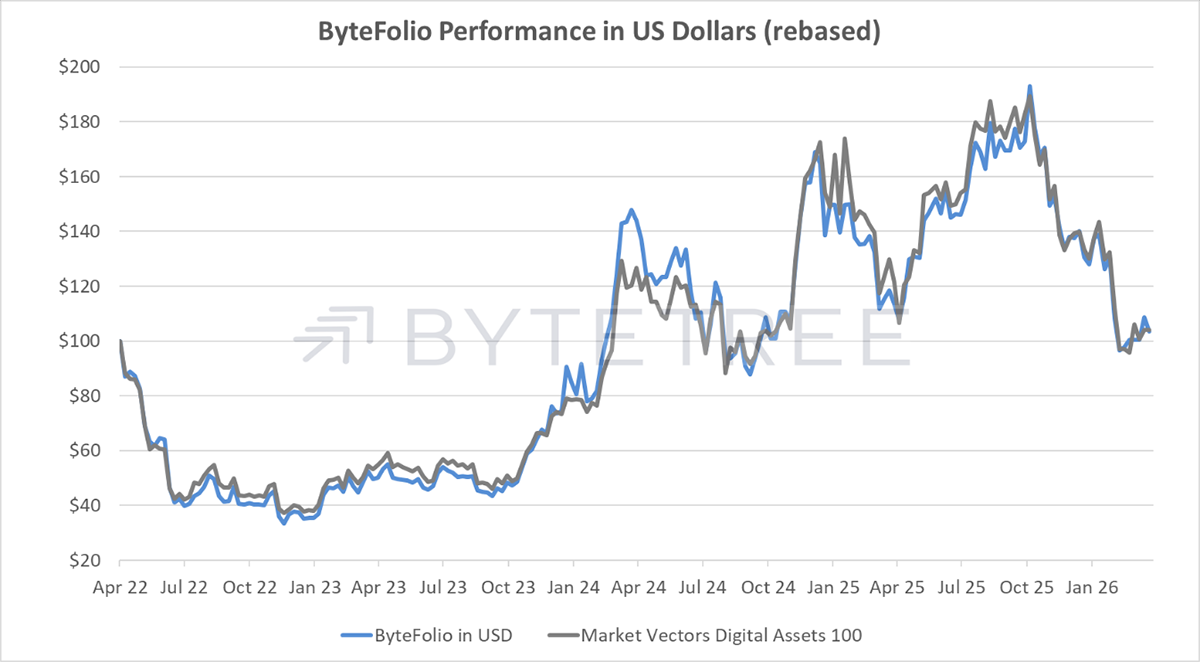

Revisiting Crypto Equities

ByteFolio Issue 202;

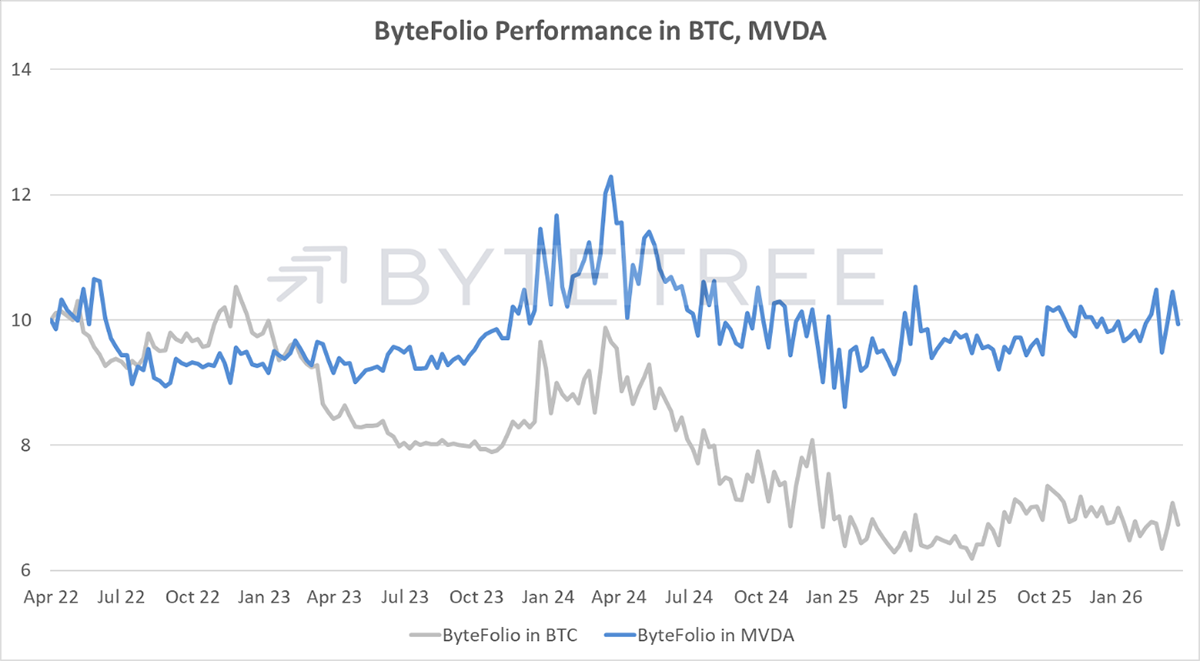

Bitcoin’s ByteTrend Score holds a 3. The price hasn’t touched the 20-day minimum since early February, but it will take a few months for the 200-day moving average to stabilise.

Bitcoin

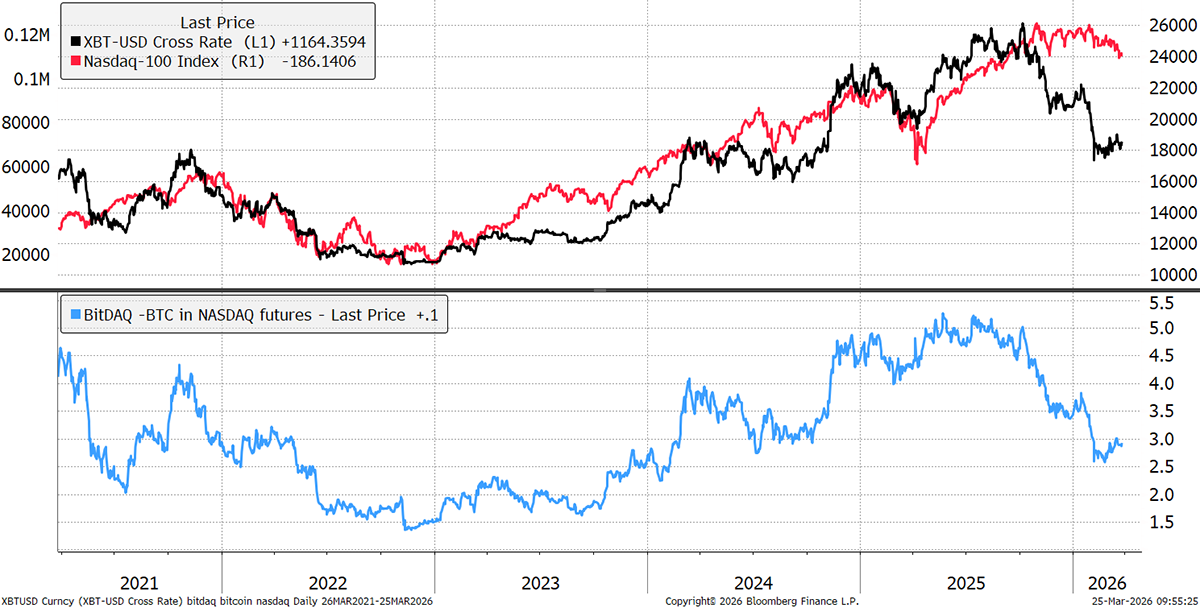

Yet against the Nasdaq, the last two months have been productive. Not exactly a bull market, but it’s an interesting time when the world’s largest stocks fall while Bitcoin makes modest gains. I have always felt that this is one of the most important charts for Bitcoin.

Bitcoin in Nasdaq

When Bitcoin is outperforming its natural rival, tech stocks, the Bitcoin ETF buying strengthens. What’s more, investors don’t sell aggressively when it’s lagging behind.

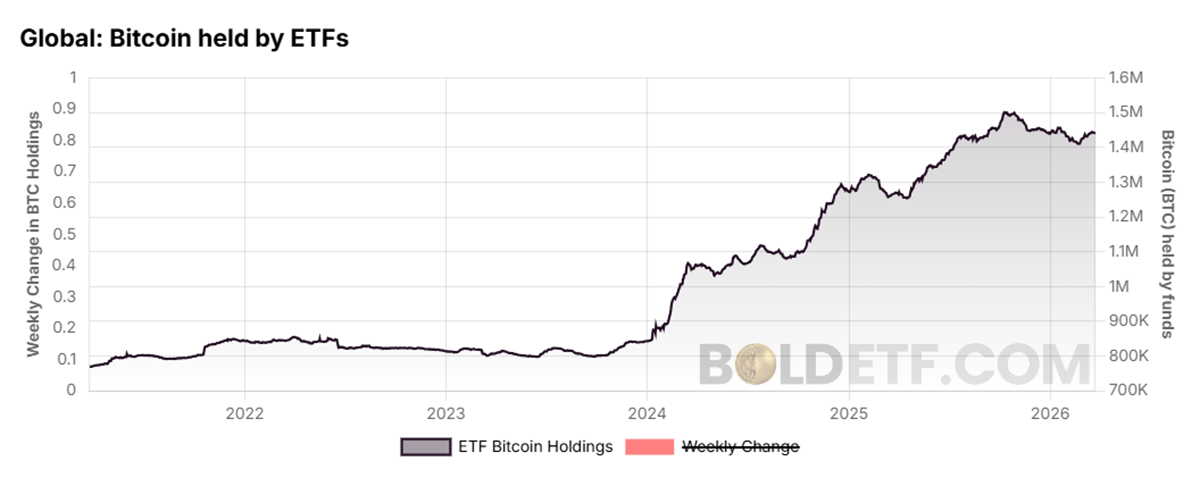

Bitcoin Held by ETFs

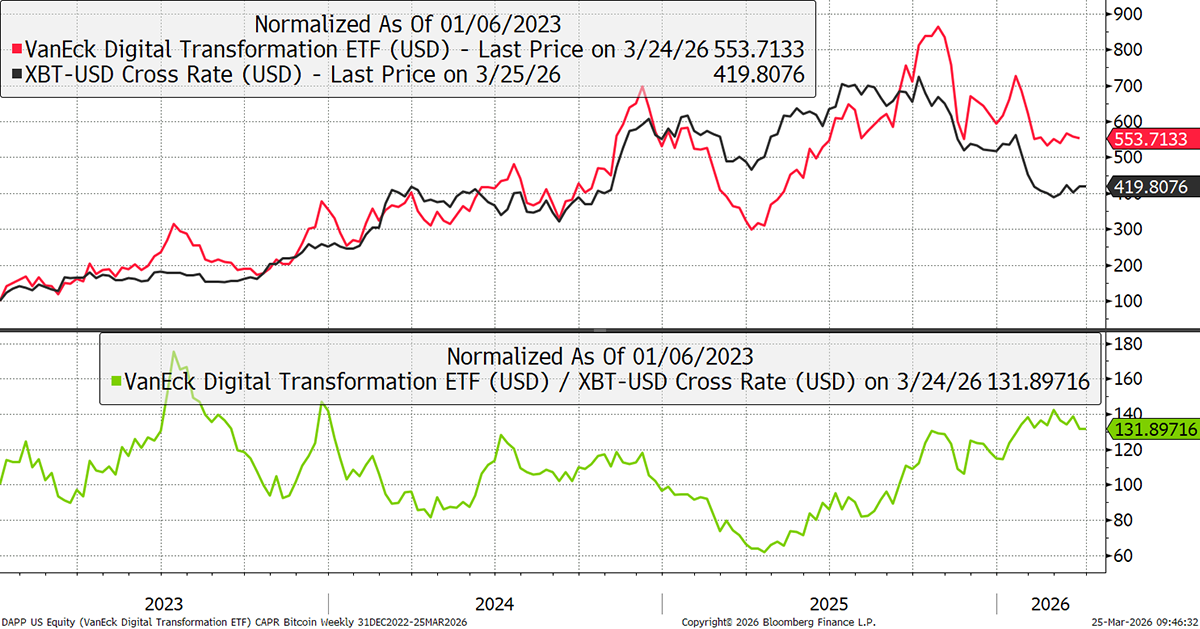

Although the Nasdaq is home to big tech, it is also where the crypto stocks are listed. Since the last bull market began, it is remarkable how crypto stocks have beaten Bitcoin by 31%.

Bitcoin vs Crypto Stocks

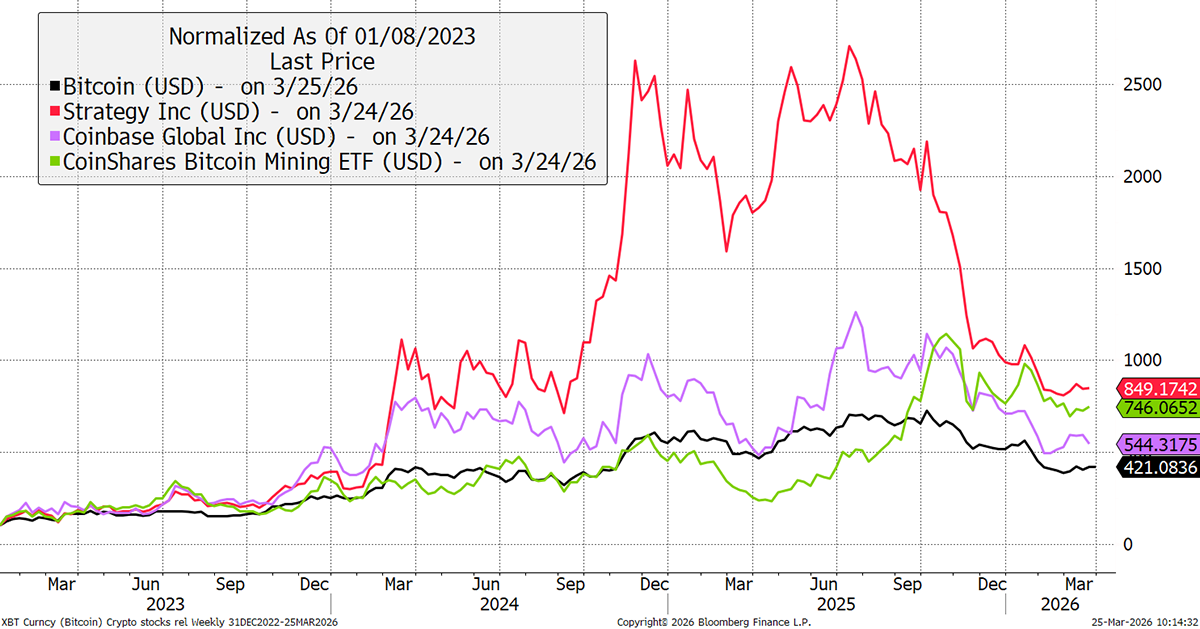

The giants are Coinbase ($48bn) and Strategy ($45bn). Circle ($24bn) is mentioned below, but it is a newcomer. Coinbase is the king of the sector with its fingers in every pie, while Strategy is the Bitcoin hoarder. I also show the CoinShares Bitcoin Mining ETF (WGMI), which has done much better than you might expect from past cycles.

Bitcoin Stocks

The miners were pure-play leveraged bets on Bitcoin, as revenue came almost entirely from block rewards and transaction fees, which would fall sharply when the Bitcoin price fell. However, they are no longer dependent on Bitcoin mining alone and have diversified, pivoting into AI.

After the 2024 Bitcoin halving, the miners repurposed their existing infrastructure, with cheap power contracts, massive data centres, and secure locations, for AI/ high-performance computing (HPC) workloads. These pay 3–5x more revenue per megawatt than Bitcoin mining. By late 2025, many were generating meaningful non-mining revenue, with projections that mining could drop to under 20% of total revenue for some by 2026. Pure-play miners without the AI pivot have lagged, while diversified ones have thrived. It’s an interesting development that has now been tested in a bear market.

While it’s encouraging to see diversification among the miners, crypto stocks are not immune to external developments, particularly legislation. Progress on the CLARITY Act – the comprehensive legislative framework for crypto assets in the US - has been stalled for months, with disagreements between banks and crypto companies, particularly around stablecoin yield. Under the GENIUS framework, stablecoin issuers like Circle are prohibited from directly offering yield to holders, though third-party platforms can still provide yield products on stablecoins they hold. Banks argue this creates a loophole, and their concern is straightforward: if stablecoins were permitted to offer yield directly, they could rival traditional savings accounts and trigger deposit flight from the banking system, a direct threat to their core business model.

Markets responded swiftly when a draft of the CLARITY Act surfaced yesterday, 24 March, as it revealed the prospect of strict limits on stablecoin yield. Circle fell 20% and Coinbase, a major force behind USDC, dropped around 10%. The proposed legislation would reportedly bar rewards on passive stablecoin balances and ban structures "economically equivalent to interest," striking at one of the key incentives that has driven USDC adoption.

Circle Internet

Prior to yesterday’s sell-off, Circle had been on a strong run since February. The general consensus is that the drop reflects a short-term market overreaction to the news, as the long-term prospects of stablecoins remain unchanged. We will also be publishing a Token Takeaway deep dive on stablecoins later this week.