Our First Ten Quality Stocks

Earlier this year, we saw the opportunity in quality equities, as they were increasingly out of favour. We started planning to launch a research service dedicated to identifying and building a portfolio of high-quality companies at knock-down valuations. Then in the summer, we launched ByteTree Quality, and here’s what we wrote at the time:

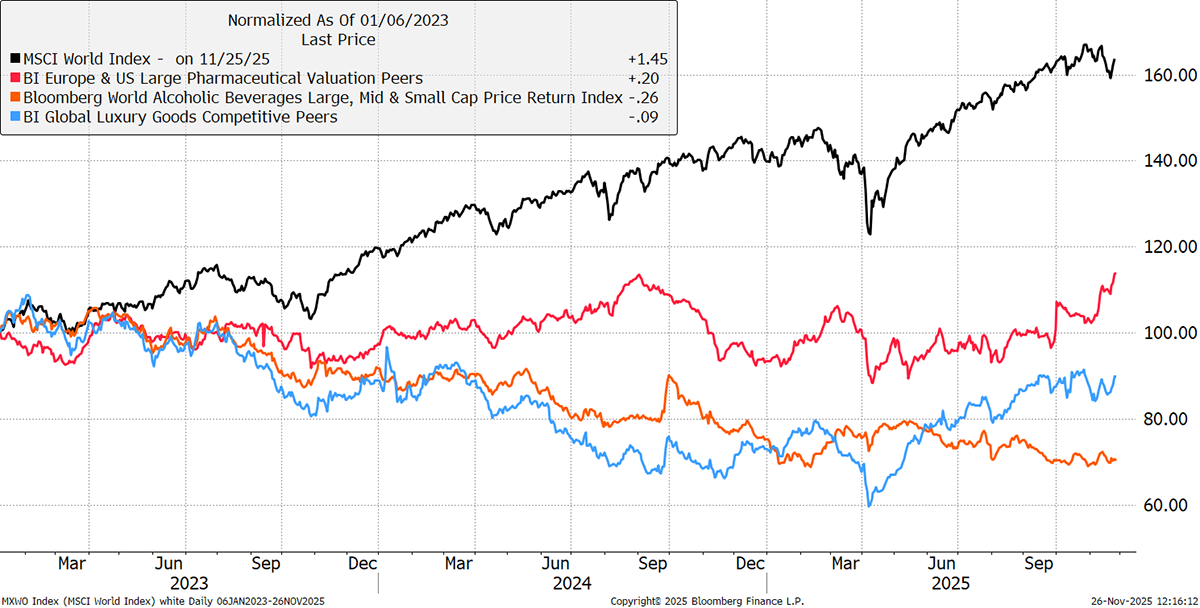

“While there has been a generational surge in what might be described as quality growth, based around technology, quality defensives are on sale. That can be shown since the interest rate hikes in 2022, whereby the world index has recovered strongly, while these key brands have slumped. The companies haven’t changed, but in several cases, their share prices are back into attractive territory.

Alcohol, Luxury, and Pharmaceuticals versus the World

The time to begin this journey is now, because so many quality companies are being derated as they have been crowded out by the big technology companies. We saw what happened the last time this happened in 1999. Technology stocks fell back to earth, while quality stocks, which were trading at bargain prices, went on to beat the market for years to come. Our timing feels right.”

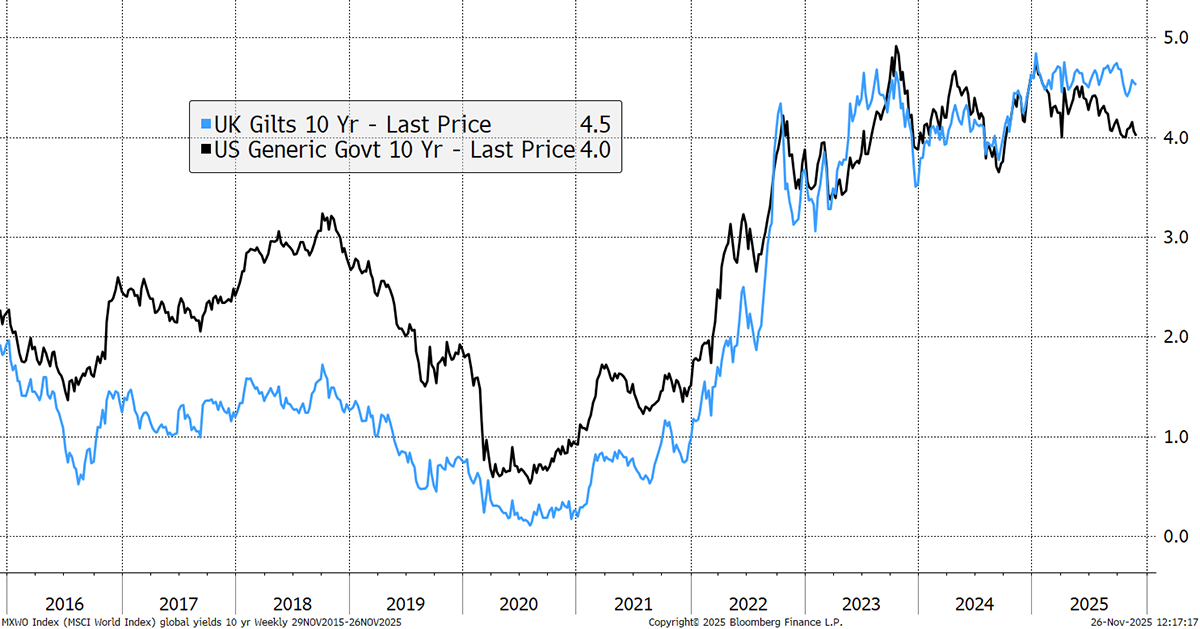

Three months on, the rotation has begun. Firstly, bond yields are coming down in the UK (blue) and, especially, in the US (black). This helps quality stocks, whose predictability and dividends make them attractive for similar reasons to bonds. High bond yields are more certain than quality stock dividends, but falling yields make them more attractive again, especially when quality dividend yields are above their historic average because of falls in the share price, as they currently are.

Bond Yields Are Falling

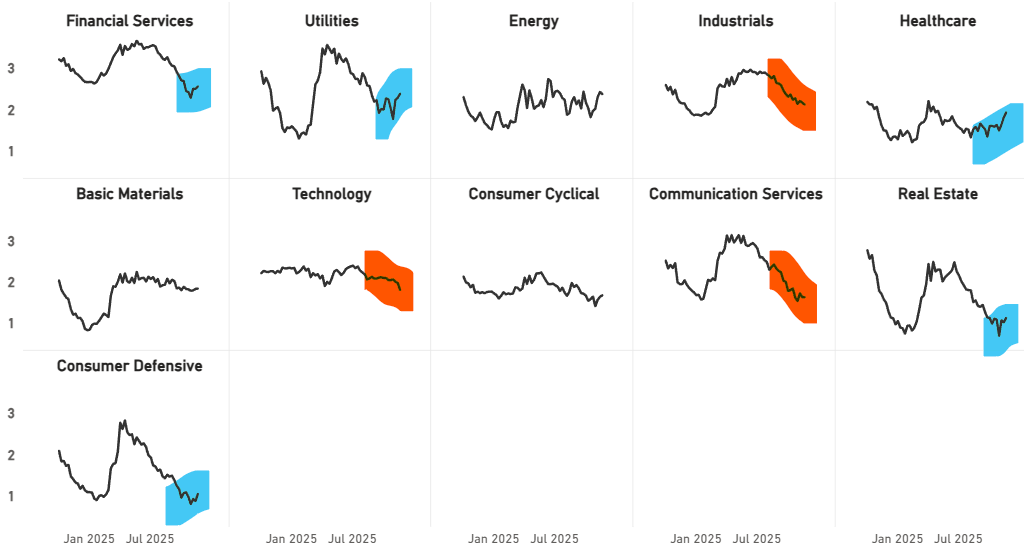

Secondly, low volatility stocks are showing great resilience as speculative high volatility stocks pull back after their rampant summer run. The last time this occurred was in late 2021, which was followed by a broader bear market in global stocks.

The Tortoise and the Hare

This is also visible in our Global Trends data, which shows high volatility stocks around the world weakening and low volatility stocks strengthening, relative to the World Index.

Most notably, healthcare has performed well over the last month, while technology has been the weakest sector in recent weeks. Nvidia is down more than 15% from its recent peak, and the credit risk of various AI-focused companies is shooting higher as the bond markets lose a bit of faith. Other defensive sectors, such as consumer defensives and utilities, are also doing well, while real estate benefits from lower rates too.

Taken together, we can see falling bond yields supporting low volatility, high-quality defensive stocks. This is where we said things were likely to go, and the first steps towards building the ByteTree Quality portfolio have been in this area.

Quality investing is about steadily compounding your wealth over the long term, while sleeping well at night. Our service cuts through 1000s of stocks to pick the best select few, while doing all the analysis and valuation for you, helping you deeply understand the stocks you are investing in.

Ten Down, 15 To Go

Our first note on Diageo was publicly available, and since then, we have recommended nine more to reach ten stocks in the portfolio. Across health tech, pharmaceuticals, cleaning products, top global brands, healthy snacks, unhealthy snacks, spirits, and cigarettes, we’ve already achieved wide diversification. We plan to have around 24 stocks by springtime next year.

We already have the company with the greatest impact on global healthcare access, a whisky maker born two centuries ago in the Scottish highlands, the most exciting drug development platform in a fast-growing new field, the oldest and largest global fermentation specialist, the market leader in a high-margin healthcare product niche, and one of the most resilient stocks of the last three bear markets. Together they form a high-margin, competitively dominant, globally diversified portfolio of essential, resilient products.

- The portfolio has an average Return on Invested Capital of 16%. You can read our deep dive on this key metric on our Free Resources page.

- The average volatility of the stocks is 23%, but in combination, that will be lower as their movements cancel each other out.

- Dividend per share growth has been 4% over the last seven years, while the dividend yield of the portfolio is also 4%. This compares to 1.5% for the World index.

- Free cash flow has grown even faster, on average at 5%, and the average cash flow to EV yield (an important valuation metric) is cheap at 6%, compared to 3% for the World Index (higher is cheaper).

That marks a good start, but we are adding more all the time. We’ve picked up the pace in November as the market conditions are favourable for quality to outperform. Now is the time to buy quality.

Second Issue: Unlocked

Our first note on Diageo was made free for all. This week, we removed the paywall from our second note:

We built this service because we saw the best companies trading at attractive prices, underperforming in an increasingly concentrated and speculative market. These factors are now beginning to turn back in favour of our strategy, putting us in a good position as we build the portfolio into 2026.

Thank you to our early clients for showing faith in our analysis, and we hope you are enjoying the service so far.

Many thanks,

Charlie Morris & Kit Winder

ByteTree Quality

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd