Trades in Whisky;

Georgia is often described as the Switzerland of the Caucasus, and with Russia on its borders, a position of neutrality is key. It has enjoyed strong growth of around 6% in recent years as it has embraced a market economy. The population is 3.7 million, inflation is 2.2%, and the currency (Lari) is stable.

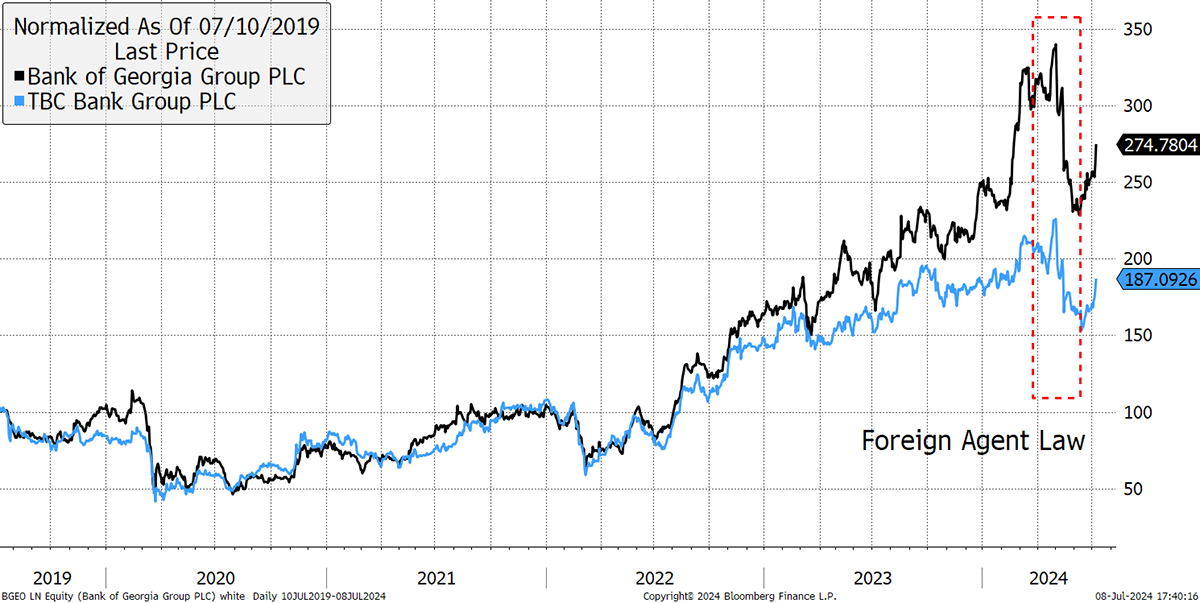

There is a basic stockmarket, but it lacks scale. As a result, there are three Georgian companies listed on the London Stock Exchange: TBC Bank (TBCG), the Bank of Georgia (BGEO), and Georgia Capital (CGEO), which owns a 19.81% stake in the Bank of Georgia. These banks are deemed to be well managed, offer good value in a growth market.

There has been some fear since the war in Ukraine, but that seems to have passed. More recently, there has been some pushback from the European Union over the newly introduced law that targets “foreign agents”, i.e. any organisation that receives more than 20% of funding from abroad. Basically, it means NGOs become known as “foreign agents”, and neither the EU nor the NGOs or the media like it. The counter-argument is that it improves transparency, and from the market’s perspective, fears are deemed to have been overblown.

Georgian Banks

I have looked at the two banks, and both of them seem to be compelling with the recent new law causing a dip, which I believe offers an entry point. Both of the banks are very profitable, high-tech, and offer good growth. BGEO is slightly larger, has more liquid shares and has grown slightly faster. But then TBCG has a subsidiary, which could transform it. It is cheaper, and ironically, the shares are slightly less volatile.

Buy the Dip

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd