Issue 32;

Clean Up with UK Small Caps

The leading global value managers are currently highly focused on UK small-caps because they have been left behind. As a result, we have seen an abnormally high level of takeover activity as foreign investors snap up once-in-a-lifetime bargains. The UK economy is far from strong, but it’s not weak enough to take the blame. For that, we look to things like outdated stamp duty on UK share transactions, excessive regulation, repeated political dramas, super-taxes for North Sea Oil and Gas, net-zero targets, and the general anti-business agenda. Yet despite all of this, the UK smaller companies are world-class and ripe with innovation, creativity, and scope.

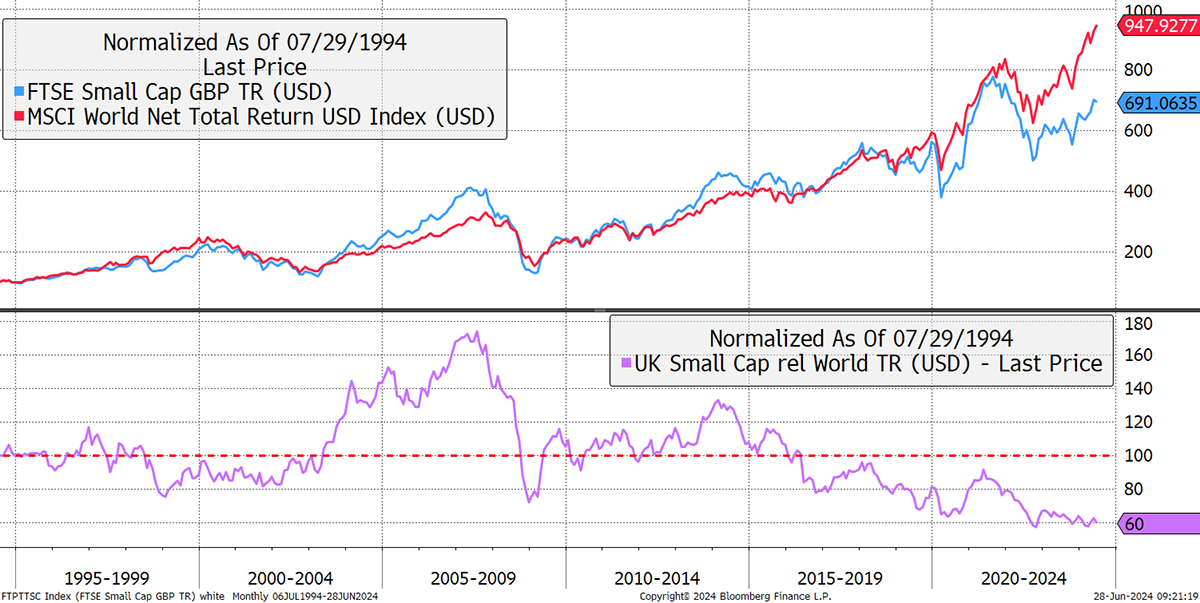

UK Small Caps Relative to the World Total Return in USD – 30 Years

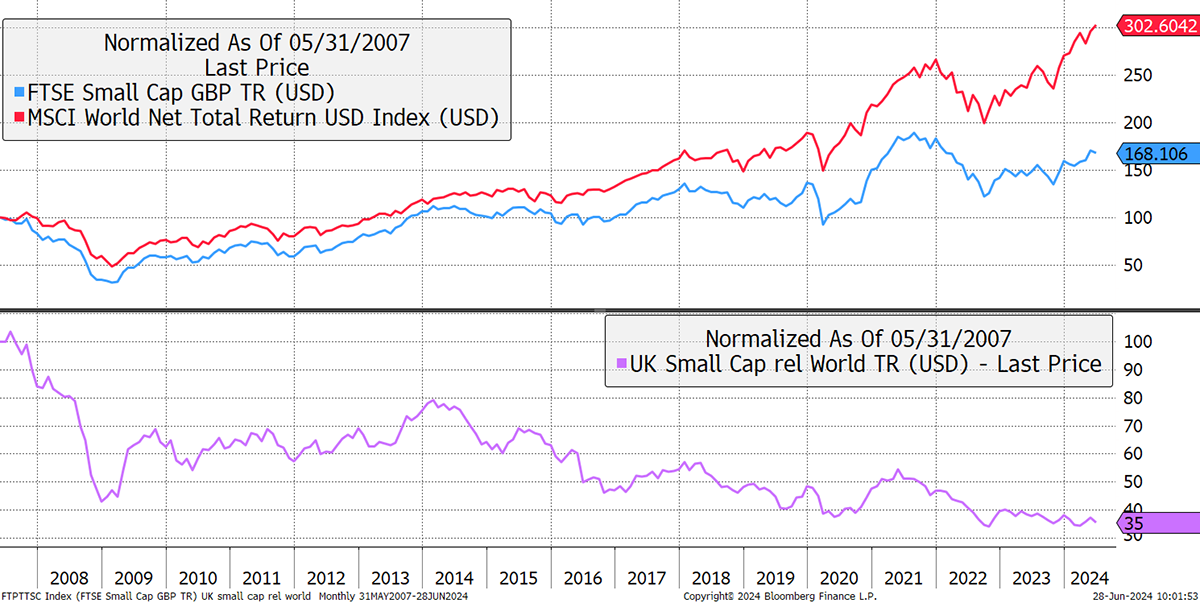

Having been highly correlated with global equities for three decades, UK small-caps have fallen behind. $100 in the world index back in 1994 would be worth $947 today, and in the UK smaller companies, $691. The high point on the purple relative chart was in May 2007. Rebasing the chart to that date shows UK small-caps lagging the world by 65%, which means they need to double to catch up. The good news is that they will.

UK Small Caps Relative to the World Total Return in USD – Since May 2007

In the 32nd issue of Venture, I select a pharmaceutical company that has fallen 68% in recent years despite growing the top line for 20 years in 100 countries and generating strong cashflow. In a rational market, these opportunities should not exist.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid. Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds - Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment. Exchange Traded Funds (ETFs) with derivative exposure (leveraged or inverted ETFs) are highly speculative and are not suitable for risk-averse investors.

Bonds - Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation - Profits from investments, and any profits from converting cryptocurrency back into fiat currency is subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change.

Investment Director: Charlie Morris. Editors or contributors may have an interest in recommendations. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of ByteTree Group Ltd. ByteTree Asset Management (FRN 933150) is an Appointed Representative of Strata Global Ltd (FRN 563834), which is regulated by the Financial Conduct Authority.

© 2026 ByteTree Group Ltd