Stablecoins – aka Crypto Cash

Stablecoins are among the fastest-growing sectors in crypto, not just in terms of market cap but also in usage. Stablecoin usage has consistently been strong across blockchains, and the regulatory landscape in the US, the largest market for stablecoins, has seen significant developments. This article will explore the stablecoin market, the regulatory developments, and provide a future outlook.

Introduction

A stablecoin is a type of cryptocurrency designed to maintain a stable value by pegging itself to an external reference asset. Most commonly, this would be the US dollar, but also other fiat currencies, commodities like gold, or baskets of assets have been used.

Today, the stablecoin market cap is hovering around $300bn. While growth has slowed since Q4 2025, it is quite respectable given how poorly the broader crypto market has been performing amid global uncertainty.

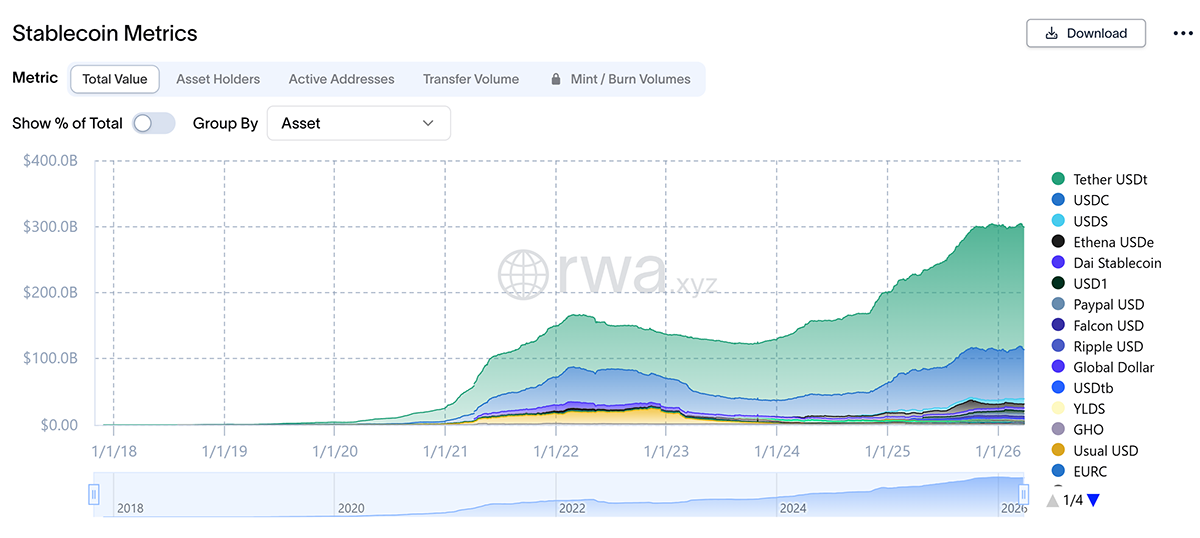

Stablecoin Market Cap by Asset

As shown in the chart above, USDT leads by a wide margin with a $185bn market cap, followed by USDC at $74bn, Sky Protocol's USDS at $7.8bn, and Ethena's USDe at $5.8bn.

Unlike Bitcoin (BTC) or Ethereum (ETH), whose prices fluctuate with market sentiment and network demand, a stablecoin is engineered to maintain a predictable, stable value. Naturally, this stability makes them the preferred medium of exchange in crypto. Traders and investors park value in them between positions and use them for value accrual, while protocols use them for liquidity, and consumers and businesses use them for cross-border payments.

A Brief History of Stablecoins

The stablecoin story began in July 2014 with BitUSD, which was issued on the BitShares blockchain by Charles Hoskinson (founder of Cardano) and Dan Larimer (founder of EOS). BitUSD was collateralised by BitShares' own volatile native token, which was an inherent structural flaw, as a sharp decline in BitShares could destabilise the peg. It ultimately de-pegged in 2018. Another early entrant, NuBits, launched in September 2014 using a similar model but with BTC as collateral. Unsurprisingly, it failed as well, unable to defend its peg during periods of market stress.

The breakthrough came in October 2014 with Tether, then called Realcoin. Unlike its predecessors, Tether offered a simple, auditable promise: one USDT would always be redeemable for one real US dollar held in the reserves. Initially built on the Omni Protocol on top of Bitcoin, Tether later expanded to Ethereum, Tron, Solana, and several other chains. Despite years of controversy over reserve transparency, Tether grew to become the most traded asset in crypto, surpassing Bitcoin in daily volume as early as 2019. Notably, in an announcement on 27 March 2026, Tether revealed that they had hired KPMG to conduct a full audit of its reserves and brought in PwC to prepare internal systems for that audit.

The first major growth wave for stablecoins began in 2021, where the stablecoin market cap grew from $25bn on 1 January 2021 to over $165bn in March 2022, driven by the crypto bull market and the explosion of DeFi activity. The UST collapse in May 2022 and the brief USDC de-peg during the Silicon Valley Bank failure in March 2023 triggered sharp contractions and regulatory alarm. The market stabilised and rebounded, with 2025 marking a definitive return to confidence, as the total market cap rose a little over 50% in the year, from $198bn in January to just over $300bn by October. This marked a meteoric rise in the significance of stablecoins, making the sector large enough to compel regulators to introduce dedicated stablecoin regulation. More on that later.

Stablecoins are broadly split into two camps: centralised and decentralised.

Centralised Stablecoins

Centralised stablecoins are issued by a legal entity, typically a financial company or trust, that holds a corresponding pool of reserve assets in custody. For every token minted, the issuer holds one unit of the underlying asset (usually one US dollar in treasuries, cash, or equivalents) in a reserve. The issuer is also accountable for regular reserve reports and for guaranteeing 1:1 redemption.

Tether's USDT and Circle's USDC are the canonical examples of centralised stablecoins. Their strength lies in their simplicity, liquidity depth, and regulatory clarity. Their weakness is the trust requirement: users must believe the issuer is solvent, transparent, and not misusing reserves. This is a concern that has periodically shadowed Tether throughout its history.

Decentralised Stablecoins

Decentralised stablecoins operate through smart contracts rather than trusted intermediaries. They typically maintain their peg through one of two mechanisms: over-collateralisation or algorithmic supply management. Over-collateralised models, like MakerDAO's DAI (now Sky Protocol’s USDS) and Aave's GHO, require users to deposit crypto assets worth more than the stablecoin they receive, creating a buffer against price declines.

Meanwhile, algorithmic stablecoins, which attempt to maintain pegs through automated supply expansion and contraction, have a troubled track record. The most catastrophic failure was TerraUSD (UST), which collapsed in May 2022, erasing tens of billions in market value virtually overnight and triggering a broad wave of regulatory scrutiny. The UST collapse established the defining lesson of the decade: stability cannot be conjured by code alone without robust, high-quality collateral backing it.

A third, hybrid category has also emerged. Ethena's USDe, for instance, uses a delta-neutral strategy, combining assets like stETH with offsetting perpetual futures short positions to maintain its dollar peg while generating a yield. This synthetic approach does not rely on fiat reserves, yet it is also not purely algorithmic, representing a sophisticated middle ground that has attracted significant interest.