Sanctuary in Asia

A new chart for the textbooks, where the price of oil rises and falls by 30% in a single day. To put it into a historical context, I show it using quarterly data, but yesterday’s daily range was between $83.66 and $119.50.

Brent Crude Quarterly – 20 Years

The oil price is the most important financial metric in this conflict. The price of energy drives the economy, and the cheaper it is, the better. A price surge can trigger a recession, just as it did in 2008. The similarities are there, as companies in private credit are starting to come under pressure. But $140 in 2008 was much higher than it is today, as inflation has reduced purchasing power by 50% in the USA, and 67% in the UK. I would add that the troubles in private credit may prove significant, but I doubt they match the banking crisis of 2008.

Markets were calmed as ships started moving in the Gulf, albeit at much higher freight rates, and Trump declared victory. But the supply chain has once again been tangled, and it will take time to ease. The good short-term news is that the oil price has likely peaked, meaning the worst for markets may be behind us.

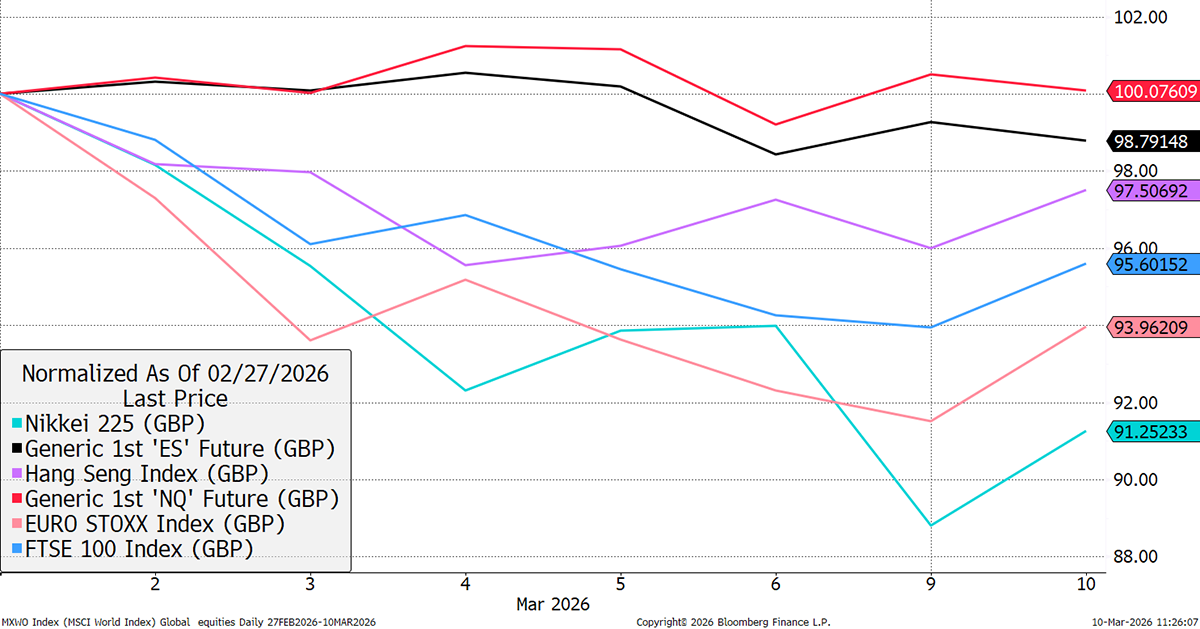

Yet the World Index fell by 3.7% peak to trough since last Friday, ahead of the strikes. The US market barely felt it, while Europe and Japan took the brunt. For reference, “ES” (black) is the S&P 500 future, and “NQ” (red) is the Nasdaq.

Shock Hits Europe and Japan; US Insulated

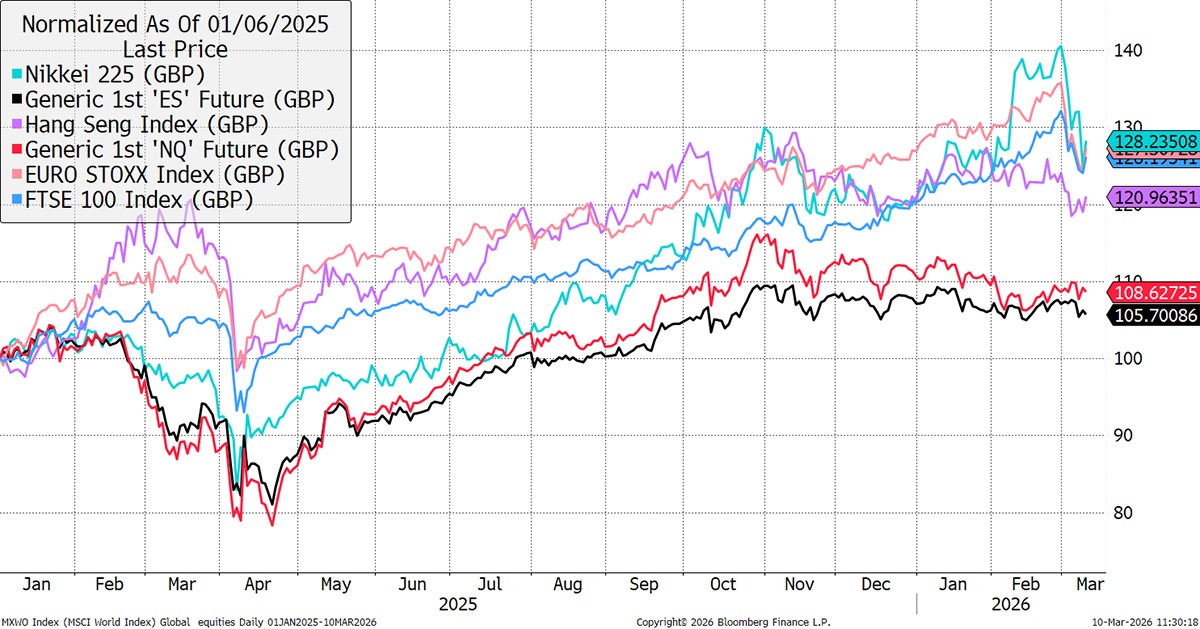

This comes in stark contrast to the prevailing trend since January 2025. Over that longer period, the lag in US equities remains clear.

Rest of World Outperformance since January 2025

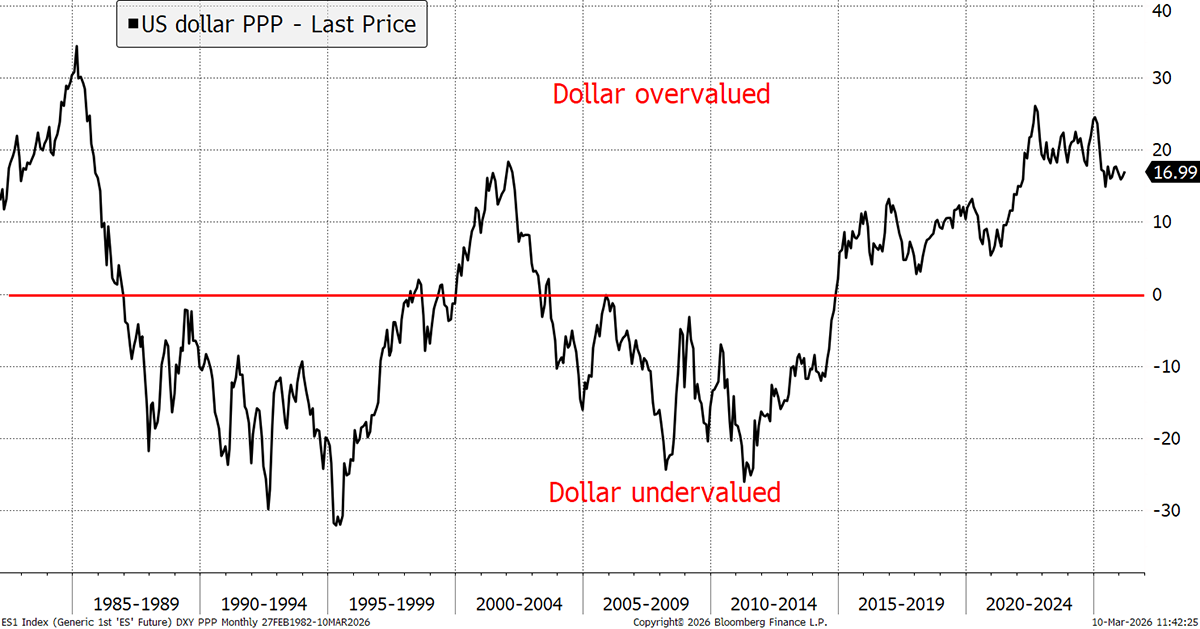

The ByteTree Portfolios have been on the right side of the big trends over the past 15 months, but on the wrong side over the past 7 days. The dollar has risen alongside oil, and both have slid back in yesterday’s reversal. In the short term, the dollar and oil will continue to inversely reflect the appetite for risk. I can see how the dollar will hold up amid geopolitical tensions, but it’s expensive and has the potential to fall a long way from here. If they start printing money to fund expensive wars, that could happen quickly.

Dollar Purchasing Power Parity

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd