Evaluating Catastrophic Risk

The California wildfires of 2025 were one of the largest catastrophe insurance events in history. But remarkably, from 2019, insurance coverage for homes in the affected region had been falling. Why? Regulation.

As inflation and natural catastrophes drove increased risk and higher prices, insurers responded naturally by raising premiums. After all, as they say in the insurance industry, disasters drive premiums. However, regulators placed limits on this, and the response was predictable – insurers pulled back, refusing to cover risks at prices that didn’t compensate them.

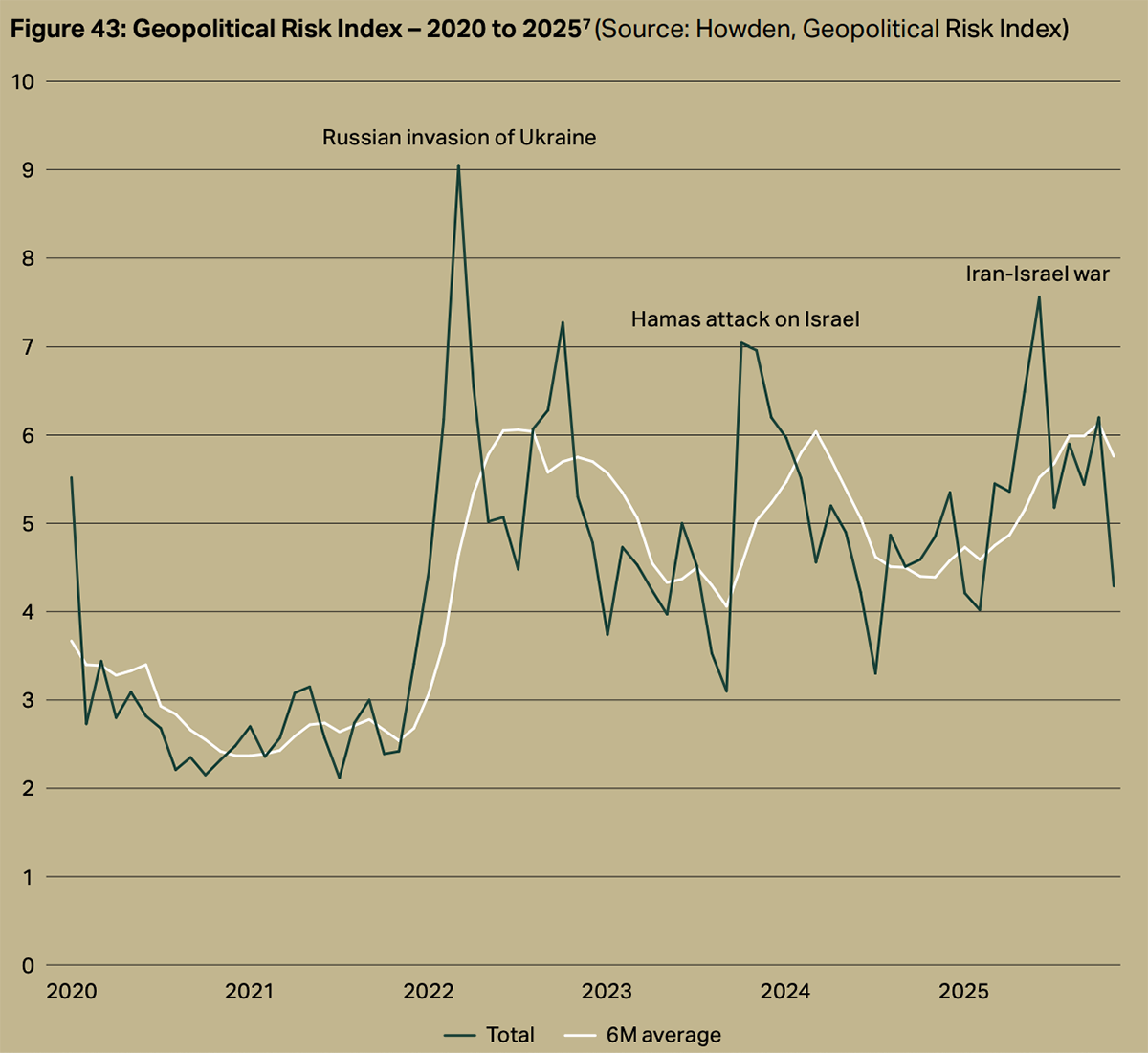

Risks Rising

This is happening amid high global risks. Conflict, inflation, politics, climate, trade, and of course, AI, are driving the proliferation of risk. Risk used to be (like the band) earth, wind, and fire, along with asbestos and oil spills. Now, with the increasing knowledge and interconnection of human systems, this is expanding to include cyber, physical and mental health, food systems, microplastics, pathogens, fungi, and the digital world. All carry potentially systemic risk.

Climate change is a secular growth driver for catastrophe insurance, increasing demand, but it also makes accurately pricing risk harder (as old models for natural catastrophes become outdated). This risks losses on products sold under the old models, but the edge for sophisticated players in the sector could get wider.

Growing Pains

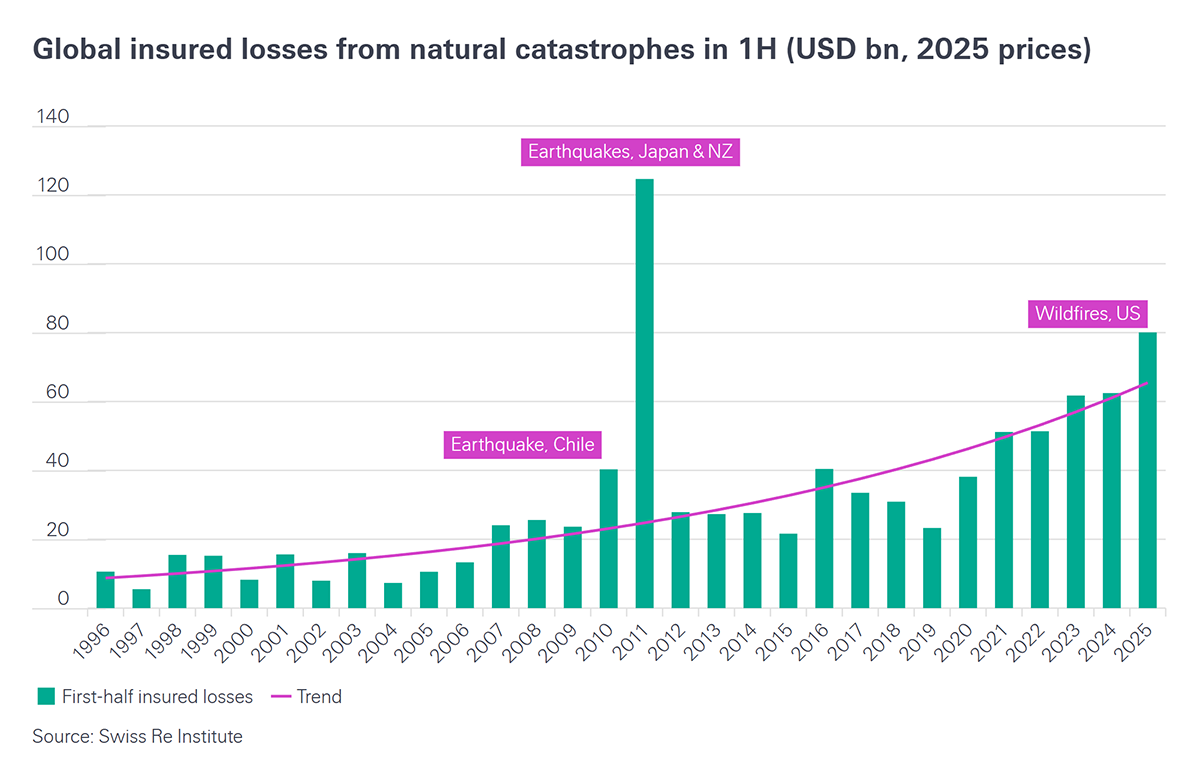

According to data from Munich Re,

“Natural disasters caused significant losses worldwide in 2025. All in all, damage amounting to some US$ 224bn was incurred, of which insurers covered around US$ 108bn. This means that 2025 joins a growing list of years with insured losses exceeding the US$ 100bn mark.”

Insurers trying to offer protection against these things are themselves exposed and seek to insure their own risk exposure. For this, they turn to specialist reinsurers.

What Is Reinsurance?

Global giant Swiss Re says,

“In essence, reinsurance is insurance for insurance companies. Only by sharing some of their risk with reinsurers it is possible for primary insurers to offer cover against the key risks we face today and to keep prices at affordable levels… Risks are transferred from individuals and companies, through primary insurers, to the reinsurer.”

The increasing severity and frequency of major disasters, including natural catastrophes and manmade events, has shed light on the role that reinsurers play as shock absorbers for the global economy. By helping to mitigate the potential losses that could result from risks such as major new construction projects or breakthrough new technologies, reinsurers also fulfil an important function as enablers of innovation.”

Their large investment portfolios also provide capital to the global economy, enabling growth. Their clients are insurers with exposure to volatile lines of business or natural catastrophe risks.

The American market is the wealthiest, and because of hurricane season and other threats, it is vulnerable to disasters. Many emerging markets have underdeveloped insurance markets but are equally, or even more, physically exposed. Data is essential for accurate risk pricing, yet there is a widespread lack of it in many developing nations.

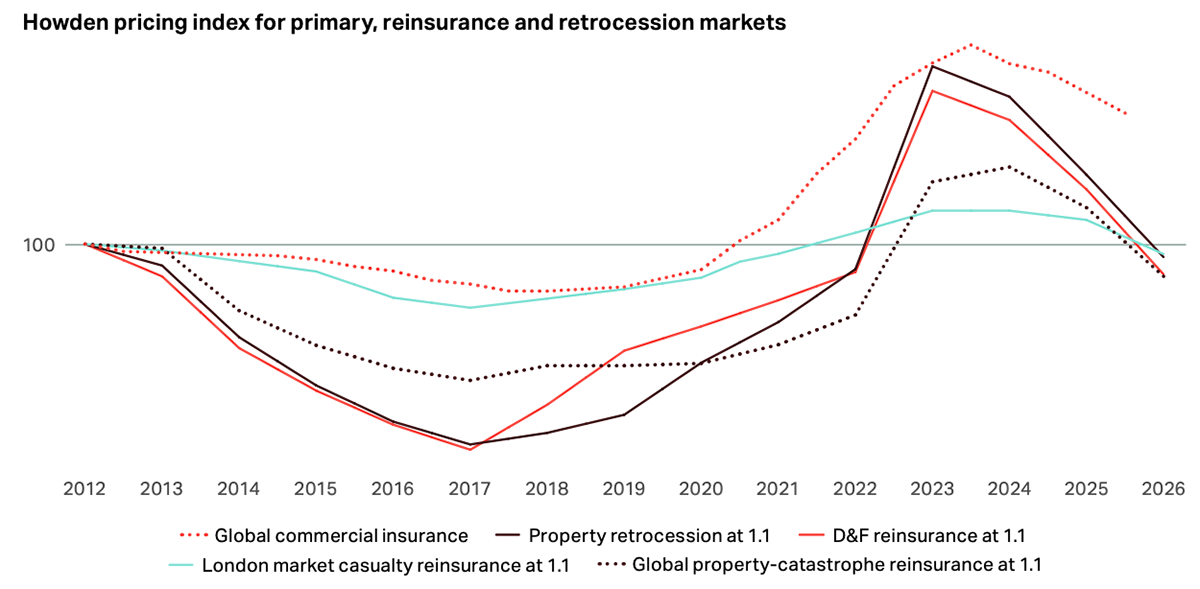

The reinsurance market has enjoyed some of the best market conditions for over 20 years. Catastrophe reinsurance pricing was broadly flat in 2024, which followed an uptick of 25% in 2022 and 37% in 2023. After two years of strong returns, catastrophe pricing reduced by 5-15% in 2025. Pricing levels are nonetheless still at levels not seen since the mid-1990s.

Quality Credentials

The non-life insurance industry in particular offers valuable characteristics to investors. This is what Nick Martin of the Polar Capital Insurance fund calls “the oil that greases the wheels of the global economy”. Ships don’t sail, planes don’t fly, and your Amazon package doesn’t arrive without it. Buffett has famously been a long-term admirer of its value to investors, not least for its defensive credentials.

According to the Polar Capital Insurance team,

“A key attraction of the [non-life insurance] sector is that the driver of book value growth for the best companies is underwriting profits. This profit stream tends to be largely disconnected from the broader economy and financial markets. Insurance is mostly a compulsory purchase, often required by law, and therefore the industry exhibits robust demand characteristics and has historically been defensive in challenging economic times.”

The sector has benefitted in recent years, as the premiums they receive from clients (the “float”) are invested until payouts are due. This is typically focused on highly liquid government securities, prioritising safety. This allows the firm to earn a return in the interim, and as rates have risen since 2021, the return earned has gone from 1-2% to 4-5%, a dramatic improvement. Placed on top of continued underwriting profits, this has driven rapid growth in free cash flow (as the extra earnings required no extra investment).

In terms of inflation, insurers benefit from the consequent higher rates as their investment income grows. Also, premiums have generally risen faster than GDP or inflation. Speciality insurance (for unique/bespoke business risks) is benefiting most at the moment, as risk becomes more complex.

Insurance follows a capital cycle. In “hard markets”, capital is scarce, and insurance can therefore charge high prices to cover its clients’ risks. In “soft markets”, capital is plentiful, and insurers compete for business by lowering prices and increasing volumes, but reducing profitability.

The catastrophe reinsurance market hardened in the early 2020s, peaking in 2024. It has now declined for two years running. It is a “hard market softening” environment. Sustained profitability gives competing firms more capital to deploy, which drives the cyclicality. High prices lead to profits, which are deployed, lowering prices. Overall, it is now a $500 billion market, up 8% from year-end 2024.

The Capital Cycle in Insurance

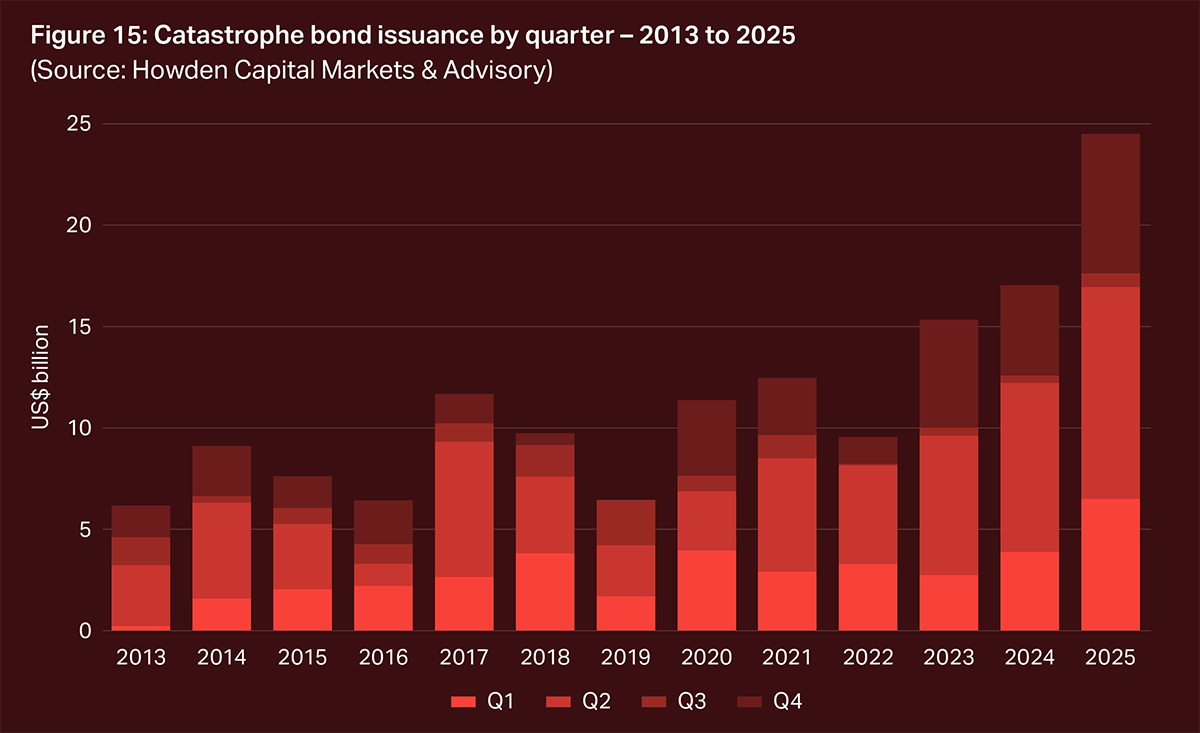

Volumes in catastrophe bond issuance grew healthily last year, and broke records, reaching levels nearly 45% higher than in 2024 at $24.5 billion. However, high volumes are often associated with weaker pricing, as more money chases fewer deals.

Record Catastrophe Bond Sales

In summary, the growing complexity and severity of risk are increasing the broad demand for insurance. While cyclical in the short term, insurance is a long-term growth story with a clear history of resilience during times of market stress, as demand for it is relatively consistent, in good times and bad. This is also true of reinsurance. More complex markets, like catastrophe and speciality lines, are less competitive, resulting in higher margins. The market for these was at its best in 2024 but has weakened slightly in the last two years. However, high interest rates have supported the cash flows and share prices of the companies involved.

Our next recommendation is the market leader in this area of the insurance market. Defensive, high margin, and with a long history of outperforming the market in times of stress, it is a natural fit for the ByteTree Quality strategy.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd