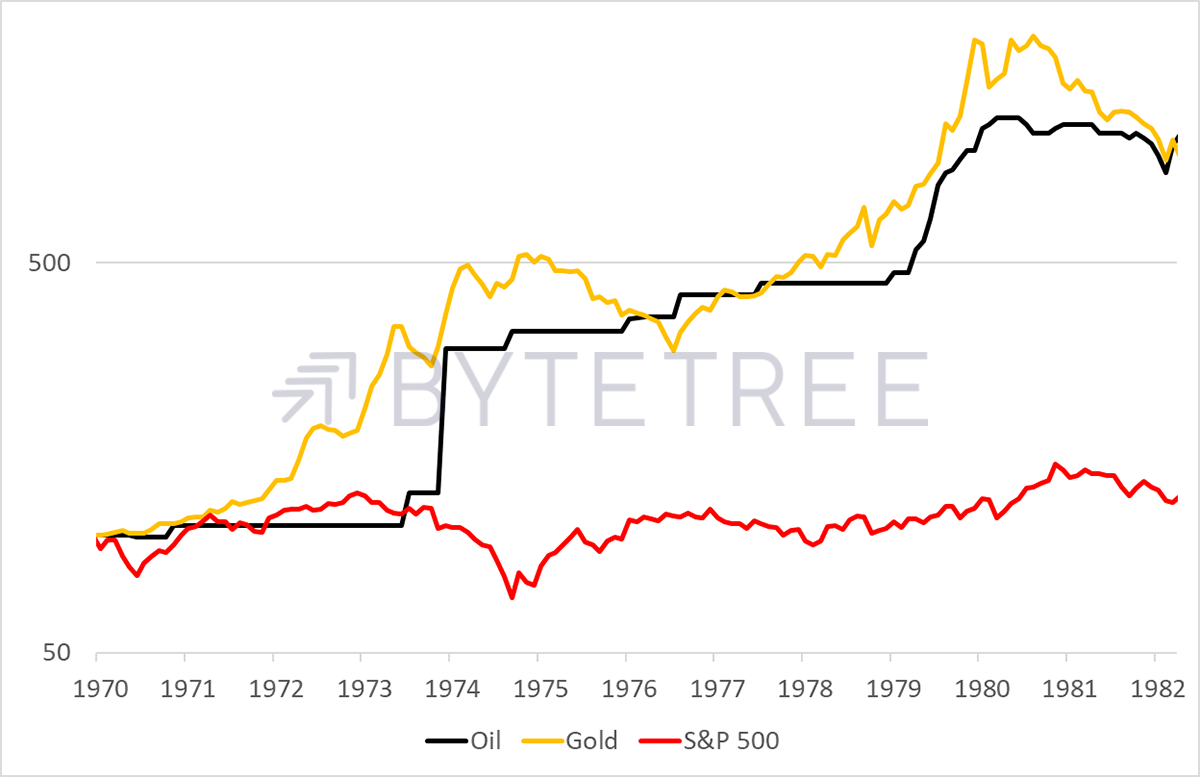

Gold and Oil in the 1970s

Atlas Pulse Gold Report - Issue 112;

These are times to think differently. An oil shock might be bad for gold in the short term during liquidation, but it is most likely supportive over the medium and long term. Investors need to think differently and should treat the 60/40 portfolio with caution.

In gold terms, who knew that the highest oil price on record occurred in 2005? Gold was still in the $400s, while oil traded above $60. The cheapest came during the pandemic, when oil was virtually free at one point.

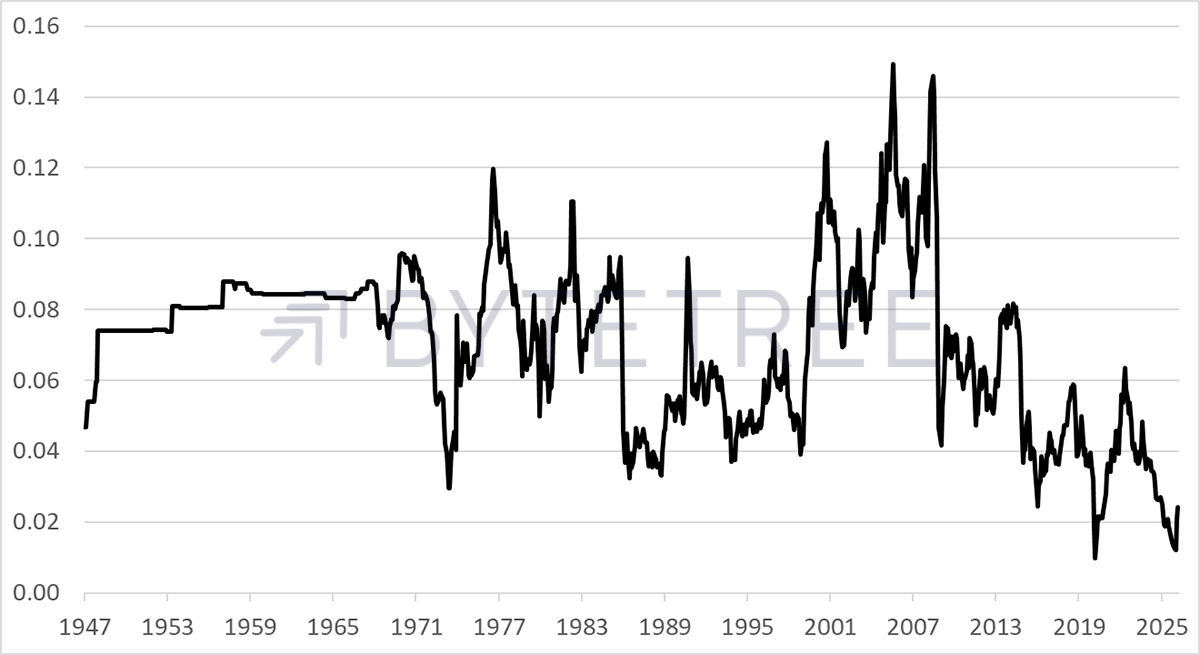

The Oil Price in Gold (oz)

For those thinking that $110 per barrel for Brent crude is too high, think again. A barrel still only buys you 0.24 ounces of gold when the eight-decade average has been three times that.

High oil prices broke the stockmarket in 1974, 1982, and 2008. The 2008 financial crisis was a credit event combined with an oil shock, and the outcome wasn’t pretty. But that still lives in many investors’ minds. For the young investors who missed it, it is still readily available on the charts for inspection. In contrast, the shock in the 1970s isn’t. Not only will few active investors remember it as they’d be 85 or more today, but no modern charting systems carry the data.

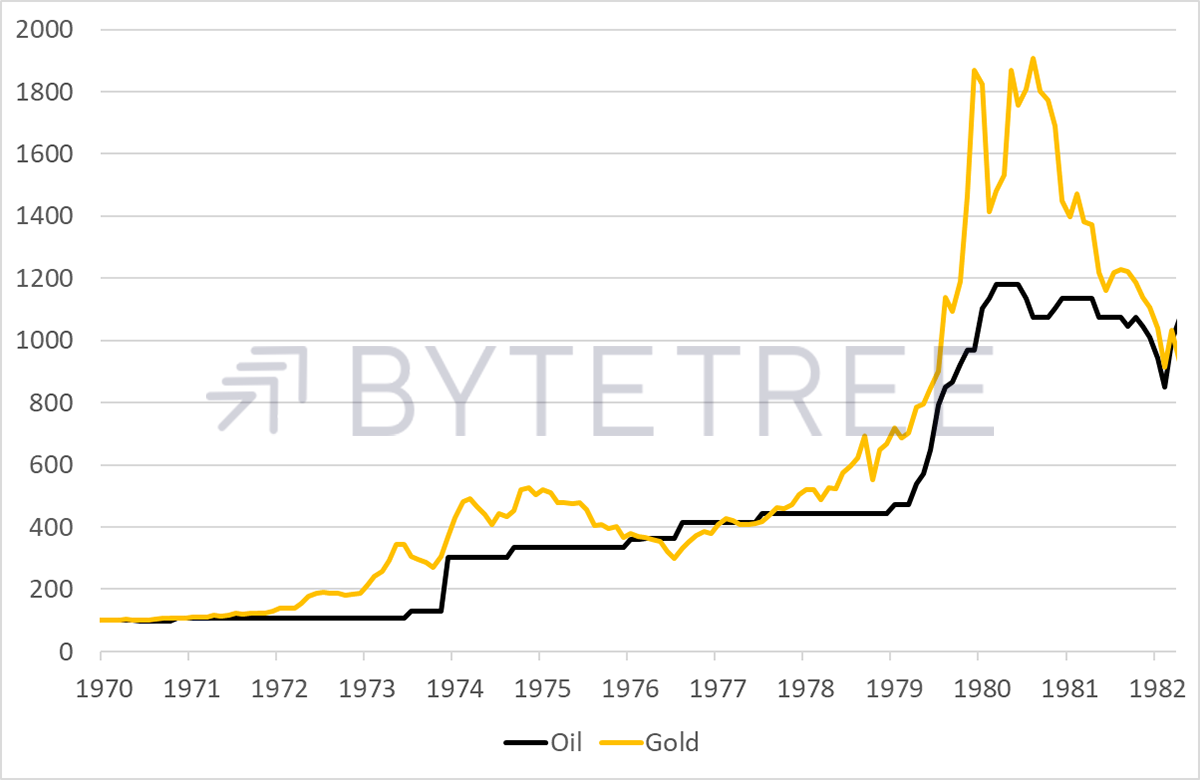

I’ve been doing some asset price archaeology to unveil that era. Between 1970 and 1982, gold and oil rose 10-fold in nominal terms, with gold managing much more in 1980.

Gold and Oil in the 1970s

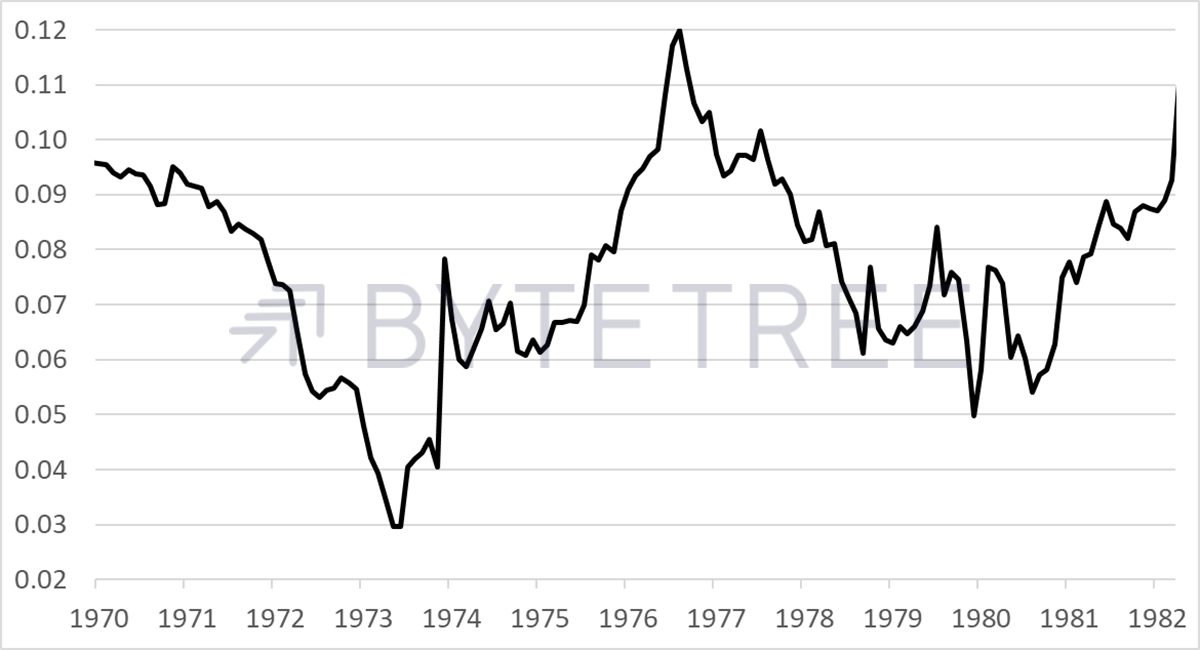

Zooming in on the oil price in gold during the 1970s is mind-blowing. Although both assets did well, they took turns with huge relative moves. Oil lagged gold by 70% until the oil shock, when it surged 4x. The next dip was smaller, only 50%, but it then doubled in 1982.

The Oil Price in Gold (oz) – 1970 to 1982

While oil and gold both ended up in the same place, holding both was much better than holding one. The low correlation would have led to rebalancing transactions and significant outperformance as a result. I was too young at the time, but had I been an active investor, I would like to think that I would have been promoting a strategy blending gold and oil, ticker GOIL.

I now show oil and gold with the S&P 500 in nominal terms, using a log scale so you can actually see what equities did at the time.

Gold, Oil, and the S&P500 in the 1970s

The S&P 500 rose by 52% over the 12-year period when oil and gold rose 10x. Then consider inflation of 159% over the period, meaning that a dollar lost 61.4% of its purchasing power. That means that equity real returns saw a 42% drop in capital terms, but a 4% gain including dividends. Still, 4% over 12 years isn’t much, and that’s in total, not the annualised figure.

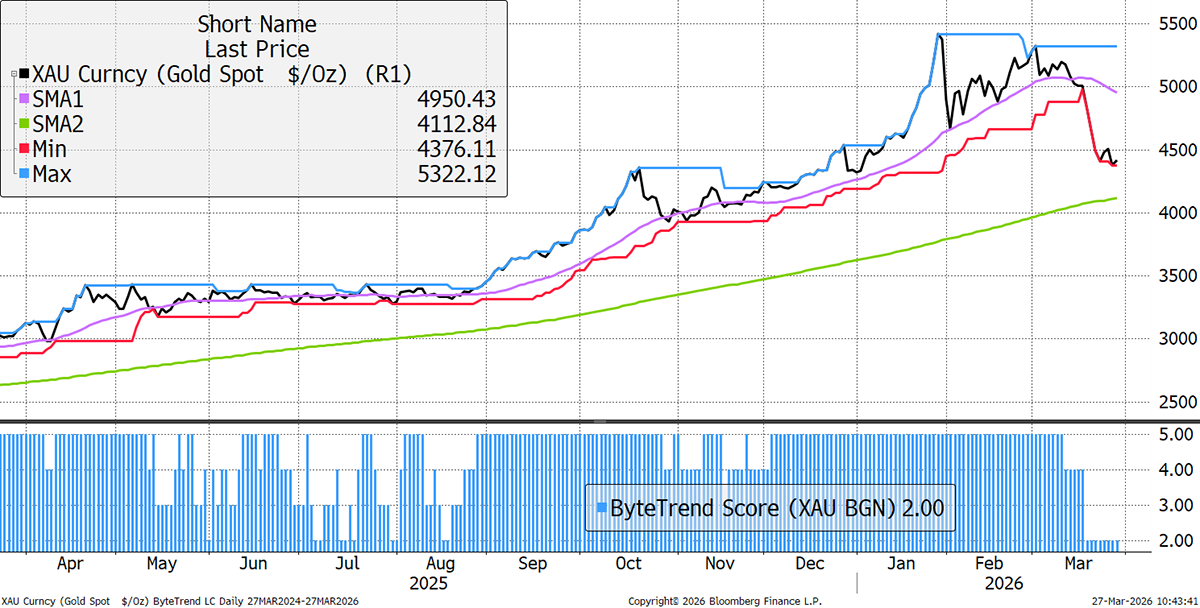

Since Iran, oil is up while gold is down. The ByteTrend Daily Score for gold has dropped to a 2 as the short-term trend has broken.

Gold - Daily

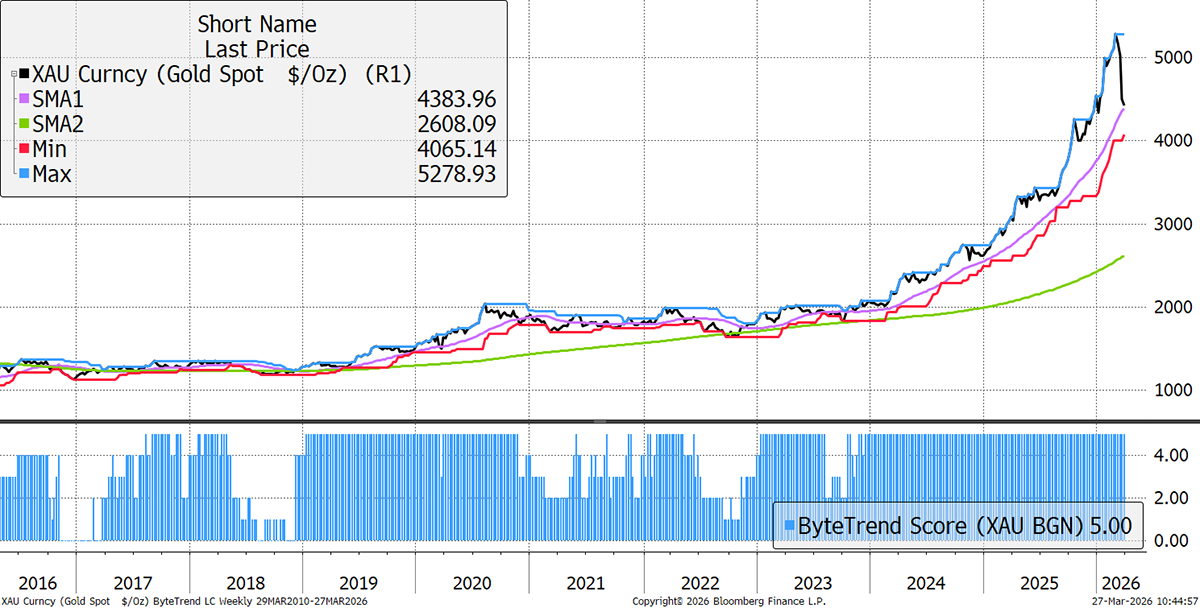

Yet using the ByteTrend Weekly Score, gold remains a 5. It is remarkable how high and far above trend gold was. That was highlighted in last month’s Atlas Pulse, “Gold’s Risk Rises”. Sometimes it is a pity to be right and then not do enough about it.

Gold - Weekly

In March, gold is down 17%. Of that, 7% can be attributed to the rise in real yields, and the bond market has been a casualty of war. The dollar has risen by 2%, but more importantly, there have also been reported gold sales from several central banks, including Turkey, Russia, Bulgaria, and Kazakhstan. Others too, no doubt.

Then there’s the speculators and investors (same thing perhaps?) who have dumped 2.6 million ounces of gold through ETF sales. It soon adds up.

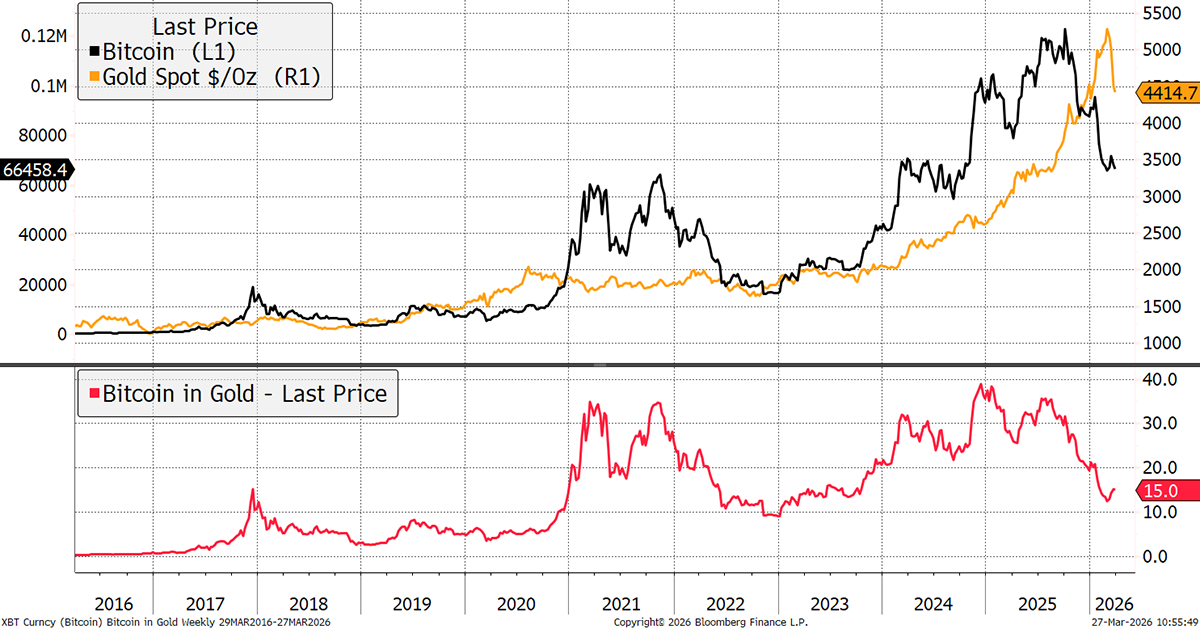

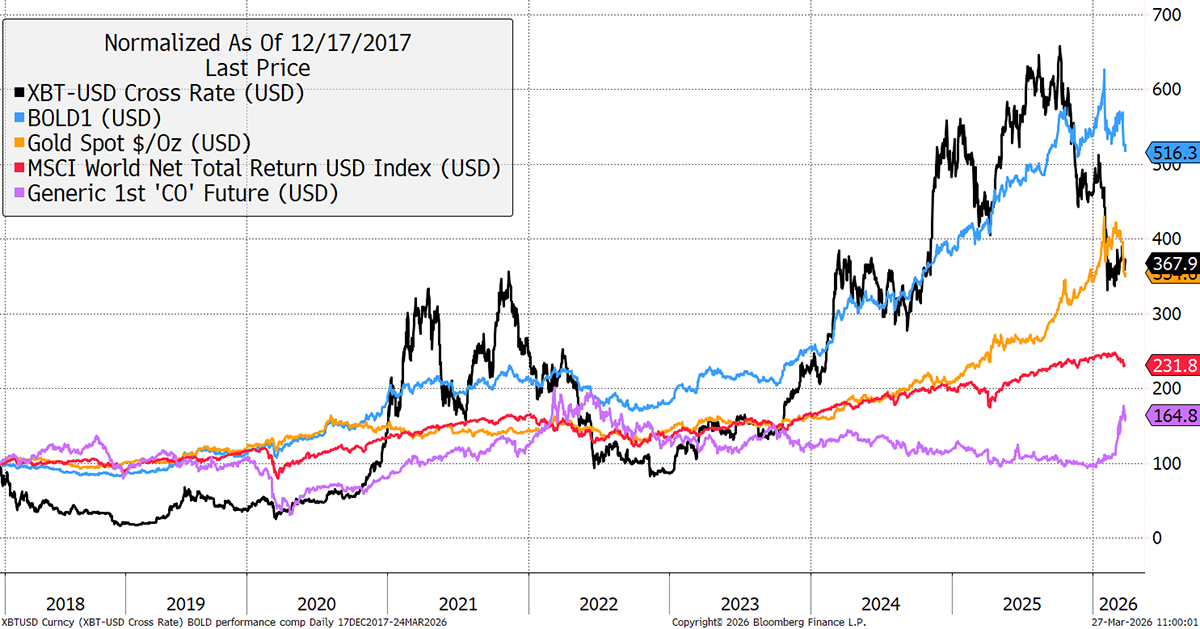

A surprise to some is that Bitcoin is one of the few assets, other than oil, that has held up in March. As a speculative asset, it is perhaps surprising that it has achieved that, but it is still heavily underweighted by mainstream investors. This is the long-term bull case: no one owns Bitcoin.

Bitcoin and Gold

This is one of those times I dream that BOLD contained oil. BOIL? BOGO? BOGCoin? Funny names are welcome, but although I would have supported performance this year, it would have been a detractor over the longer term. I’ll keep BOLD as it is with Bitcoin and Gold.

Gold’s and Bitcoin’s divergent performance during this oil shock merits further discussion and context. To provide it, I brought ByteTree board member and Bitcoin and General fund manager, Charlie Erith, on for a discussion. Watch the full conversation here.

Bitcoin, Gold, BOLD, and Stocks

Bitcoin wasn’t around in the 1970s, but I believe it would perform much better than equities in a similar environment. It will probably outperform gold from here because it is cheap, and decentralised assets become attractive during times of stress. But I doubt it beats oil during an oil shock.

For product details on the 21Shares Bitcoin Gold ETP (BOLD), please visit the 21Shares website. For strategy information, please visit BOLDETF.com.

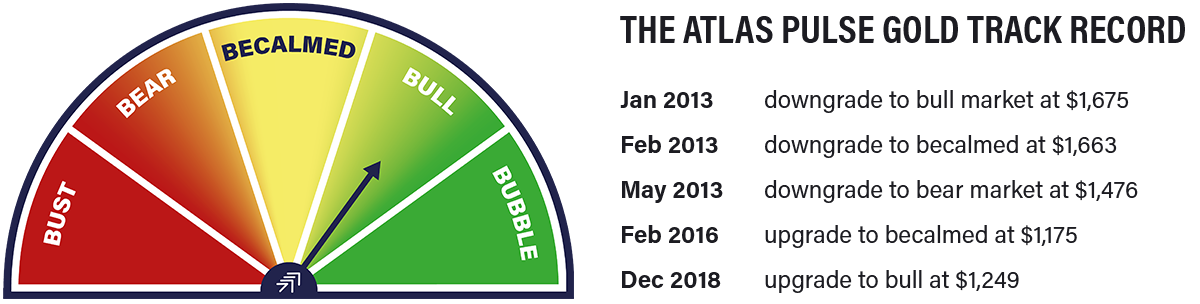

Summary

These are times to think differently. An oil shock might be bad for gold in the short term during liquidation, but it is most likely supportive over the medium and long term. Investors need to think differently and should treat the 60/40 portfolio with caution.

Thank you for reading Atlas Pulse. The Gold Dial remains on Bull Market.

Charlie Morris is the Founder and Editor of the Atlas Pulse Gold Report, established in 2012. His pioneering gold valuation model, developed in 2012, was published by the London Bullion Market Association (LBMA) and the World Gold Council (WGC). It is widely regarded as a major contribution to understanding the behaviour of the gold price.

Please email charlie.morris@bytetree.com with your thoughts.