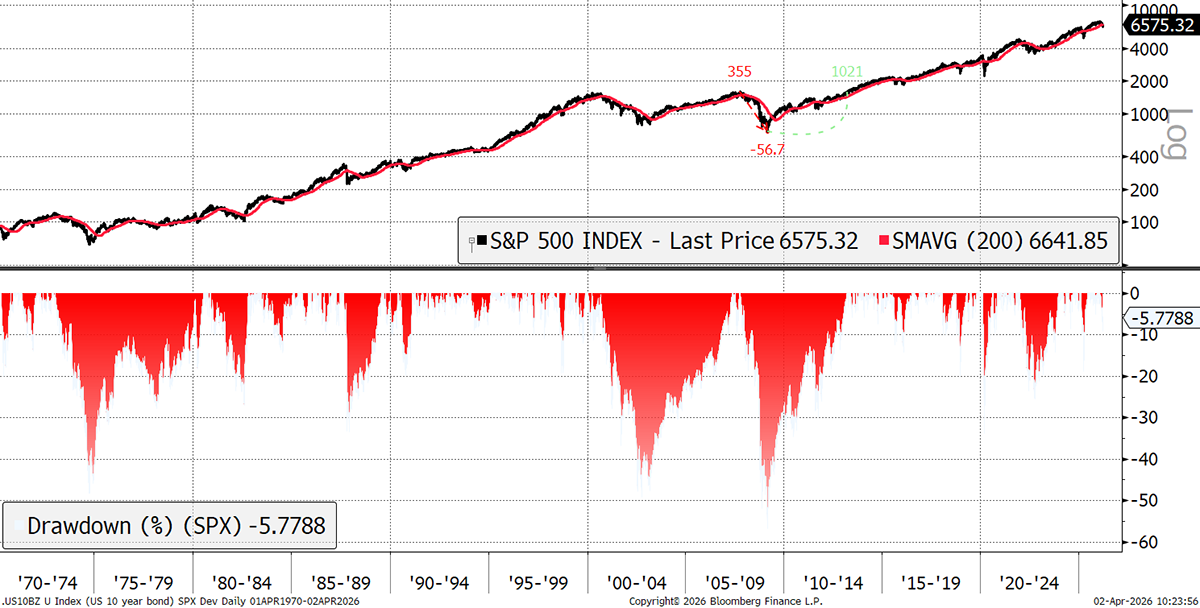

It is never comfortable when the stockmarket is trading below its 200-day moving average. When it does, volatility rises, and the risk of sharp losses increases. In recent years, these have been short-lived or even false alarms. However, against that, we know that US equities are richly valued, and sooner or later, a sharp drop becomes inevitable.

S&P 500 with Historical Maximum Drawdowns

There’s something about the post-2008 world, where market corrections have shortened. Many believe the “plunge protection team” (PPT) will step in and either print more money, cut interest rates, or deliver a fresh narrative. I think it’s somewhat true, even though no one has ever identified who the PPT actually are, or whether they actually exist.

These days, markets are awash with derivatives. Recent volatility has prompted traders to hedge their positions, which, in the short term, supports the market. However, these will eventually expire, and that’s when things can turn nasty. The risk is that the PPT runs out of ideas, and the backstop that we have become used to isn’t there.

The correction in equity markets has been relatively modest given the scale of events. The safe haven has been energy stocks, while almost all other sectors have fallen. Those hit the worst have been housebuilders, industrials, consumer stocks, and REITs. Bond yields have risen, and the rally in the US dollar has been slight. In a world with few havens, the best way forward is to reduce risk and diversify.

I intend to have a cautious stance on market exposure until it is clear that the war is over and the green shoots of economic recovery are within sight. Trump has declared victory of sorts several times, yet Iran denies it. There can be no doubt that Iran’s military is severely depleted, but the Straits of Hormuz remain shut, and the Yemen Houthis are attacking Israel and threatening to blockade the Red Sea. On top of that, Ukraine is stepping up attacks on Russian oil exports. In Trump’s latest announcement, he said he would return Iran to the Stone Age and leave the Strait of Hormuz to the allies to sort out for themselves. The world has changed, and I cannot see a path where commodity prices are not much higher over the coming months and years.

Commodity exposure, particularly energy and agriculture, is important because it is the most effective and immediate way to offset short-term inflationary risks. Over the medium term, no doubt Bitcoin, gold, commodity stocks, and other hard assets will do even better, but that is unlikely to show itself until the market turns up again. That is the primary reason I have embraced broader commodity exposure beyond precious metals and mining stocks.

Away from the warzones, there’s pressure on the jobs market, not just from broader economic conditions but also from job cuts driven by AI efficiencies. This is one reason why the authorities will double down and are more likely to cut rates to ease the burden on consumers, rather than fight inflation, on the presumption that the oil shock is transitory. But is it?

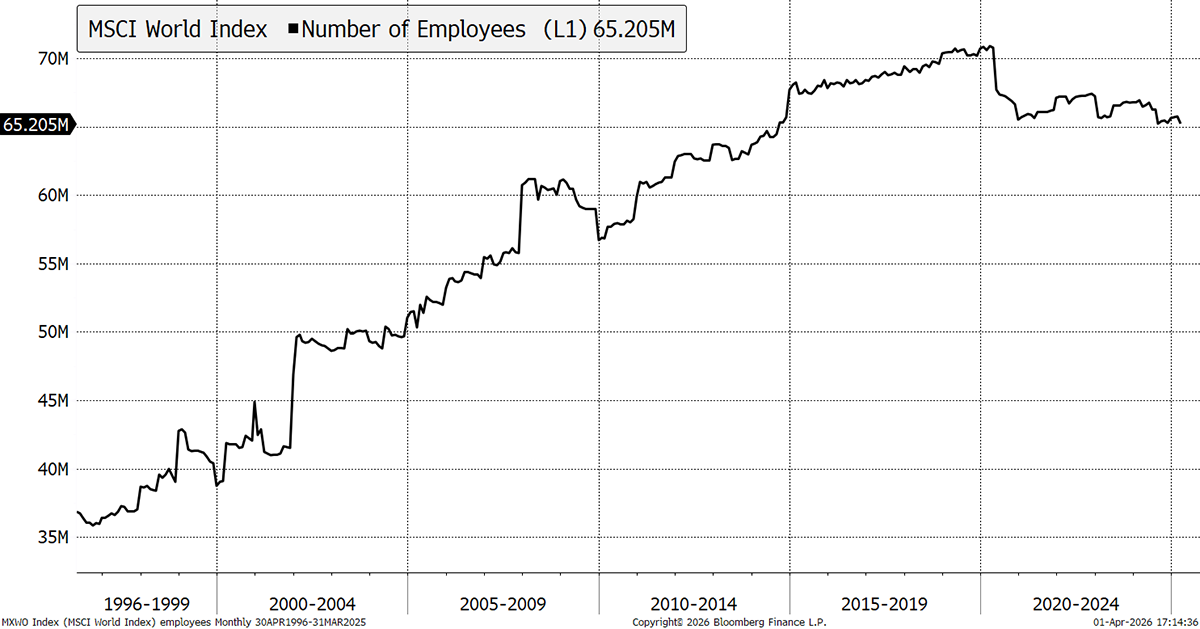

The AI impact on employment cannot be underestimated. This data is somewhat lumpy but shows an interesting trend. According to Bloomberg data, the 1,316 companies that make up the MSCI World Index employed 70 million people in 2019, which has now dropped to 65 million. Meanwhile, the value of the World Index is 85% higher than it was back then, which demonstrates how rising stockmarkets and corporate profits don’t create jobs like they used to.

Total Employees at Major Global Public Companies

There are also signs of stress in private credit markets, a shadow bank asset class that has ballooned in recent years. Some private credit funds have closed their doors, and we don’t know the scale of the problem because these markets are private and lack disclosure. No doubt the damage could be contained in a stable environment, but if a recession comes, then things can escalate.

With so much uncertainty, I believe it is right to prioritise capital preservation over gains. That is not to say we shut up shop, but rather that we maintain lower exposure to risky assets and a wider degree of diversification than normal.

The Multi-Asset Investor

The Multi-Asset Investor is a commentary and two portfolios, Whisky and Soda, that cover traditional assets. The portfolios are designed to be easy to replicate for investors managing their own money. Soda is low turnover and medium risk. Whisky is more dynamic and medium-high risk. It is written by Charlie Morris and updated weekly, with additional Flash Notes when immediate action is required.

The Whisky Portfolio

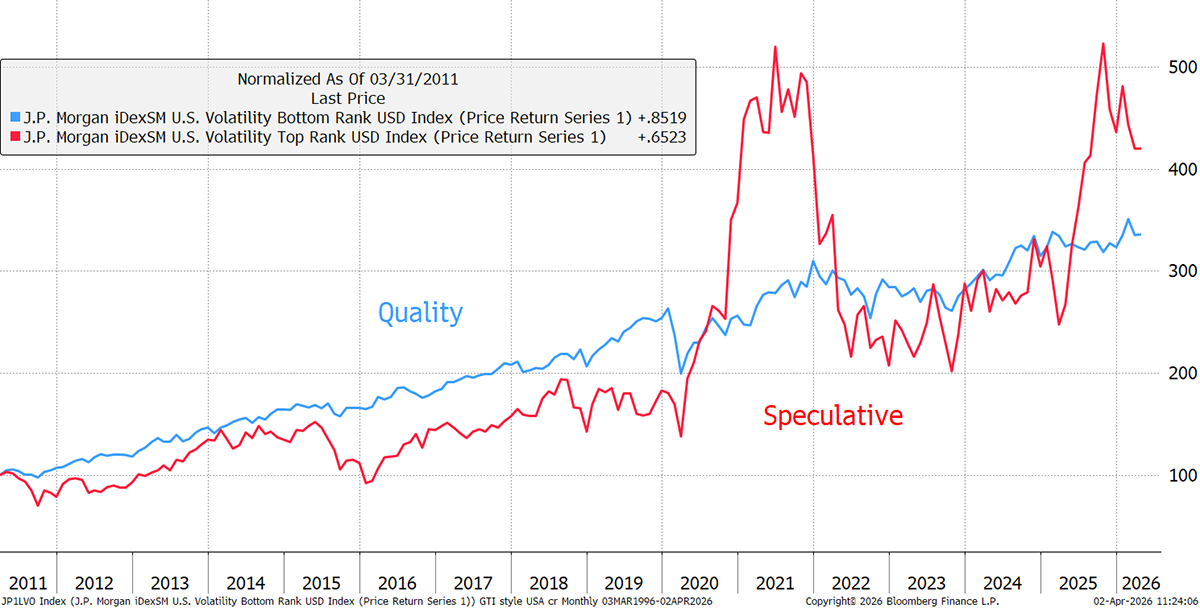

In late 2025, the Whisky Portfolio was heavily exposed to precious metals, and this was reduced later in the year. A major shift was toward attractively priced, high-quality stocks that would prove resilient during a slowdown and a lower-interest-rate environment. This hasn’t worked out particularly well so far, but the thesis remains unchanged. Quality stocks have generally been stable as they are globally diversified, stable businesses, yet Diageo and Unilever have disappointed.

Diageo’s woes are not so much down to reduced alcohol consumption, which has been exaggerated, but due to premiumisation. They are effectively a luxury goods company, and that sector has been dragged down as consumer spending shifts from the high end and, most importantly, as the marginal buyer tightens their belt.

Unilever is in deal-making mode, and the market doesn’t like it, at a time when it would prefer stability. March performance has been dire, but the stock appears to be severely undervalued. I stand by quality stocks as a good place to remain invested in this period of uncertainty.

Quality versus Speculative Stocks

In March, I reduced equity exposure to a more comfortable level, having been fully invested in February. It is always difficult to know what to sell, but REITs were the easier decision, as bond yields rose. No doubt there is long-term value in property, but now is not the time to explore.

Other stocks were also sold, with best intent, to get the portfolio into a more defensive position. Given that a high GBP cash balance isn’t an attractive option, as the pound could fall in a difficult time for financial markets, I added more effective portfolio diversifiers in energy, grains, and the yen. With the main equity exposure in energy, commodities, and quality, this has brought the volatility right down to defensive levels.

The aim is to preserve capital should things get worse, in the full knowledge that when things improve, there will be an abundance of opportunities to explore. I want to ensure that capital is preserved until such time. It may well be that the war ends soon, there is a regime change in Iran, and stockmarkets rally. I would be delighted to see that and will gladly eat humble pie as we reinvest.

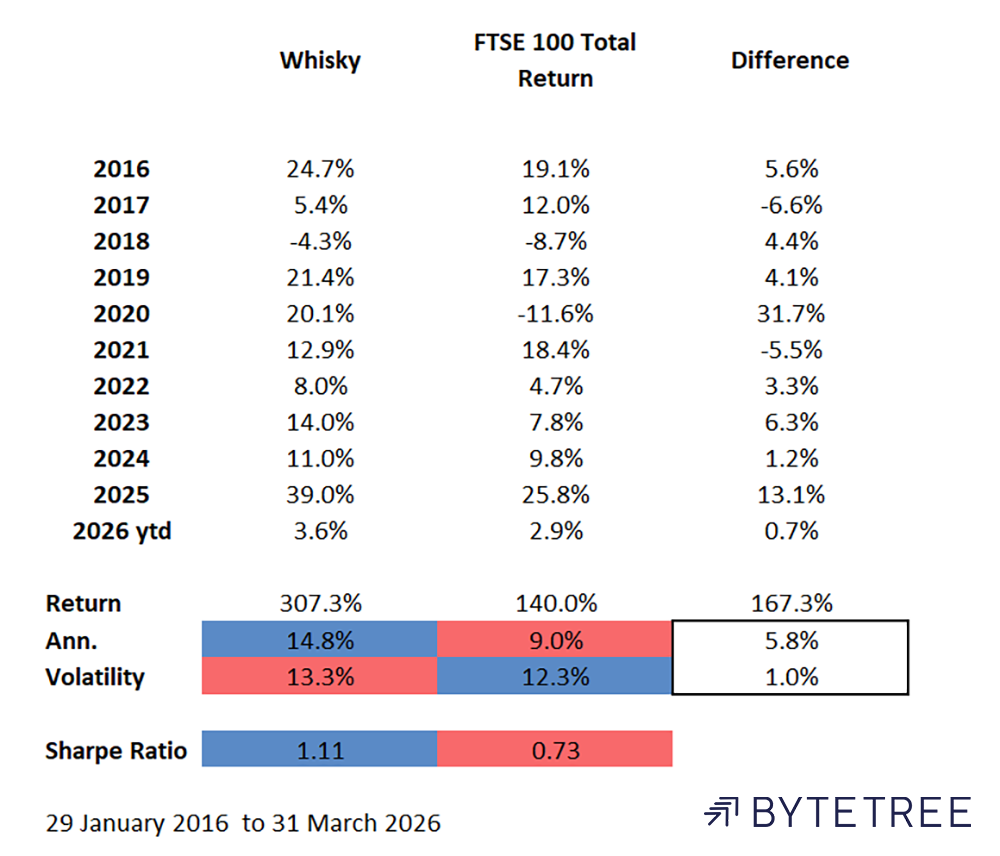

After a strong 2025, Whisky is marginally ahead of the FTSE 100 this year. It was much higher in January, before the crash in precious metals. Long-term performance remains strong.

Whisky vs FTSE 100

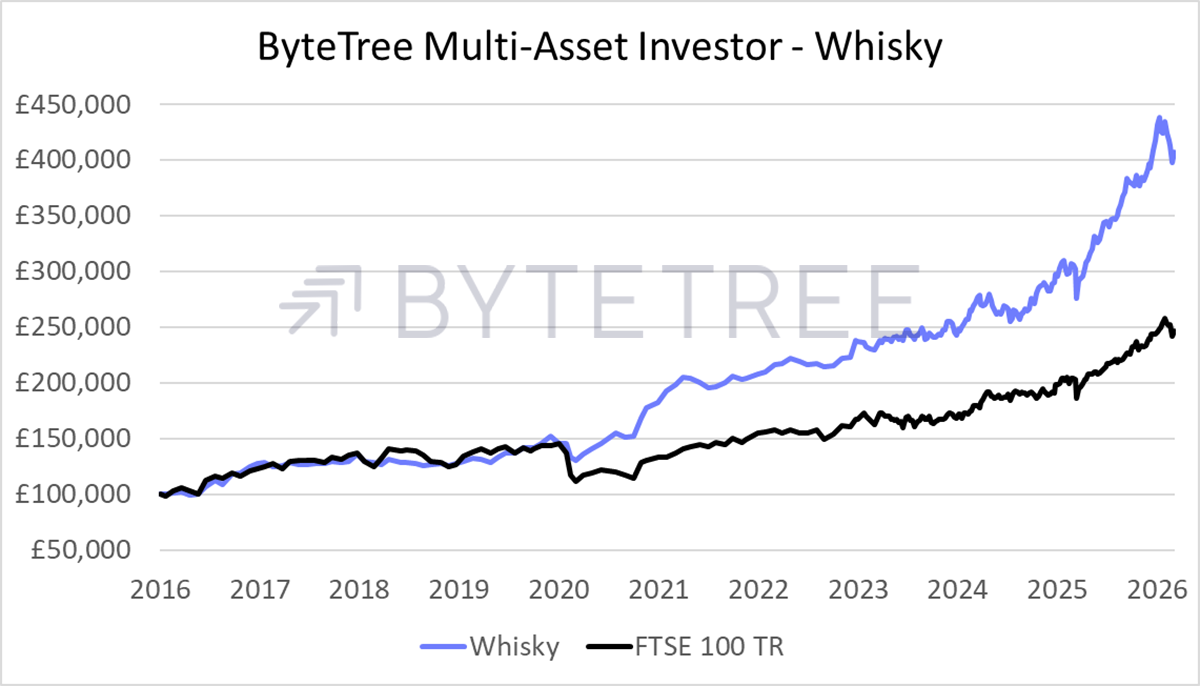

That performance comes to life in the chart below. The best year versus the market was 2020 when Whisky rose, and the FTSE slumped. It is during these darkest periods that a capital preservation first approach can yield the best long-term payoff.

Whisky Portfolio Performance

The Soda Portfolio

Soda followed similar lines, reducing equity exposure and adding diversifiers. In February, before the war began, I sold two investment trusts, Caledonia and Pantheon, because their exposure to private markets no longer seemed to be an attractive proposition. Fortunately, I had added energy exposure in January and switched some equities into a more defensive, actively managed fund.

In March, I sold some of the equity ETFs to reduce equity exposure and added short-term diversifiers in commodities and yen. UK index-linked bonds were also sold, and the asset allocation is now defensive.

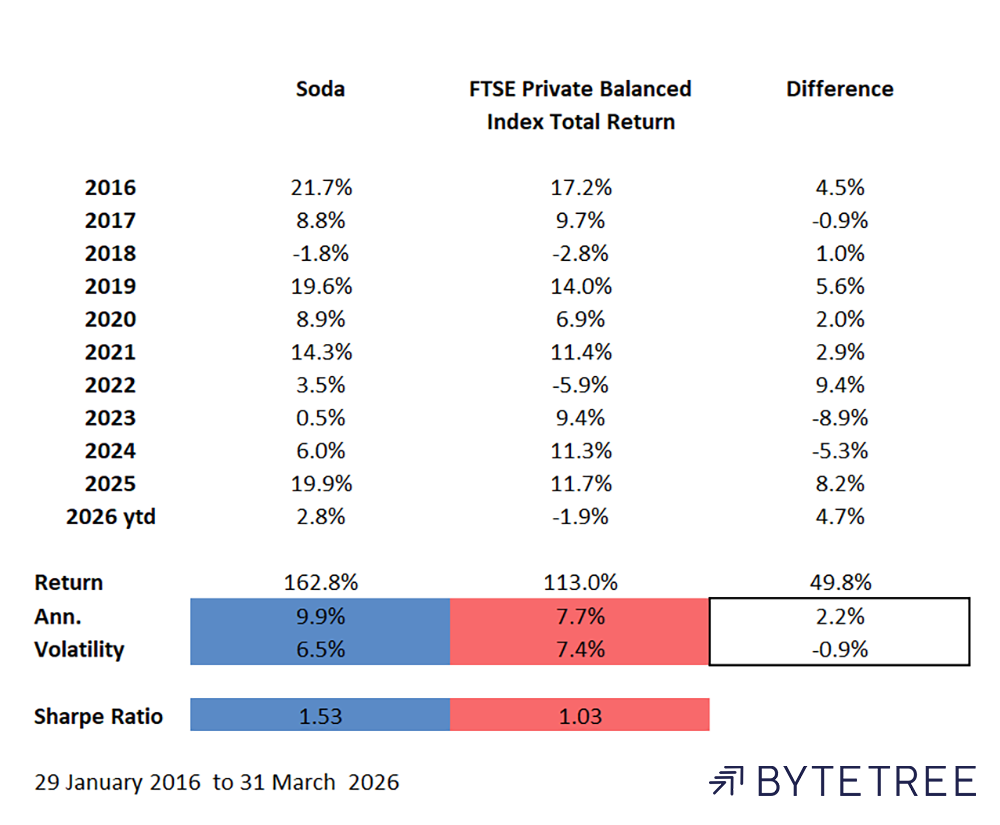

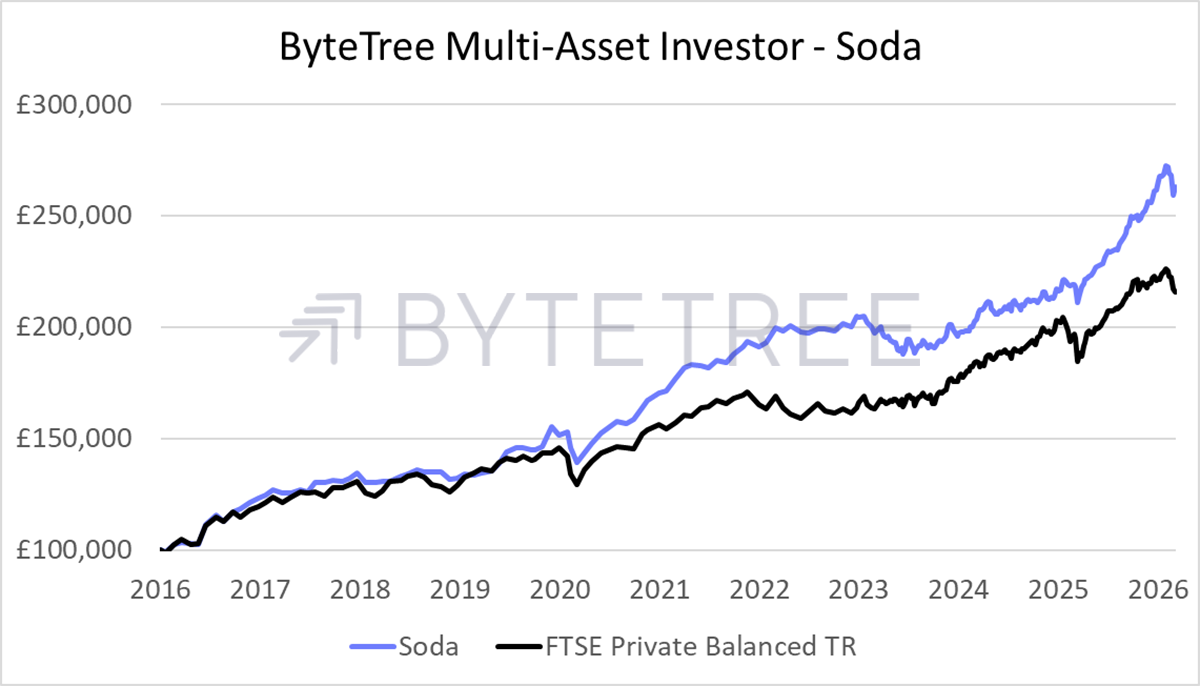

Soda is up 2.8% this year, which is a good result against the FTSE Private Balanced Index, which is a 60% equity, 40% fixed income strategy.

Soda vs FTSE Private Balanced Index

The longer-term performance has been improving since late 2024, after a patch where I failed to embrace the bull market in technology stocks. I sense that won’t matter again for quite some time, as the sector dominance has peaked.

Soda Portfolio Performance

The plan is not to worry about making gains in the short term, but over the medium to long term. That means preserving capital until better times are upon us.

The Recovery List

The best thing about uncertain times is that when they come to an end, opportunities will be in abundance. Back in February, it was getting harder to find cheap, good stocks than it had been a few months earlier. There were cheap stocks and good stocks, but not in tandem.

My recovery list is already underway and filling up nicely. It is important to have watch lists ready to go so that when the opportunity arrives, we are ready. I am much more interested in companies that have been out of favour for some time and are recovering than in simply buying oversold stocks. Our models at ByteTree keep improving, and by combining our Global Trends data with our valuation and growth models, we are able to cast a wide net across many countries and sectors. I have no doubt that when things improve, we are very well placed to capitalise.

The recovery list, where I note my best ideas for the future, is growing and now shows 30 companies. The common thread is cheap and good businesses that are out of favour. The highest returns follow low prices. The key is to have capital intact when the opportunity comes.

Thank you all for your support during these stressful times. No one likes churning their portfolio, but I feel we are there and can get back to some kind of normality. The good times will return, because they always do.

Please let me know your thoughts by emailing me at charlie.morris@bytetree.com or tweeting me @AtlasPulse.

Many thanks,

Charlie Morris

Editor, The Multi-Asset Investor

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd