Emerging Quality

Emerging markets, notably Latin America, are out of the spotlight today, as the focus is on Iran. However, they are commodity powerhouses, and rising prices help drive regional growth. On top of that, their economies continue to catch up with developed markets.

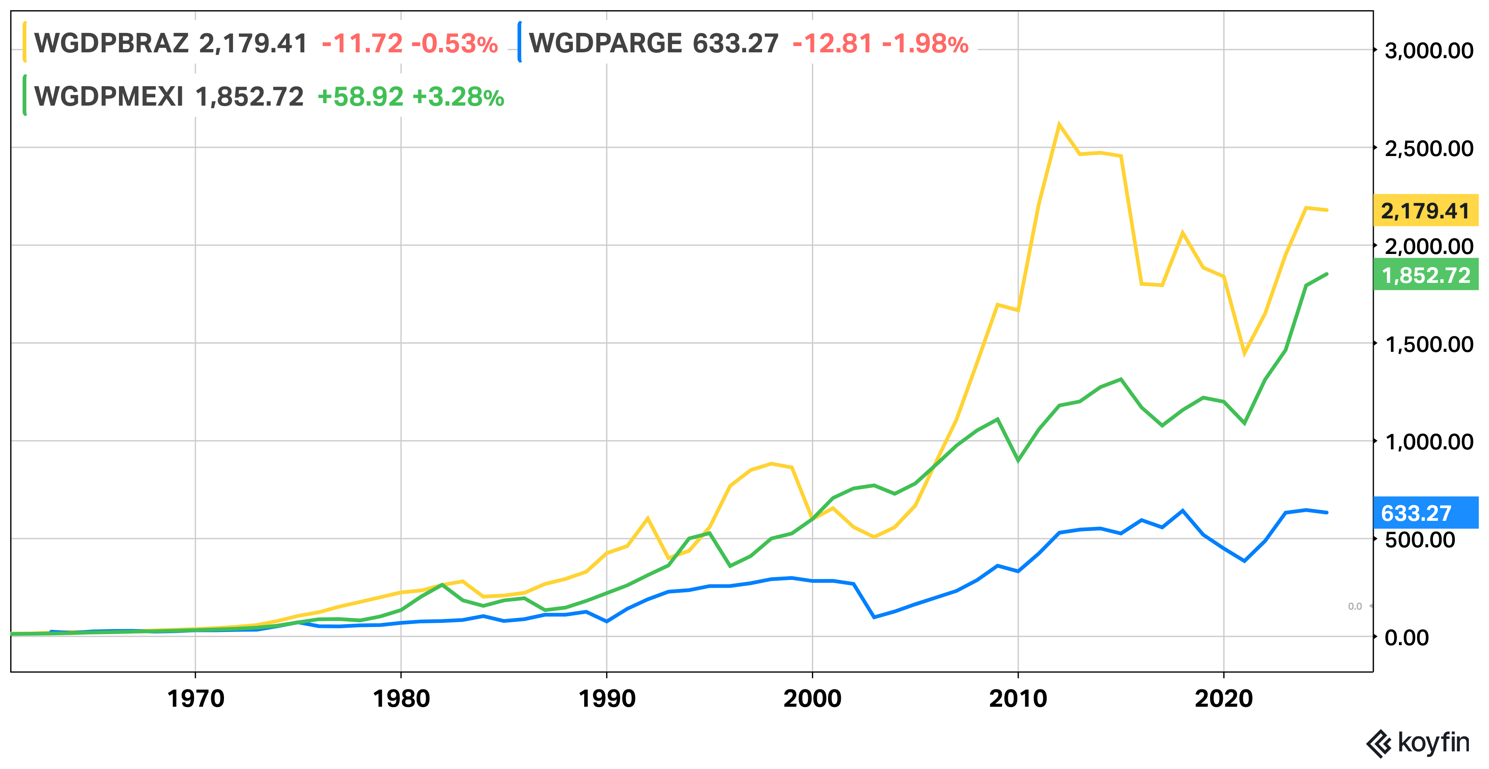

Brazil ($2.1 trillion) and Mexico ($1.7 trillion) alone contributed around 60% of Central + South America's GDP in recent data. Adding Argentina ($0.7 trillion) pushes the trio's share to approximately 70%. The population split within the three is around 60% in Brazil (215m), Mexico (130m), and Argentina (47m), which sums to about 390 million people. Together, their share of the continent’s people is 60% - these are the big three economies.

However, they are far from the wealthiest in per capita terms. At $10k per person, Brazil is outside the top five and far behind Guyana and Uruguay, which have $29k and $23k, respectively. Mexico is at $14k/person, and Argentina is at $13k. The OECD average is nearly $50k, so they have a huge amount of catching up left to do.

Their economies share some key drivers, but each has its own distinct profile. Brazil is the world’s largest exporter of soybeans, raw sugar, and coffee, but wealth is highly concentrated. As a result, Brazil has the highest income inequality in the region. Mexico’s economy benefits from large trade with the US, and is diversified across manufacturing, agriculture, and energy sectors, but has high income inequality and persistent political problems related to the unrelenting power of the drug cartels. Argentina is a fascinating case. Beset by corruption and debasement for decades, it is now in the midst of a possible turnaround under Javier Milei, who has a grip on inflation, and supports free markets. It is also a large exporter of agricultural and other commodities. Of the three, it is Argentina which has fallen behind.

GDP of Brazil (yellow), Mexico (green), Argentina (blue)

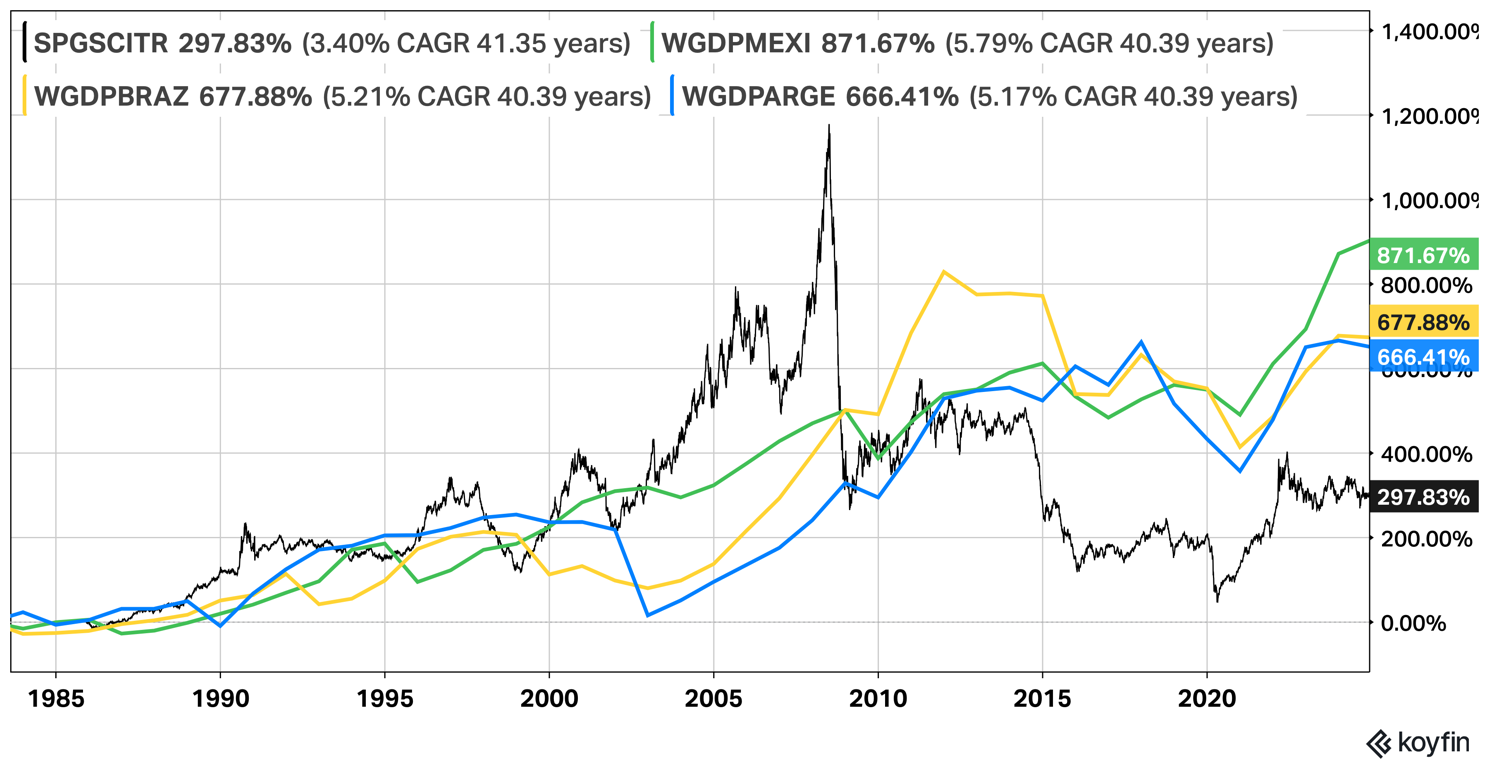

Their GDP growth is largely driven by commodity prices, given their role as major exporters. The collapse in commodity prices in the 2010s saw their economies fall. The recovery began after the pandemic, when inflation spiked once more.

GDP Growth BRA/MEX/ARG vs GSCI Commodity index (black)

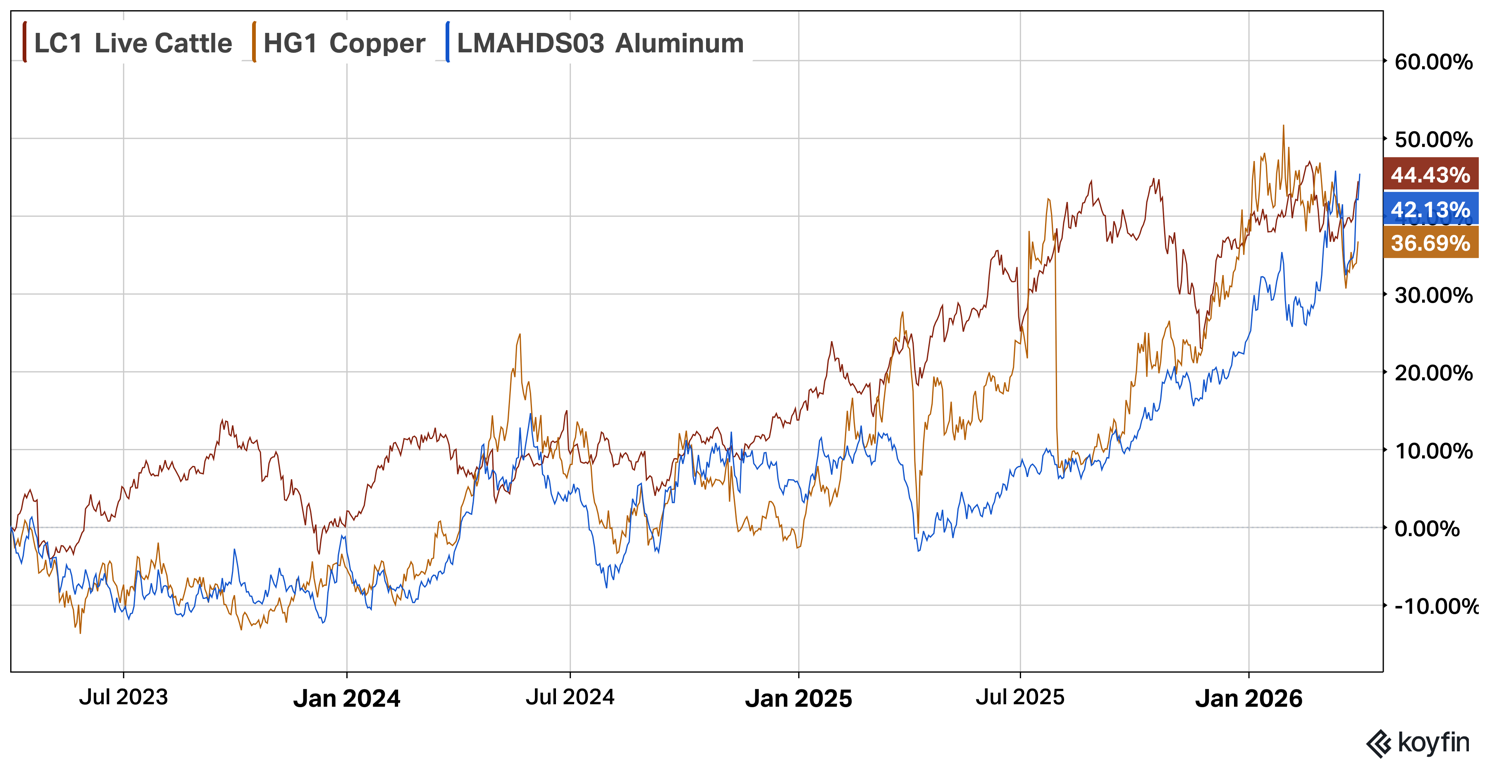

Commodities have been rising again in the last two years, most notably precious metals, copper, aluminium, and cattle. Soybeans and Corn have also stopped falling, and are up 10-15% over the past year.

Commodity Bull Market

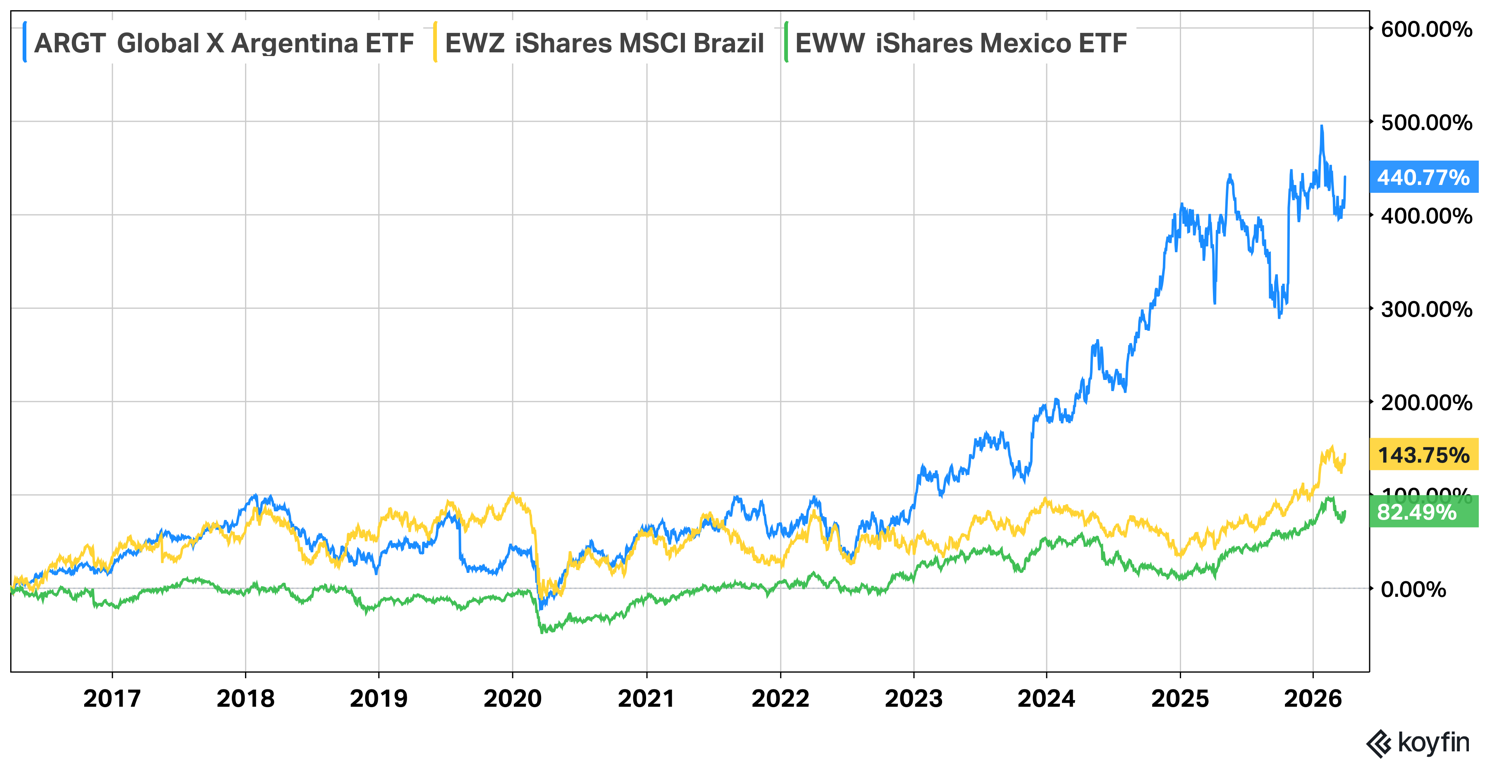

Their stock markets have responded and are rising again relative to the world index since the start of 2025. The Milei effect is visible in Argentinian equities, which have led the region.

Commodity Driven Comeback

Finally, there is Pix. Brazil’s central bank created a digital payments system in November 2020, and its adoption has been extraordinary, reaching 60% of adults in Brazil in its first year, and becoming Brazil’s most common payment mechanism by 2024. This was achieved partly through its speed and low cost, and partly through central banks mandating all large financial institutions to adopt it.

Overall, Central and Latin America are home to 600m people, and generate over $6tn in GDP. Per capita incomes are low, with lots of catching up to do, but commodity prices are rising, driving their stock markets to outperform. Political risk is above average, as are FX and commodity risk, but over a long enough time horizon, a company’s execution outweighs that. Their digital economy is growing rapidly, and socio-economic growth is accelerating.

Our next recommendation in the ByteTree Quality Portfolio, more than any other, exemplifies and is driving the catch-up in Latin American growth.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd