Food for Thought

Trade in Whisky;

The winds have changed, and we have reset the sails in The Multi-Asset Investor. It has been a busy period, possibly the busiest ever, but following recent portfolio changes, we are over the hump. I feel much more comfortable after boosting the allocation to commodities, outside of precious metals, and reducing equity exposure in this environment.

In a market that has seen both stocks and bonds fall at the same time, adding commodities makes good sense, especially as the strength in energy is almost certain to spill over into other areas, notably agricultural commodities. Before we start, and to follow up on Friday’s note, I want to clarify the dividing lines between the portfolios in terms of potential commodity exposure.

Update on Commodities at ByteTree

The Soda Portfolio will consider investments in physical gold, diversified commodity funds, diversified commodity equity funds, trusts and ETFs. It is unlikely to go far beyond that.

The Whisky Portfolio will embrace physical silver, oil, commodity equity ETFs, individual large commodity stocks, and commodity subgroups such as energy, grains, softs, and industrial metals.

Venture will embrace individual commodity stocks, large and small, and individual commodities, such as copper, wheat, etc.

I will ensure that all Soda investments are widely available on the platforms. For Whisky, I shall offer alternatives, where possible, for those who are unable to buy commodity funds. In Venture, the investors already know what to do.

The Adaptive Asset Allocation Report (AAA)

The Adaptive Asset Allocation Report (AAA), written by Robin Griffiths and Rashpal Sohan, is normally invested in equities. As of their recent note, they are now 75% invested in commodities, which is a significant change. The AAA is a high-level trend-following service that locks onto the strongest asset classes, whether they be bonds, equities (mainly countries) or commodities. This has the advantage during times of major disruption, as it has the freedom to follow a completely different path from a traditional portfolio.

I fully understand why they have done it, because it is the outcome of a clear investment process, driven by a model. It may do extremely well, but it is clearly concentrated. I will also embrace commodities, not so much to make hay, but to diversify and ensure a satisfactory outcome in what has become a difficult environment for equity markets. For those who want to go much deeper with their commodity journey, the AAA is a good option.

$100 Oil in the USA

Trump has gone out of his way to intervene by issuing reassuring statements whenever West Texas Intermediate (WTI) oil touched $100. It has now passed through that level, which will bring the Iran War closer to home.

WTI Crude Oil since Hostilities Began

I show some notable statements from Trump and his team:

- March 3: “prices are going to drop… lower than even before” once the conflict ends.

- March 5: Trump states he has “no concern” about rising U.S. gas prices, reiterates they “will drop very rapidly when this is over,” and gives a 4-to-5-week timeline for the military campaign while expressing confidence the Strait of Hormuz will stay open.

- March 9: the war with Iran is “very complete, pretty much” and “will end very soon.” The price run-up is “just fear and perception… not any shortage”.

- March 10: Trump and White House officials repeat that the operation is “ahead of schedule”.

- March 11: The International Energy Agency (IEA) announces the largest-ever coordinated release of 400 million barrels from emergency stocks—framed by U.S. officials as a direct stabiliser.

- March 16: Treasury Secretary Scott Bessent tells CNBC the U.S. is “fine with” and actively allowing Iranian oil tankers (and those from partners like India/China) to transit the Strait of Hormuz.

- March 19: Israel publicly commits to assisting the U.S. in reopening the Strait of Hormuz (and reportedly refrains from further strikes on Iranian energy sites at U.S. request).

- March 23: Trump posts that the U.S. and Iran have had “very good and productive conversations” toward “a complete and total resolution,” announces a five-day pause on strikes against Iranian power plants/energy infrastructure, and says talks will continue all week.

- March 24: Trump claimed Iran had given the U.S. a "very big present" worth "a tremendous amount of money".

- March 29: Trump claimed negotiations with Iran were going "extremely well" and that the U.S. was "getting a lot of the things that they should have given us a long time ago."

- March 30: Trump claimed "great progress" in discussions with a "new and more reasonable regime" in Iran but renewed threats: If no deal is reached "shortly" and the Strait of Hormuz is not "immediately 'Open for Business," the U.S. would "blow up and completely obliterate" Iran's electric generating plants, oil wells, Kharg Island, and possibly desalinization plants.

The markets have no choice but to listen to Trump. They have learned from past episodes to take him “seriously, but not literally”, a comment from the tariff debacle. In recent days, the market has started to focus on rate cuts instead of hikes. Before this started, rate cuts were on the agenda and baked into market expectations. A large part of the recent turmoil in equity markets has come about as a result of this change, which could be described as a second-order effect following the spike in the oil price.

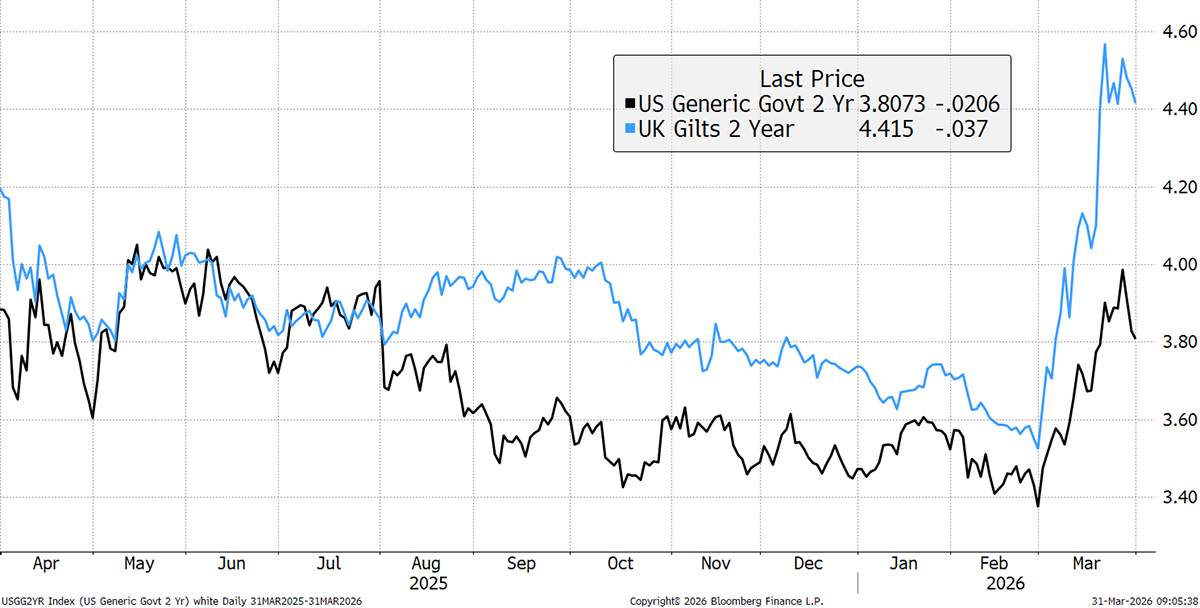

US and UK 2-Year Bond yields

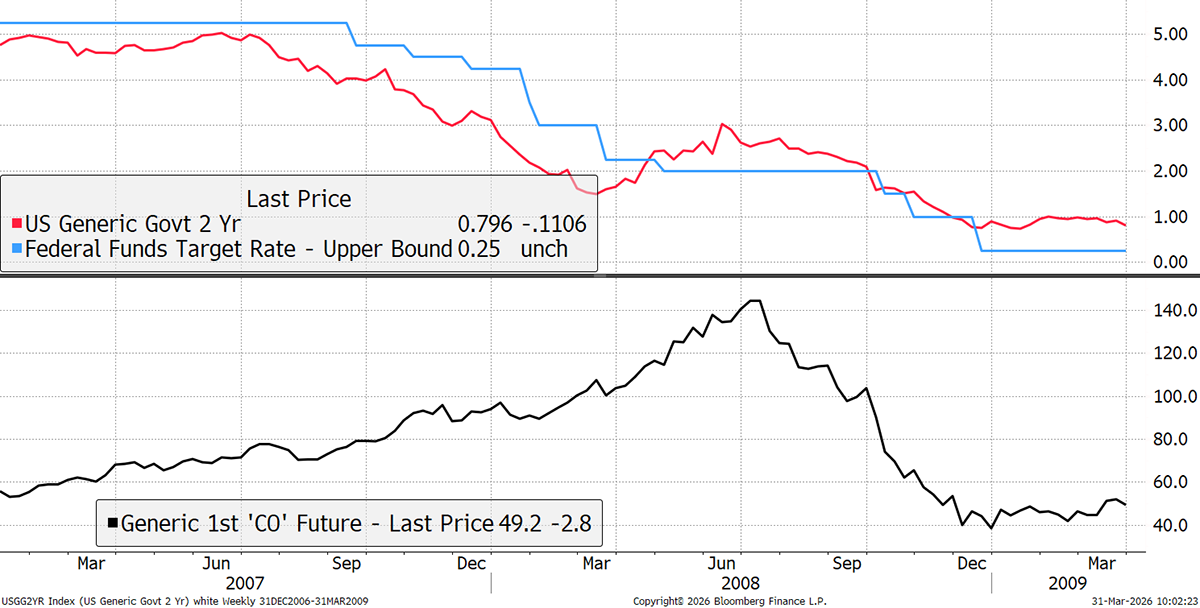

While only a few days in, the market may be following the 2007/8 playbook where oil spiked (black), but bond yields (red) fell in the face of rate cuts (blue). This all happened while inflation was rising due to the oil price. As the saying goes, the best cure for a high oil price is a high oil price, as demand destruction sets in as the economy slows. In that sense, the bond market was right.

Crude Oil Boom and Rate Cuts in 2007

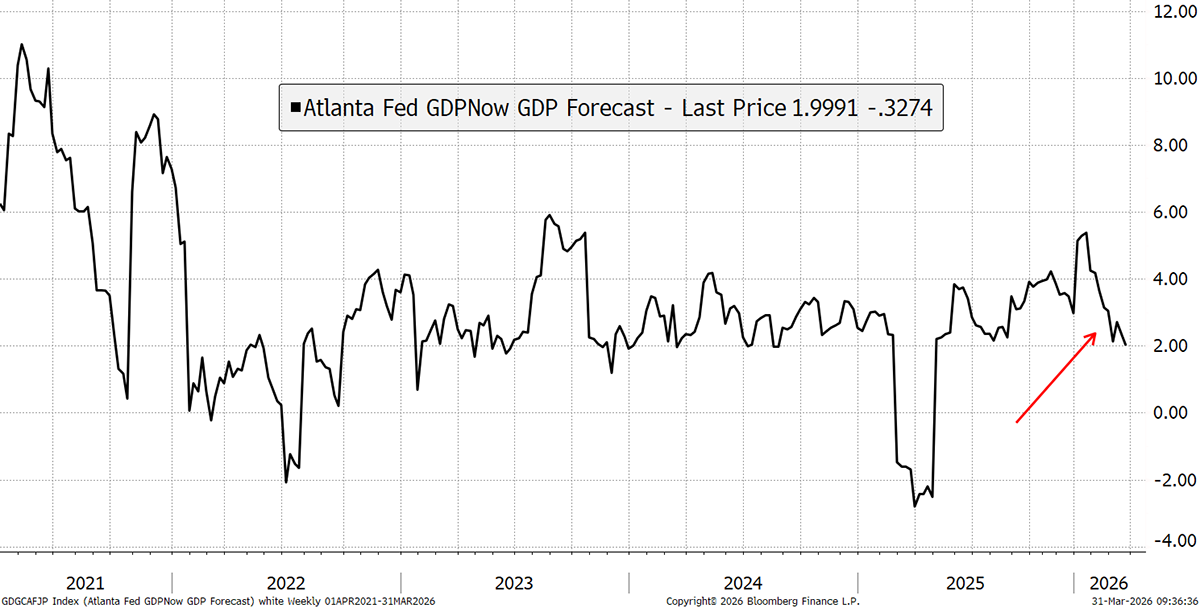

This comes amid lower growth expectations for the US economy, with the Atlanta Fed “GDP Now” models showing signs of a slowdown. These are volatile, but the direction is clear.

Lower Growth Expectations

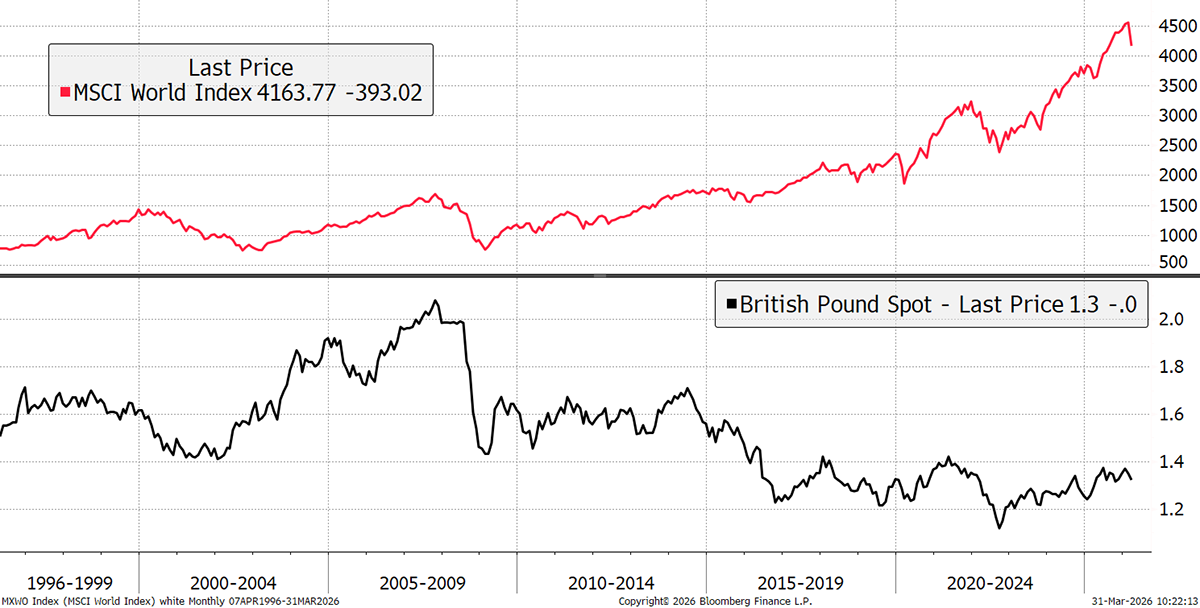

We also have a stronger dollar, especially against the pound, which is starting to weaken. The pound has a history of being correlated with equity markets because London remains a major financial centre.

The Pound and Stockmarkets

While cash is king in times of trouble, I do not believe sterling provides the answer. If it falls, as it normally does at times like this, it will lose purchasing power. That is why I bought the yen, and will find new opportunities so sterling balances don’t rise too far. This will take time.

The convergence in bond yields between Japan (black) and the USA (green) continues to narrow (blue). Historically, this has supported a strengthening of the yen, but in recent years, it still hasn’t happened. Historically, the yen has had a safe haven role during times of financial stress, and despite my last attempt at this trade, I believe this once again makes sense. If we do have a financial shock, the yen will surely run hard.

Japan and US 10-Year Bond Yields and the Yen

What’s more, this is exactly what happened in 2008, the last time the oil price surged during a macroeconomic shock. I could be wrong on this, and the yen may sit on the sidelines. In any event, I believe it is a good diversifier against a GBP cash balance.

Notable Stockmarkets

Chinese banks are proving to be a safe haven in this crisis. The Chinese yuan is one of the few currencies proving to be stronger than the dollar. In addition, recent economic data show robust exports and buoyant consumer spending. No action here at this time, but we should get used to the idea that China may emerge stronger from this war without having fired a single shot.

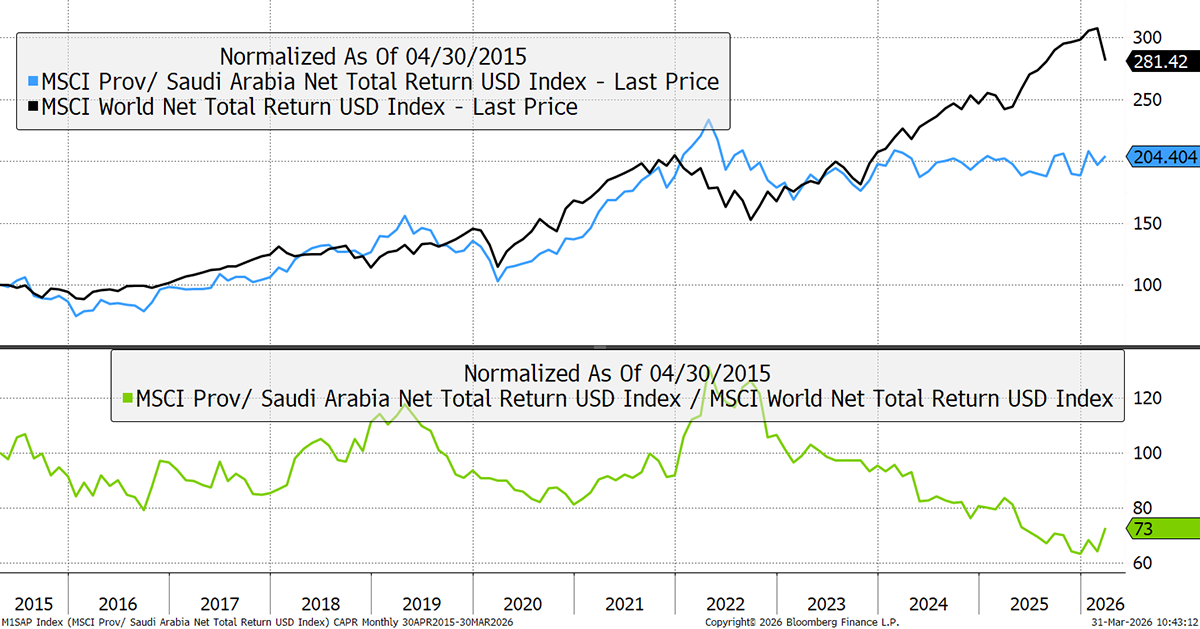

The other notable market is Saudi Arabia. ByteTree’s Global Trends Model has been lighting it up, and its recent strength comes off a low base. Saudi Arabia is a cheap market, dominated by banks and industrial companies in chemicals and fertilisers. There have also been reforms, such as freeing up ownership for global investors from 1 February. Foreigners barely own Saudi Arabia, and this comes at a fascinating time.

Saudi Arabia versus the World

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd