Venture: Crisis and Opportunities

Issue 112;

The main issue facing markets is how long the Strait of Hormuz will remain shut and how quickly normal oil production will resume. Moving the ships can happen quickly once insurance coverage resumes. But several oil facilities have been damaged or shut down, and that will take more time to return to normal. There is also the tail risk that this conflict drags on. In that scenario, equity markets feel mispriced.

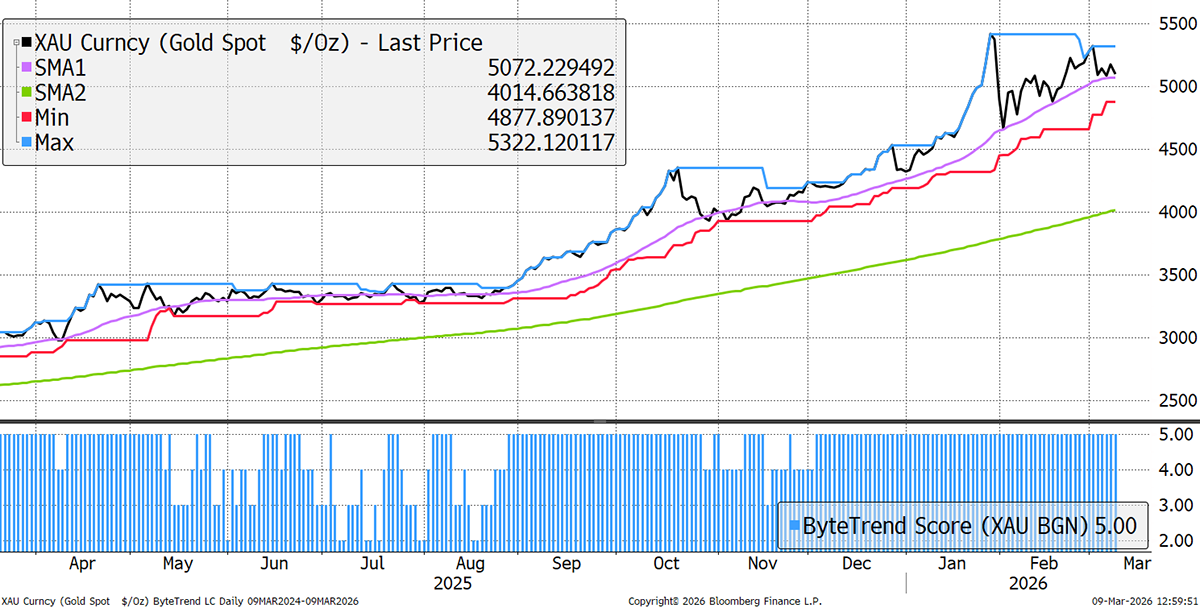

Oil is the marker, and gold is not particularly relevant to this conflict. The price is up 76% over the past year, so it has come into this with a strong bid. Had gold been flat or out of favour, I have no doubt the price would have surged since the first strike. It hasn’t moved on the disorder, but remains a monetary trade, due to longer-term forces. Gold has remained in a strong uptrend for three months.

Gold

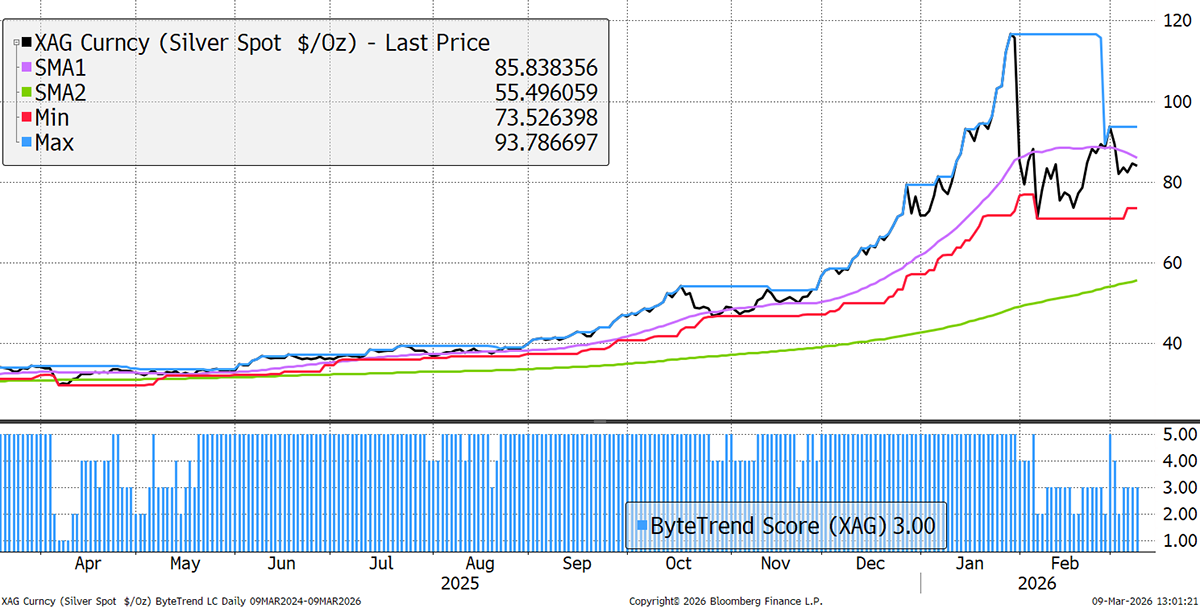

Contrast that with silver, which is up 160% over the past year. With a declining 30-day moving average, the trend is under pressure. It’s by no means bearish, but given the choice between gold and silver, I’d choose gold.

Silver

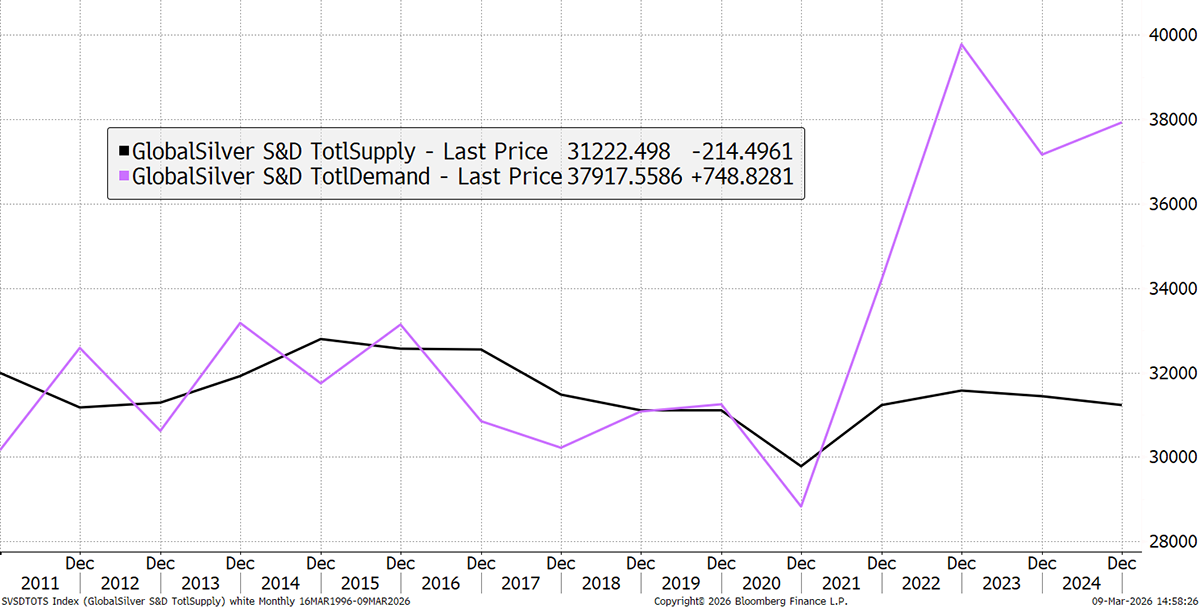

That said, silver is far from over, but it has sold off more sharply for two reasons. Firstly, it was more heavily hyped into the January peak, and secondly, it is less liquid than gold, and the weaker equivalent always gets hit harder. Perhaps silver asserts itself in the recovery. Data from Metals Focus highlights that silver supply remains soft, although the price rise will have motivated new exploration.

Silver Supply vs Demand

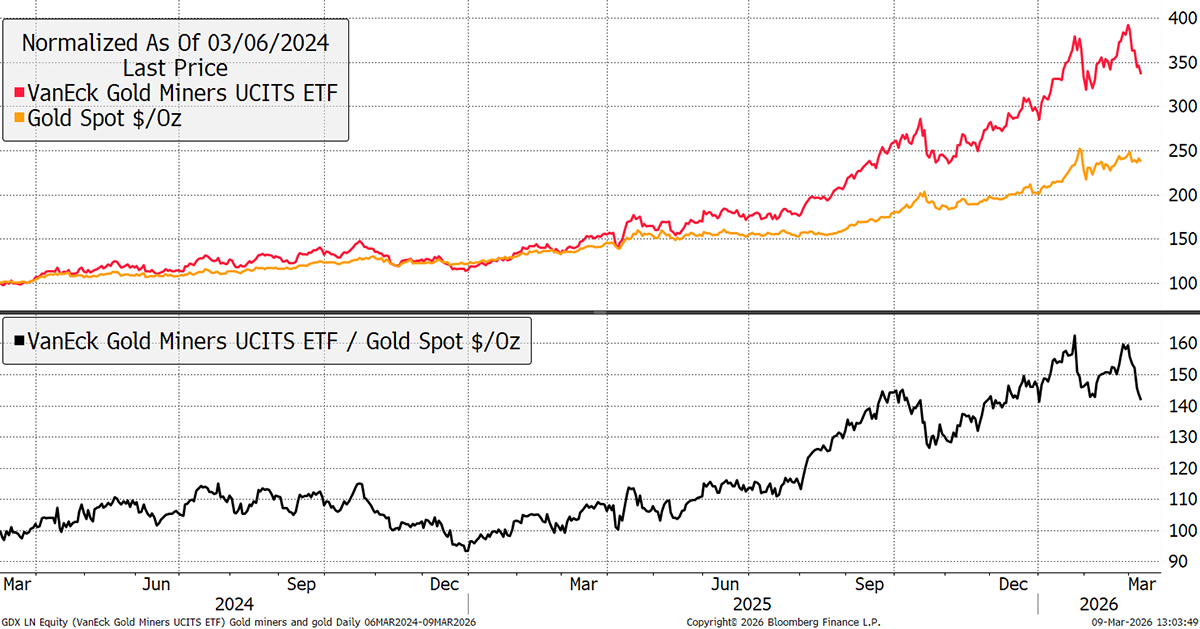

The gold (and silver) miners are lagging the metal. One reason is that higher energy prices impact profits, but as always in a crisis, gold equities turn into just equities and sell off along with everything else. In the subsequent recovery, I would expect gold equities to regain lost ground, alongside silver.

Gold and Miners

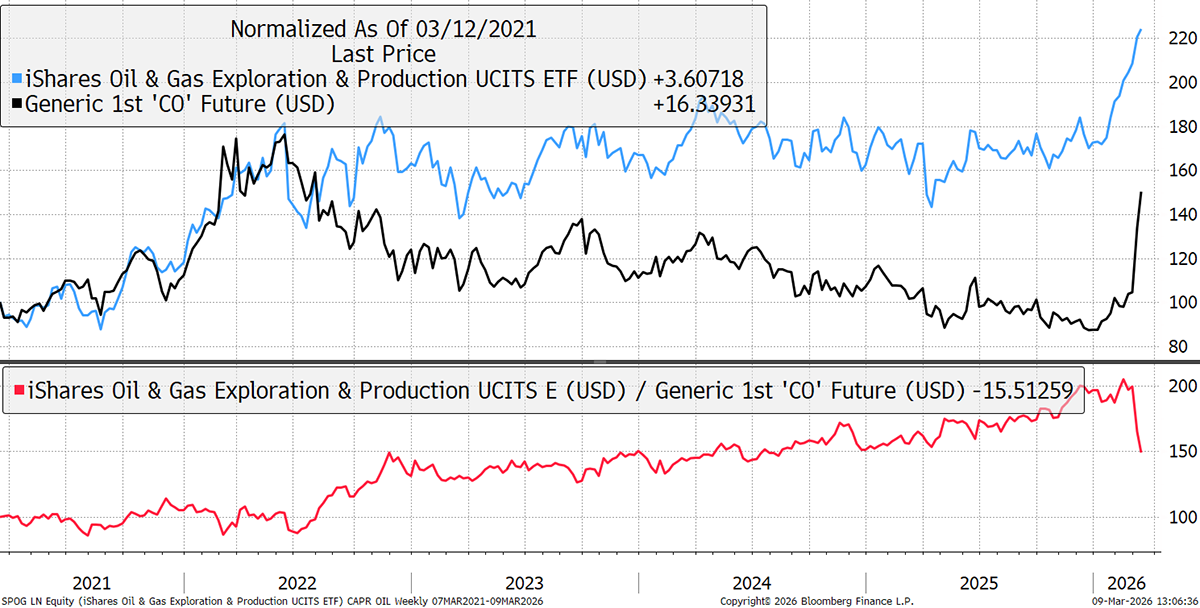

It seems late to be chasing more oil stocks. The price has spiked, but again, oil stocks are a long way behind the oil price, lagging by 50% over the past week. If oil stays high over the long term, this gap will close, but you’d need to have a strong handle on the unknown events ahead to take that risk. I have no intention of selling our oil stocks, but at the same time, there is no sense in adding more unless I can find value.

Oil and Oil Stocks

Since the strikes on Iran, there are few other areas of strength, but technology stands out, especially software. That comes after a sharp fall since October, coinciding with crypto. The physical world, and hard assets in particular, have been in vogue up until the war, and that has now turned.

Software and Bitcoin

Of the 113 stocks in the IGV ETF, half are down 40% to 70%, which will provide rich opportunities at some point. There are others around the world as well. I am also interested in crypto and crypto stocks. Despite my optimism, it is hard to say whether the low is in, but progress in the sector, especially around stablecoins, exchanges, and tokenization, has been robust. I believe it will come out of this dip stronger than ever, and opportunities will arise in this space.

In the meantime, rates have risen, which has kept a lid on defensive stocks and real estate, and caused concern across the board.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd