The Quality Opportunity Grows

Following President Trump’s address last night, the Iran war continues. In March, the oil price has been the primary driver of global financial markets, and the varying correlations among companies and assets are falling away as it dominates. Energy prices determine the likely path of inflation and, therefore, interest rates. These are important in price setting for financial markets.

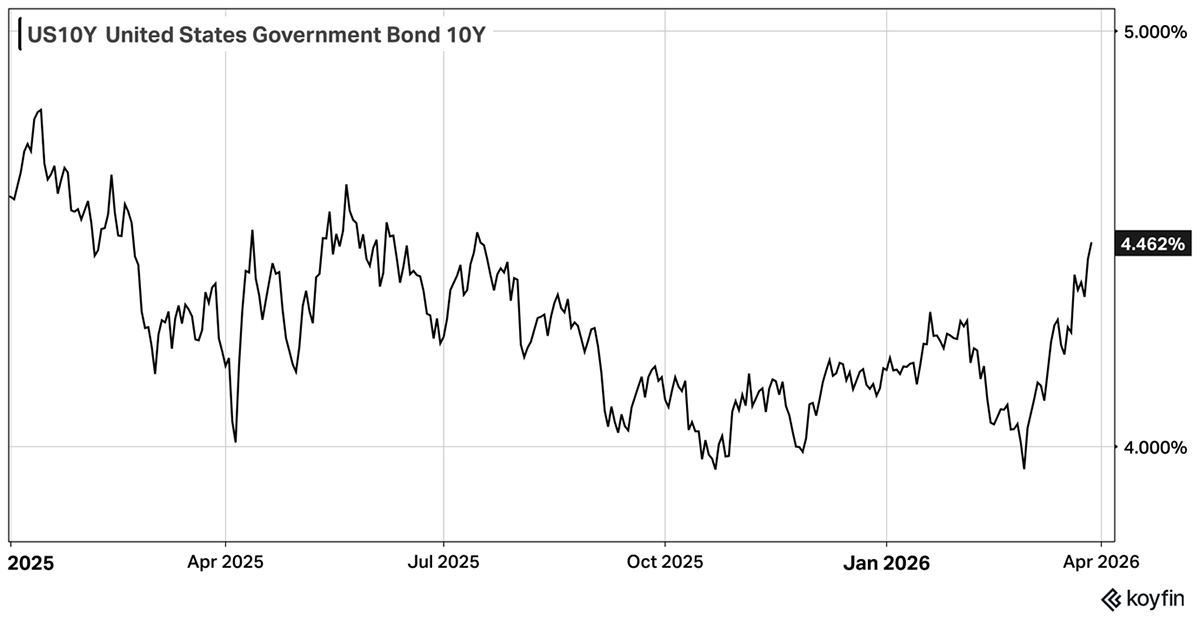

Having fallen from 4.7% to 3.9% since 1 January 2025, the yield on US government 10-year bonds has risen back towards 4.4%. Trump appears sensitive to this, as it limits government borrowing and raises the cost of mortgages.

US 10-Year Bond Yield

We are pleased with two things. Firstly, the ByteTree Quality portfolio has displayed resilience, offering a calmer ride through this storm. This is a key benefit of quality investing, and the lack of actions required is a feature of the strategy. We can be calm during crises. No positions caused us any great anxiety, and conviction remains high because of our companies’ market-leading positions, self-reinforcing growth, leading innovation, product quality, and essential nature of these companies. AI, or even war, can’t disrupt toothpaste, chocolate, or cleaning products. Whether oil prices are high or low, we still need medicines, and pioneering innovation will enable new growth drivers long into the future.

Moreover, part of our discipline is an unwillingness to overpay for quality. We wait until better valuations arrive before getting interested – as they inevitably do. Today, a growing number of great companies that we like are retreating to more reasonable price levels. The section of our investable universe that we would consider buying has therefore grown, giving us a better opportunity set going forward.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd