An Uptrend Brews in the Bond Market

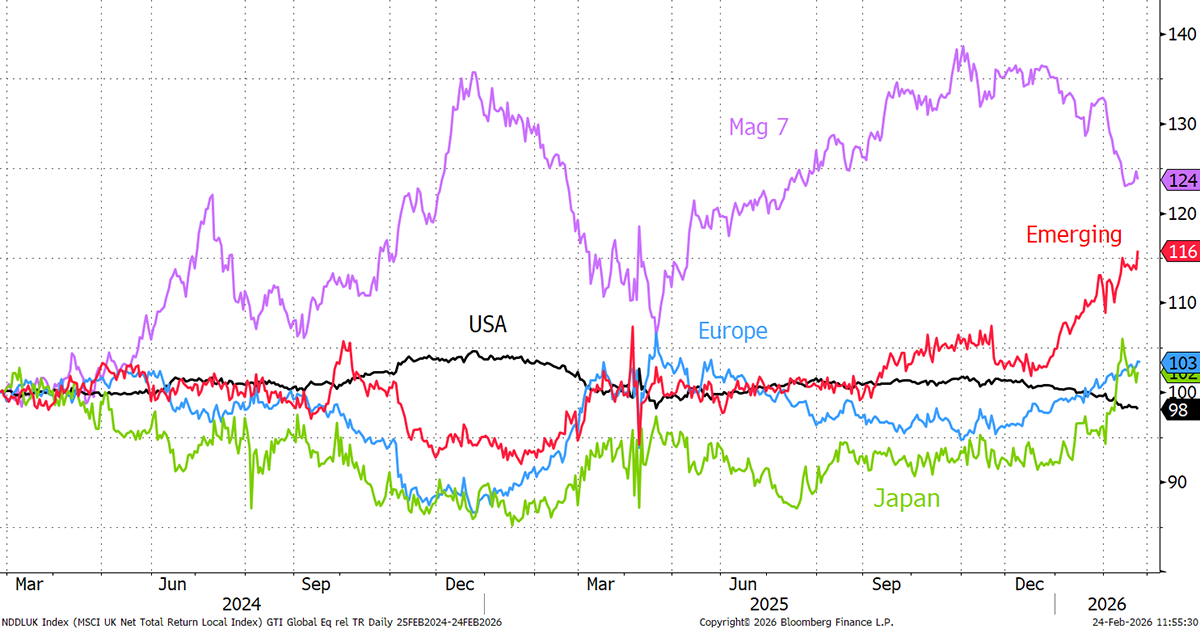

There have been some major developments since the tech peak in October. Since early 2025, the divergence between the US market and the rest of the world has been widening. The Magnificent 7 - largest US tech stocks - did well until October but have turned down sharply since. In the meantime, emerging markets have been strong, followed by Europe and Japan. Over the past two years, the USA has been sliding versus the world.

Major Regions Versus the World

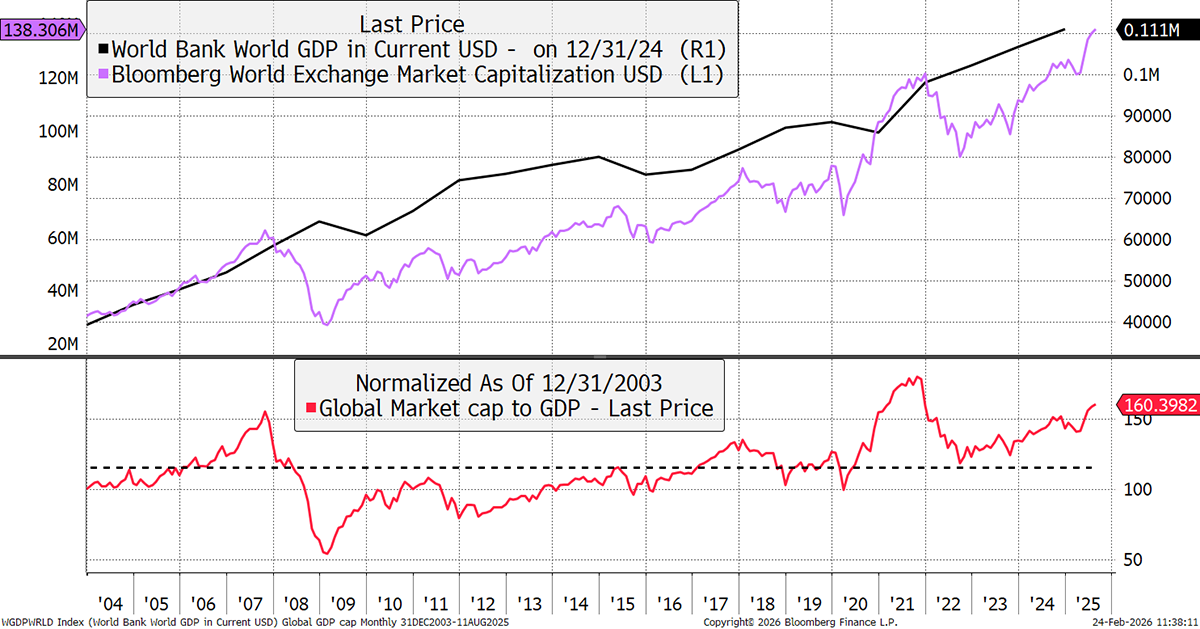

It’s all well and good to be in the right place and watch the US tech collapse (semiconductors excluded) from the sidelines, but as the saying goes, if the US sneezes, the rest of the world catches a cold. In the bigger picture, we should be concerned about global equity valuations. The value of global equities is now 160% of GDP, which is above the 2007 level, ahead of the credit crisis, and catching up with the bubble of 2021. Valuations are uncomfortable up here as stocks are ahead of the economy.

Global Equity Valuation versus GDP

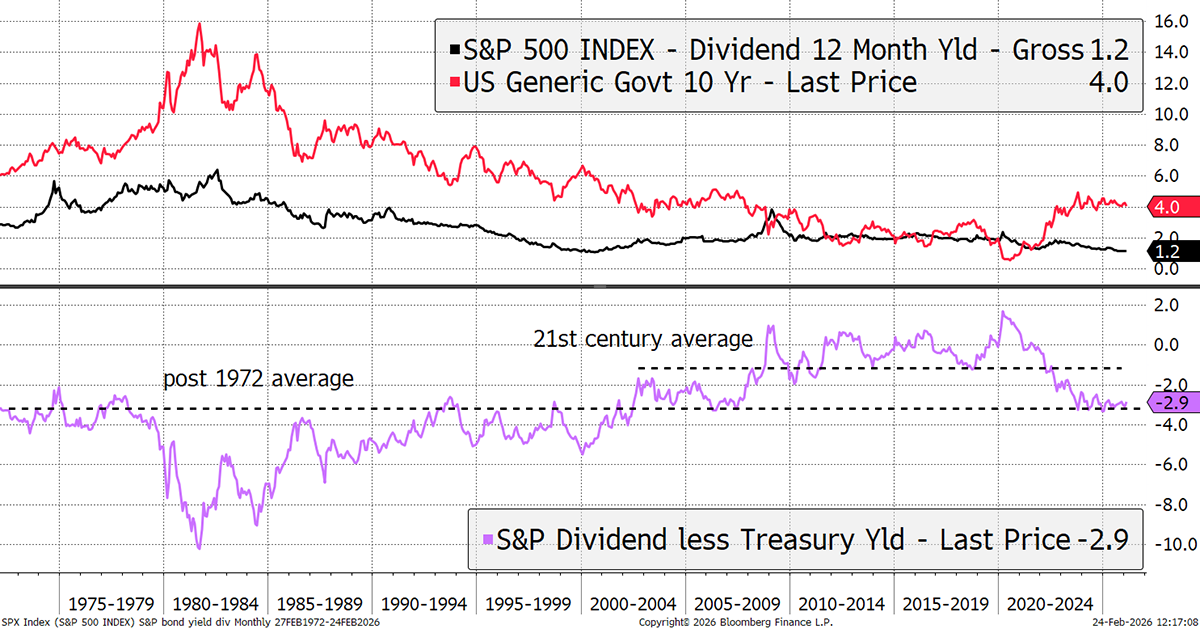

Naturally, we can blame US tech, most of which is now in retreat. Following the devastating bond bear market of 2021/22, bonds now yield 4% against the S&P 500 of 1.2%. That low equity yield was last seen in 1999, when equities turned down sharply. Now that bonds have started to rally, the concern is that a 2.9% “yield gap”, rarely seen in the 21st century, will be seen as attractive by large investment institutions seeking safety. If they buy bonds, they’ll have to sell equities.

The US Yield Gap – Bonds versus Equity Yields

Of course, for bonds to behave, we need to see inflation in check, and although the picture remains mixed, it is unlikely to run away in the medium term. The bond market has started to rally, and this matters because investors once again have a choice. During the last bond bear market, they didn’t, and in order to avoid losing money in bonds, investors bought stocks en masse.

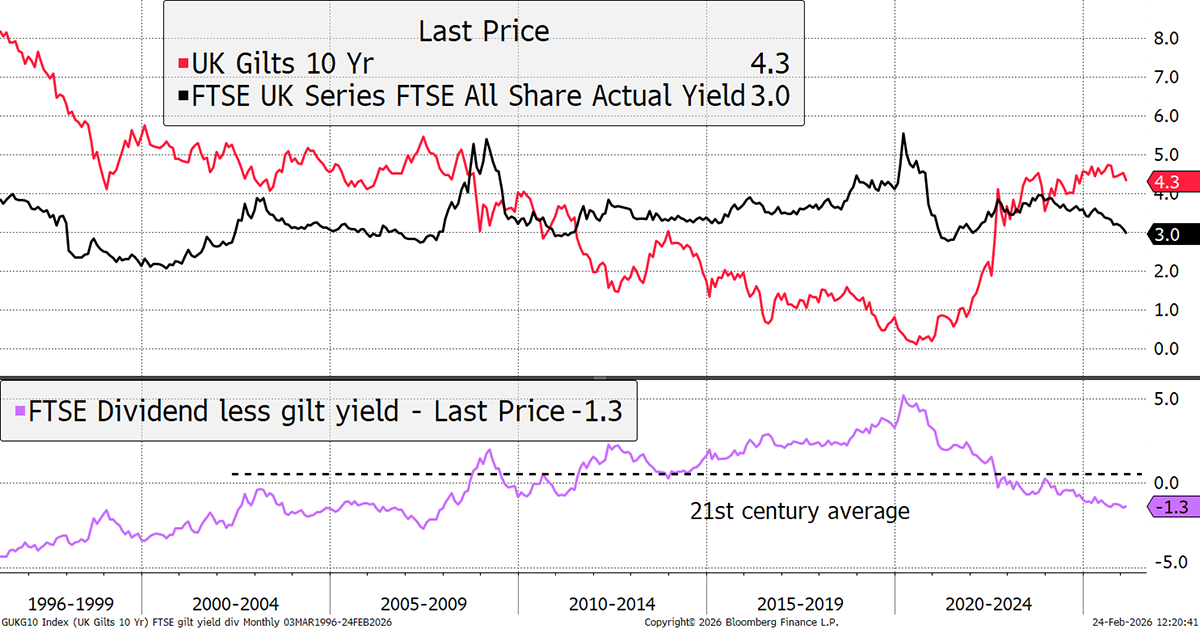

The UK is in a slightly better position than the US, but not by as much as many would think. The FTSE yield is 3% compared to 2% in 1999, and the 10-year gilt 4.3%. The yield gap is not as wide here, which is a good thing, as it suggests that equities may have more to give. But make no mistake: the best is behind us.

The UK Yield Gap – Bonds versus Equity Yields

I have no doubt that our focus should, in the main, stay focused on non-US equities. I also think we should consider going a step further. In recent months, I have shifted from a go-go profit-seeking portfolio, albeit with a heavy value bias, to a more robust all-weather portfolio. I might have been a little early in that move, but it has begun. Generally speaking, in financial markets, it is much better to be early than late.

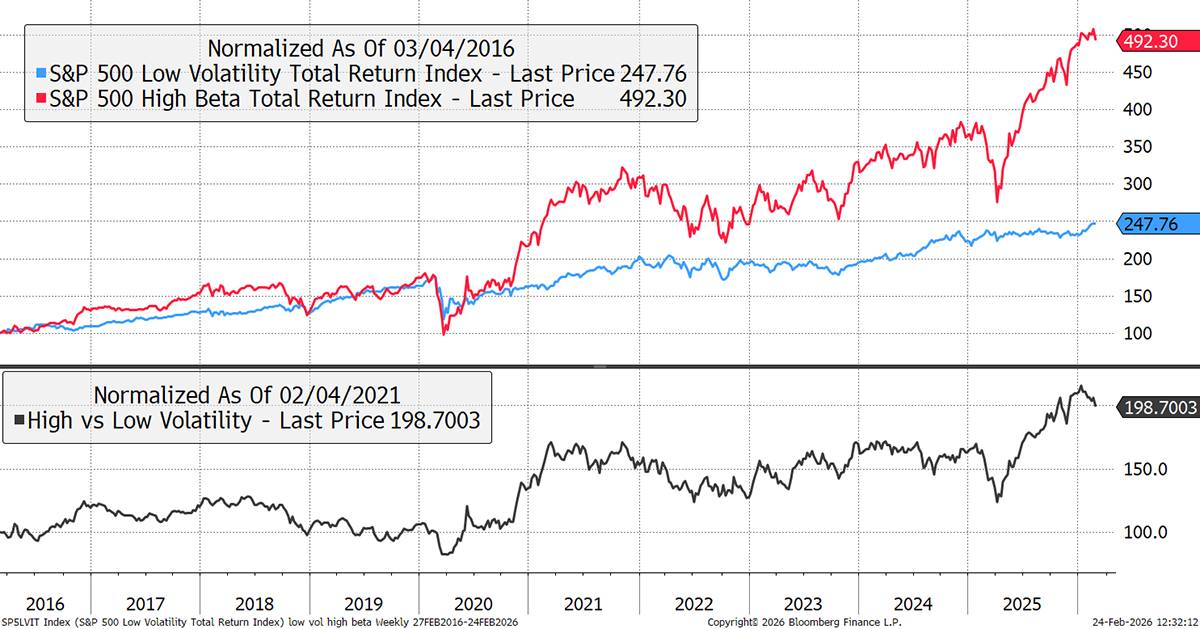

The volatile “high beta” speculative stocks (red) look like they have peaked, while the cautious low-volatility stocks have broken higher after a prolonged pause. This often coincides with strength in the bond market. The recent boom in speculative stocks has been too much, and will end in tears, just as it always does.

Low-Volatility versus High Beta Stocks

I repeat this important message because if the bond market starts to strengthen, then equity selling will follow. The valuation gap is wide, and fears over valuations, economics, and geopolitics are brewing. A healthy bond market will provide an escape hatch.

An uptrend is brewing in the bond market, as yields have started to fall, and therefore prices rise. The 200-day moving average (purple) is now rising for the 10-year US Treasury, and that is unexpected. The narrative is one of fiscal exuberance, a collapsing dollar, and high MAGA growth expectations, but what if things are more normal than they seem?

US Ten-Year Synthetic Bond Price – Trend Is Improving

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd